Fill out Fischer Homes forms

with AI.

Fischer Homes provides a variety of administrative and financial documents designed to help employees manage their internal benefits and retirement planning. These forms are essential for maintaining the financial health of the workforce, ensuring that team members can navigate the complexities of corporate benefits with clarity and precision. By providing standardized documentation for financial requests, the company ensures that all employee actions are recorded accurately and processed in compliance with internal policies and federal regulations.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About Fischer Homes forms

Typically, these forms are utilized by current Fischer Homes employees who are reaching specific financial milestones or require access to their retirement accounts. For instance, when an employee needs to manage their 401(k) through an in-service distribution, these documents allow them to specify whether funds should be paid directly or rolled over into an IRA. Because these decisions involve significant tax implications and long-term financial planning, completing the paperwork correctly is vital to avoid processing errors or unexpected tax liabilities.

Navigating corporate paperwork can often be a tedious process, but tools like Instafill.ai use AI to fill these forms in under 30 seconds while ensuring data is handled accurately and securely. This technology offers a practical way for employees to complete their documentation quickly, allowing them to spend less time on manual data entry and more time focusing on their professional goals within the company.

Forms in This Category

The forms in this category have a median Form Complexity Index of 40/100 (Basic), measured across 1 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

| Form Name | Pages | FCI | |

|---|---|---|---|

| 1. | Fischer Homes Request for In-Service Distribution | 1 | Basic 40 |

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

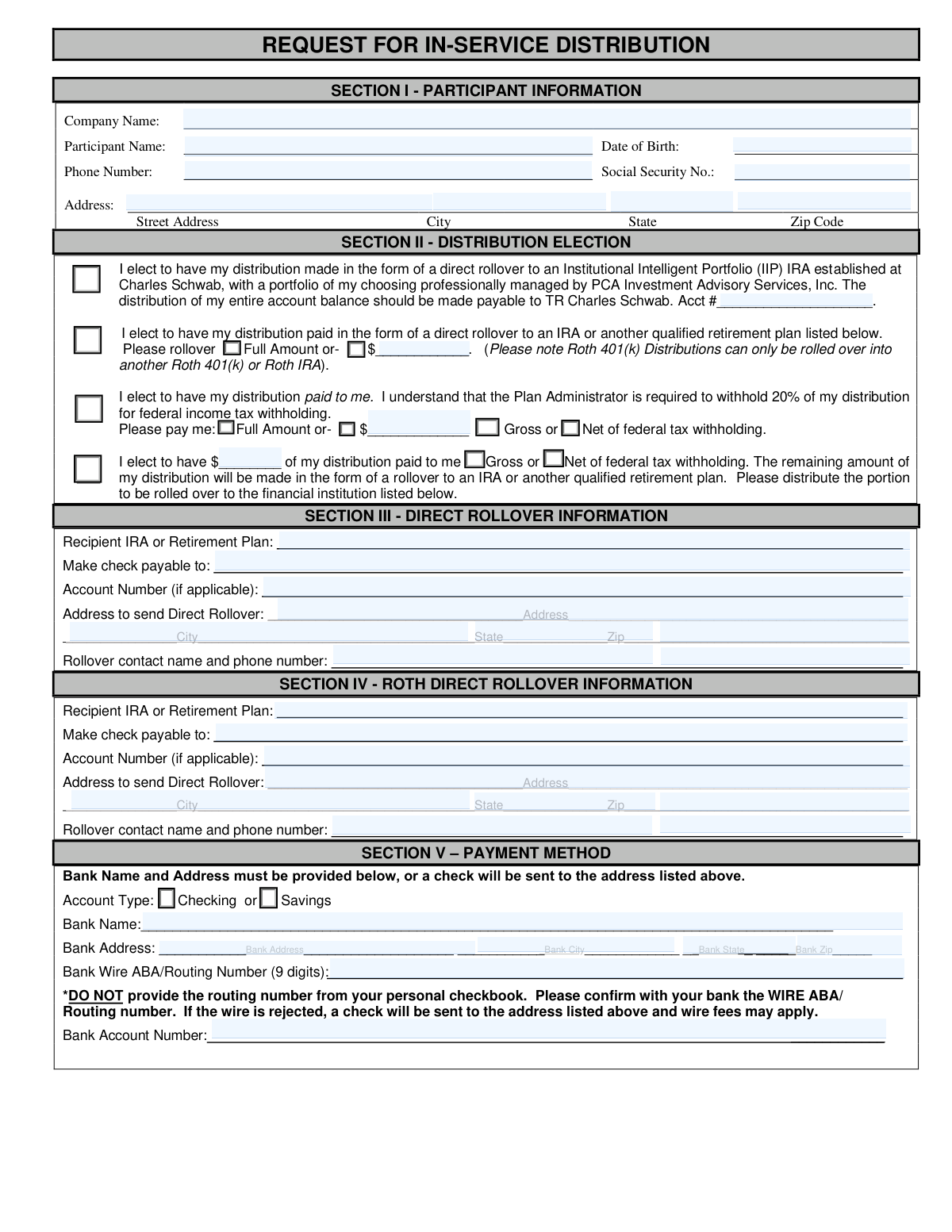

Selecting the correct documentation for your retirement plan is essential for ensuring your funds are handled according to your financial goals. Currently, the primary document available in this category is the Fischer Homes Request for In-Service Distribution.

Retirement Fund Access for Active Employees

If you are currently employed by Fischer Homes and need to access funds from your company-sponsored retirement plan, the Fischer Homes Request for In-Service Distribution is the specific form you require. Unlike standard withdrawal forms intended for former employees, this document is specifically tailored for those who remain on the payroll but meet the plan's criteria for a distribution (such as reaching a certain age or qualifying for specific plan provisions).

When to Use This Form

