Failing to submit the Taxpayer's Notice to Initiate an Appeal by the specified deadline can result in the dismissal of the appeal. It is crucial to be aware of the deadline, which is typically a fixed number of days after the assessment notice date. Taxpayers should mark their calendars and set reminders to ensure timely submission. To avoid this mistake, it is recommended to prepare the appeal well in advance and consider mailing it with a service that provides delivery confirmation.

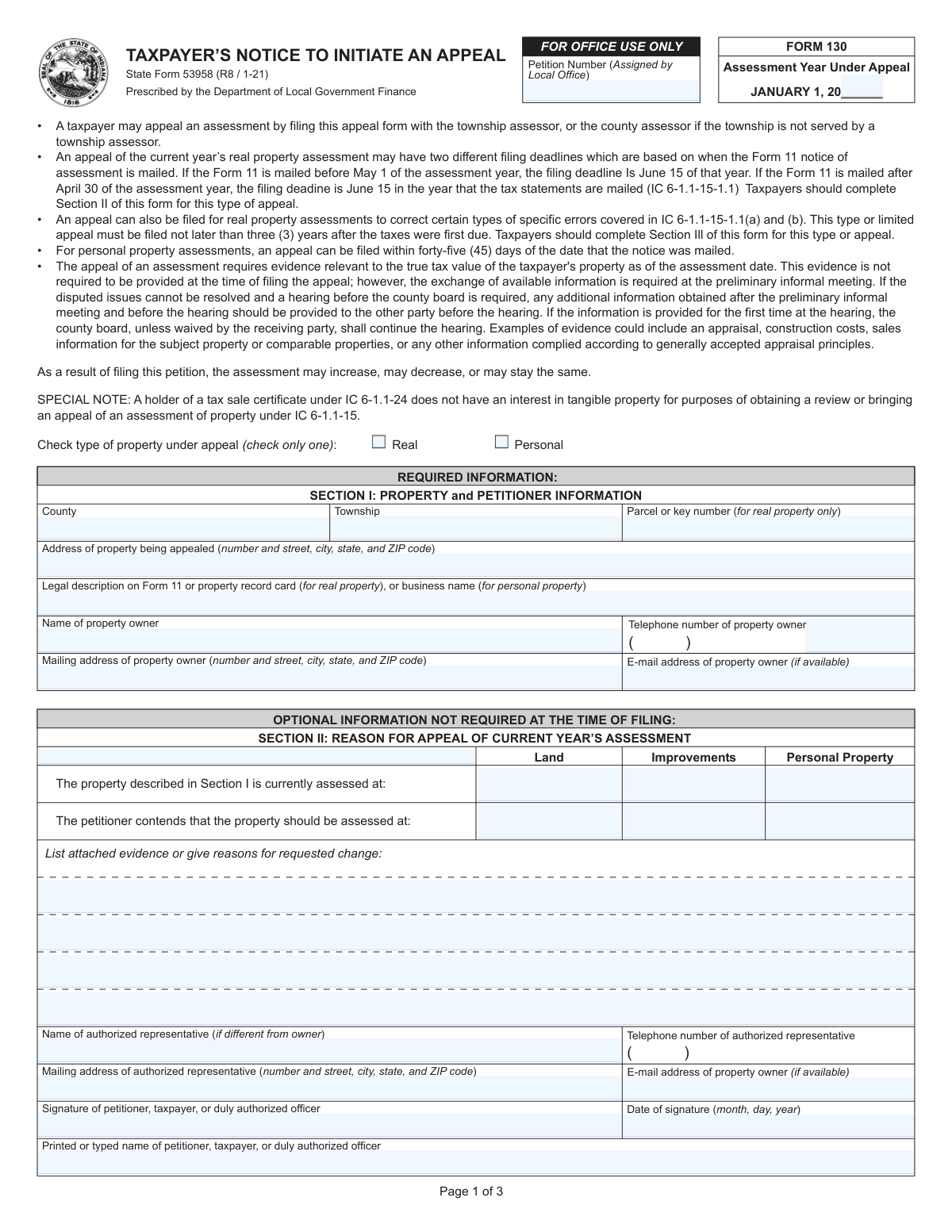

Leaving property or petitioner information incomplete in Section I can lead to processing delays or even the rejection of the appeal. It is essential to double-check that all fields are filled out accurately, including the property address, owner's name, and contact details. Before submitting the form, review all entries to ensure completeness. Using a checklist of required information can help ensure that no details are overlooked.

