Failing to attach Form 5329 to the tax return when required can lead to processing delays and potential penalties. It is crucial to understand when this form is necessary, such as when additional taxes on retirement plans or other tax-favored accounts are owed. Taxpayers should review the instructions for their tax return and Form 5329 to determine if attachment is necessary. To avoid this mistake, double-check the filing requirements and ensure that Form 5329 is securely attached to the tax return before submission.

When filing Form 5329 independently of a tax return, it is mandatory to sign and date the form to validate it. An unsigned or undated form may be considered invalid and can result in the IRS not recognizing the form, leading to unnecessary delays and possible penalties. Taxpayers should ensure that they sign and date the form in the designated area. Before mailing, it is advisable to review the form to confirm that all required signatures and dates are present.

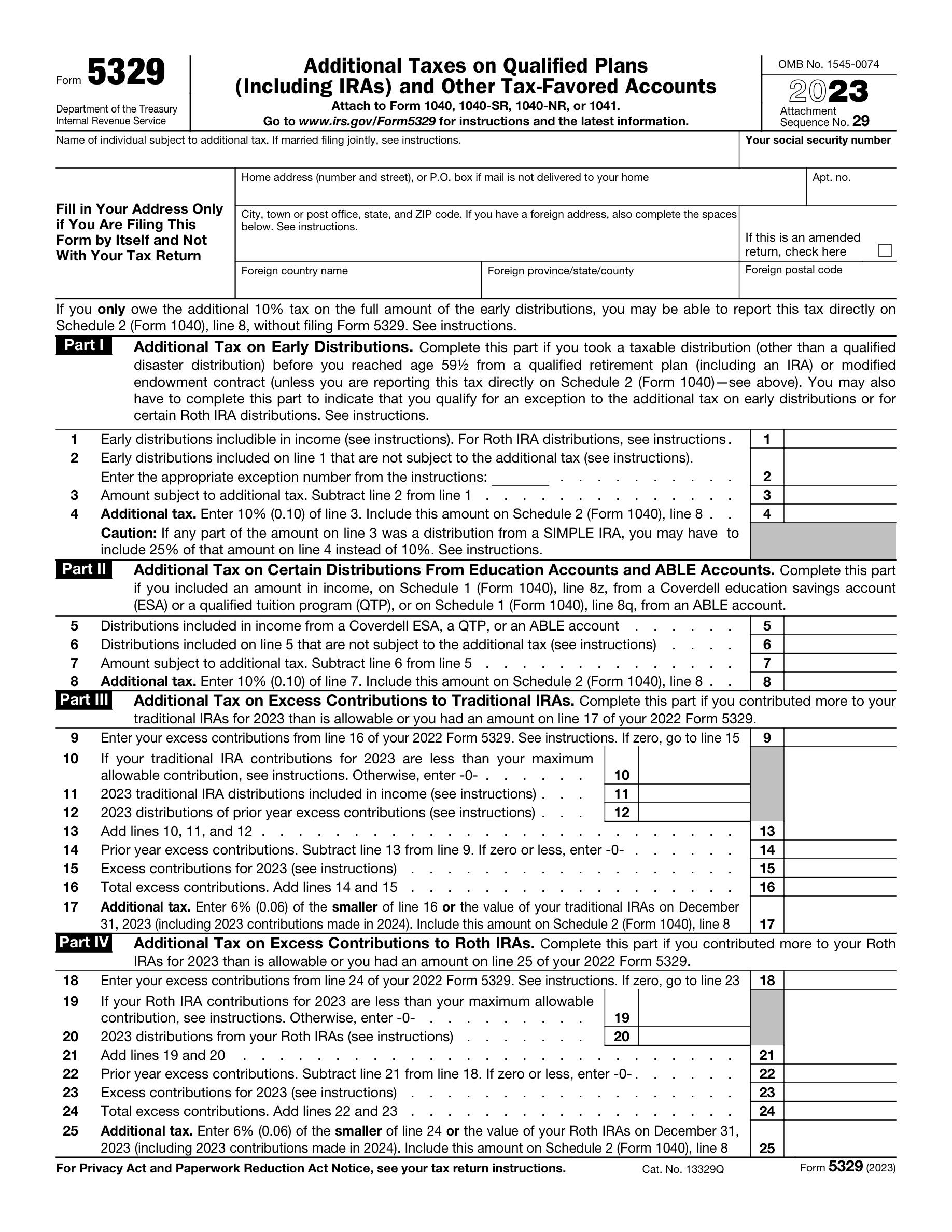

Incorrectly calculating the additional tax as 10% of early distributions is a common error that can result in an inaccurate tax liability. The additional tax should be calculated based on specific IRS rules that may not always equate to a flat 10% of the distribution. Taxpayers should carefully read the instructions for Form 5329 and use the correct calculation method as outlined by the IRS. Utilizing tax software or consulting with a tax professional can also help ensure the accuracy of these calculations.

Omitting the exception number for distributions not subject to the additional tax can lead to the IRS incorrectly assessing additional taxes. It is important to identify and enter the appropriate exception number on Form 5329 to indicate that the distribution is not subject to the additional tax. Taxpayers should review the list of exceptions provided in the form's instructions and accurately report the applicable exception number. Careful attention to detail when completing this section can prevent unnecessary correspondence with the IRS.

Miscalculating the amount subject to additional tax by not properly subtracting line 2 from line 1 in Part I can result in an incorrect tax amount being reported. This mistake can occur if taxpayers overlook the need to subtract certain contributions or distributions that are not subject to the additional tax. To avoid this error, it is essential to follow the calculation instructions on Form 5329 carefully and ensure that all arithmetic is done correctly. Reviewing the form for accuracy or seeking assistance from a tax professional can help prevent this type of error.