You should select this form if you intend to perform any of the following actions regarding your retirement account:

- Direct Payments: Requesting a cash distribution paid directly to you for immediate use.

- Rollovers: Moving funds from your Fischer Homes retirement account into an Individual Retirement Account (IRA) or another qualified employer plan to maintain tax-deferred status.

- Tax Management: Outlining your specific federal and state tax withholding options to ensure compliance with IRS regulations.

- Combination Requests: Specifying a split distribution where a portion is paid to you and the remainder is rolled over.

Streamlining Your Request

Filling out financial documents can be complex due to the specific tax information and account details required. By using the Fischer Homes Request for In-Service Distribution through Instafill.ai, you can leverage AI to ensure all fields are accurately addressed. Our platform helps you convert static PDF versions into interactive, fillable forms, allowing you to complete your retirement request quickly and submit it to plan administrators without the hassle of manual printing and scanning.

Form Comparison

| Form | Purpose | Distribution Options | Who Files It |

|---|---|---|---|

| Fischer Homes Request for In-Service Distribution | Access retirement plan funds while still actively employed by the company. | Direct payment to participant, IRA rollover, or a combination of both. | Active employees participating in the Fischer Homes retirement plan. |

Tips for Fischer Homes forms

Before filling out distribution forms, review your specific plan document to ensure you meet the age or service requirements for an in-service withdrawal. Submitting a request when you are ineligible can lead to administrative rejections and unnecessary delays in accessing your funds.

Carefully consider how much tax you want withheld from a direct payment versus choosing a rollover. Direct distributions are typically subject to mandatory federal withholding, which can significantly reduce the net amount you receive compared to a direct transfer to an IRA.

Ensure that all routing and account numbers for the receiving bank or IRA provider are 100% accurate. A single transposed digit can cause the funds to be returned to the plan, requiring you to restart the entire application process from the beginning.

Many employer-sponsored retirement plans require a spouse's notarized signature for distributions over a certain amount. Review the form instructions early to see if you need to coordinate with a notary, as missing signatures are a common cause for processing holds.

AI-powered tools like Instafill.ai can complete these forms in under 30 seconds with high accuracy, extracting the necessary data and placing it in the correct fields automatically. Your sensitive financial data stays secure during the process, providing a fast and safe alternative to manual entry.

Always save a copy of the completed and signed form for your personal financial archives before submitting it to the plan administrator. Having a digital backup allows you to quickly resolve discrepancies if there are questions regarding your distribution or tax reporting later in the year.

Frequently Asked Questions

These forms are used by current employees of Fischer Homes who participate in the company's retirement plan and wish to withdraw funds while still employed. They allow participants to specify the distribution amount and how the funds should be delivered or rolled over into another account.

Eligibility generally depends on the specific terms of the Fischer Homes retirement plan, such as reaching a certain age (often 59 ½) or meeting specific hardship requirements. Employees should consult their Summary Plan Description (SPD) or HR representative to confirm their current eligibility status before filling out the form.

Participants typically choose between a direct payment to themselves, a direct rollover to an Individual Retirement Account (IRA) or another qualified employer plan, or a combination of both. Choosing a rollover can often help avoid immediate tax liabilities and potential early withdrawal penalties.

Yes, distributions are generally subject to federal income tax withholding, and a 10% early withdrawal penalty may apply if the participant is under age 59 ½. The form includes sections to specify tax withholding preferences, but consulting a professional tax advisor is recommended before submission.

Once the form is filled out and signed, it is typically submitted to the Fischer Homes Human Resources department or the designated third-party retirement plan administrator. You should contact your benefits coordinator to confirm the preferred submission method, whether it be via email, mail, or an internal employee portal.

You will need your personal identification details, Social Security number, and current contact information. If you are opting for a rollover, you will also need the account information and mailing address of the financial institution that will receive the funds.

Yes, AI tools like Instafill.ai can be used to fill out Fischer Homes forms by accurately extracting data from your source documents and placing it directly into the required fields. This ensures that the information is consistent and reduces the risk of manual entry errors.

Using AI-powered services, you can complete these forms in under 30 seconds. The technology quickly maps your data to the PDF structure, allowing you to review and download the finalized document almost instantly.

No, the In-Service Distribution form is specifically designed for active employees. If you are a former employee looking to move your retirement funds, you would typically use a standard distribution or rollover request form designed for terminated or retired participants.

If you have a static PDF or a scanned image of the form, AI services like Instafill.ai can convert these non-fillable versions into interactive forms. This allows you to type directly into the document online rather than having to print it and fill it out by hand.

Depending on the specific plan rules and the amount being requested, spousal consent may be required and must often be witnessed by a notary public. Review the instructions on the form carefully to see if a spouse's signature is mandatory for your specific distribution type.

After the form is submitted and approved by the plan administrator, processing times can vary from a few business days to several weeks. Factors such as the method of payment and the accuracy of the information provided on the form can influence the final timeline.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 40/100 (Basic). See exactly how it is calculated.

- In-Service Distribution

- A withdrawal of funds from an employer-sponsored retirement plan while the employee is still actively working for the company, usually subject to specific age or plan requirements.

- Direct Rollover

- A transaction where retirement funds are moved directly from the employer's plan to an IRA or another eligible plan, avoiding immediate taxes and penalties.

- Mandatory Federal Withholding

- The requirement for plan administrators to withhold 20% of a distribution for federal income tax if the funds are paid directly to the employee instead of being rolled over.

- Qualified Retirement Plan

- An employer-sponsored plan, such as a 401(k), that meets IRS standards for tax-deferred savings and employer contribution rules.

- Vested Balance

- The portion of a retirement account that belongs entirely to the employee, including all of their own contributions and the earned portion of employer matching funds.

- Hardship Withdrawal

- A specific type of distribution allowed by the IRS for an 'immediate and heavy financial need,' such as medical expenses or preventing eviction.

- Early Withdrawal Penalty

- An additional 10% tax imposed by the IRS on most retirement plan distributions taken before the participant reaches the age of 59½.

- Qualified Domestic Relations Order (QDRO)

- A legal order, typically from a divorce settlement, that grants a spouse or dependent the right to a portion of a participant's retirement benefits.