Taxpayers often overlook the requirement to report additional taxes from qualified plans on Schedule 2 (Form 1040), line 8. This omission can lead to underreporting of tax liability and potential penalties. To avoid this mistake, carefully review all distributions from qualified plans and ensure any additional taxes are calculated as per the instructions for the form. Double-check that these amounts are correctly entered on Schedule 2, line 8, before filing your tax return.

Incorrectly reporting the amount of distributions from education accounts, such as 529 plans or Coverdell ESAs, can result in inaccurate tax calculations. It is essential to maintain accurate records of all distributions and their purposes. Verify that the distribution amounts used in your tax calculations match your financial records. Ensure that the distributions used for qualified education expenses are reported correctly to avoid unnecessary additional taxes.

Taxpayers sometimes fail to calculate and report the 6% additional tax on excess contributions to traditional IRAs. This error can occur if contributions exceed the allowable limits or if the taxpayer's income is too high for deductible contributions. To prevent this mistake, monitor your contributions throughout the year and compare them against the annual limits. If you have over-contributed, withdraw the excess amount before the tax filing deadline to avoid the additional tax.

Reporting additional tax on excess contributions to Roth IRAs can be complex due to the specific rules governing these accounts. Ensure that you understand the contribution limits and phase-out ranges based on your modified adjusted gross income. If you contribute more than the allowed amount, you must calculate and report a 6% tax on the excess contributions. Use the correct forms and worksheets to determine any additional tax owed and report it accurately on your tax return.

When contributing to Coverdell Education Savings Accounts (ESAs), it is crucial to avoid exceeding the annual contribution limits. Miscalculating the additional tax due on excess contributions is a common error. To avoid this, track your contributions to ensure they do not surpass the limit for the tax year. If you do contribute too much, the excess must be withdrawn or subject to a 6% excise tax. Use the appropriate IRS forms and instructions to calculate any additional tax accurately.

Incorrect calculation of additional tax on excess contributions to Archer Medical Savings Accounts (MSAs) can lead to reporting errors on the form. To avoid this mistake, individuals should carefully review the contribution limits for the tax year and use the instructions provided in the form to calculate the additional tax accurately. It is advisable to double-check the math and consider using tax preparation software or consulting with a tax professional to ensure the calculations are correct. Keeping detailed records of all contributions throughout the year can also help prevent this error.

Omitting the additional tax on excess contributions to Health Savings Accounts (HSAs) is a common oversight. Taxpayers should be vigilant in tracking their contributions to HSAs to ensure they do not exceed the annual limit. If excess contributions are made, it is crucial to report the additional tax owed on the form. Taxpayers can avoid this mistake by reviewing the contribution limits, correcting excess contributions before the tax filing deadline, and using the instructions on the form to report any additional tax due.

When it comes to Achieving a Better Life Experience (ABLE) accounts, not calculating the additional tax on excess contributions correctly can result in reporting inaccuracies. Taxpayers should familiarize themselves with the specific contribution limits for ABLE accounts and use the form's instructions to determine any additional tax liability. To prevent errors, it is recommended to monitor contributions throughout the year, promptly address any excess contributions, and seek assistance from tax preparation resources or professionals if needed.

Reporting the additional tax on excess accumulation in qualified retirement plans inaccurately can have significant consequences. Taxpayers should ensure they understand the requirements for minimum distributions and the tax implications of any accumulations beyond these amounts. To avoid mistakes, individuals should carefully calculate the required minimum distributions, report any excess accumulations accurately, and consult the form's instructions or a tax advisor for guidance. Regular review of retirement account statements can also help in maintaining accurate records.

If a paid preparer is used, their failure to sign, date, and provide their information on the form is a procedural error that can lead to processing delays. To ensure compliance, paid preparers must remember to provide their signature, the date of completion, and their relevant information in the designated sections of the form. Taxpayers should verify that their preparer has completed these steps before submitting the form. It is also important for taxpayers to choose a reputable and reliable tax preparer who understands the importance of these details.

Failing to review the entire form for accuracy and completeness before signing can lead to errors or omissions that may result in penalties or delays in processing. It is crucial to double-check all entries and ensure that every required section is filled out correctly. Cross-referencing the information provided with personal financial records can help verify accuracy. It is also advisable to have a second pair of eyes, such as a tax professional, review the form before submission.

Submitting Form 5329 independently when not eligible is a common error that can cause complications with the IRS. Taxpayers should understand the specific circumstances under which Form 5329 should be filed separately. In most cases, this form accompanies the taxpayer's standard tax return. To avoid this mistake, taxpayers should carefully read the instructions regarding eligibility for separate filing and consult with a tax advisor if there is any uncertainty.

Neglecting to follow the detailed instructions for each part of the form can result in incorrect or incomplete entries, which may lead to penalties. It is essential to read and understand the instructions for each section before filling out the form. If there is any confusion, taxpayers should seek clarification from the IRS guidelines or a tax professional. Taking the time to comprehend each step can prevent costly errors and ensure compliance with tax regulations.

Misunderstanding the form's requirements often leads to entering incorrect information, which can have serious consequences, including fines or an audit. To avoid this, taxpayers should familiarize themselves with the form's terminology and requirements before beginning the process. Utilizing IRS resources or consulting with a tax professional can provide clarity. Additionally, taxpayers should not rush through the form and should take the time to carefully read each question and its instructions.

Omitting to report the correct amounts on the corresponding lines of the form can result in an inaccurate tax calculation and potential penalties. Taxpayers should ensure that all amounts entered on the form are accurate and correspond to the correct lines as indicated by the instructions. Double-checking figures against financial statements or previous tax returns can help ensure accuracy. It is also beneficial to use a calculator or tax software to prevent simple arithmetic errors.