Not specifying the type of property in Section II can cause confusion and hinder the appeal process. The form typically requires the taxpayer to classify the property as residential, commercial, industrial, or agricultural. To avoid this error, carefully read the instructions for Section II and select the appropriate property type. If uncertain about the correct classification, consult the assessment notice or reach out to the local tax assessor's office for guidance.

An appeal without supporting evidence for the contention that the property's assessed value is incorrect is likely to be unsuccessful. It is important to gather relevant documentation, such as comparable sales data, appraisals, or photographs, to substantiate the claim. Organize the evidence clearly and reference it in the appeal form. To prevent this mistake, prepare the evidence in advance and ensure it is readily available when filling out the form.

If a taxpayer is represented by an authorized individual, such as an attorney or tax agent, omitting this representative's contact information can lead to communication issues. Ensure that the representative's name, address, phone number, and email are provided in the designated section. This allows the appeals board to contact the representative directly with any questions or updates. To avoid this oversight, verify the representative's contact details before submitting the form and confirm that they are willing to act on the taxpayer's behalf.

Filling out the petition number section incorrectly can lead to processing delays or the appeal being misdirected. It is crucial to double-check the petition number for accuracy before submission. Ensure that the number matches the one provided in the initial assessment notice. If you are unsure of the petition number, contact the appropriate tax authority for confirmation. Always review the entire form for accuracy before submitting.

An unsigned or undated form is often considered incomplete and can result in the rejection of the appeal. Always remember to sign and date the form in the designated areas. Verify that the date corresponds with the actual day of signing to avoid any confusion. Keep a copy of the signed and dated form for your records. It is advisable to check the form for a signature and date as the last step before mailing or submitting it electronically.

Omitting details about the error in Section III can hinder the review process, as the authorities may not understand the basis for the appeal. Be specific and clear when describing the error you wish to correct. Provide all necessary details and reference any applicable laws or regulations that support your claim. If additional space is needed, attach a separate sheet with a full explanation. Review Section III thoroughly to ensure that your explanation is complete and understandable.

Neglecting to attach supporting documentation or evidence can weaken your appeal, as the tax authority relies on this information to make an informed decision. Gather all relevant documents before filling out the form. Make sure to reference these documents in the form where appropriate, and attach them securely. Keep copies of all documents for your records. Before submitting the form, double-check that all necessary attachments are included.

Selecting the incorrect box for the type of property can lead to misunderstandings regarding the appeal. Review the definitions of property types provided by the tax authority to ensure you are selecting the correct category. If you are uncertain about which box to check, seek guidance from a tax professional or the issuing authority. After making your selection, review the form to confirm that the correct box is checked. Correctly identifying the property type is essential for the appeal to be assessed properly.

Failing to comprehend the roles of the Property Tax Assessment Board of Appeals (PTABOA) and the Indiana Board of Tax Review (IBTR) can lead to confusion about the appeal process and the appropriate steps to take. It is crucial for taxpayers to recognize that the PTABOA is the first level of appeal where they can present their case, while the IBTR is the next level if further appeal is necessary. To avoid this mistake, taxpayers should thoroughly research or seek guidance on the specific functions and jurisdictions of these bodies before initiating an appeal. Understanding the hierarchy and the role of each entity ensures that the appeal is directed to the correct authority and that the taxpayer is prepared for the process.

Taxpayers often initiate an appeal without a clear understanding of the potential outcomes, which can lead to unrealistic expectations or unpreparedness for the result. It is important to be aware that the appeal could result in a decrease, increase, or no change to the assessed value of the property. Before filing an appeal, taxpayers should consider consulting with a tax professional or legal advisor to gain insight into the possible outcomes and to develop a well-informed strategy. This preparation can help manage expectations and ensure that the taxpayer is ready for any adjustments that may result from the appeal.

Overlooking the review of relevant statutes and deadlines is a common mistake that can lead to the dismissal of an appeal. Each jurisdiction has specific legal requirements and time frames within which an appeal must be filed. To prevent this error, taxpayers should carefully read the governing statutes and mark all critical deadlines on their calendar well in advance. Seeking clarification from local tax authorities or legal counsel can also help ensure compliance with all procedural requirements. Adhering to the established timelines and legal guidelines is essential for a valid and timely appeal.

Submitting the Taxpayer's Notice to Initiate an Appeal to the incorrect assessing official can delay the process or result in the appeal not being heard. It is imperative to identify and verify the correct official or department responsible for handling appeals in the specific jurisdiction. Taxpayers should double-check the address and contact information for the assessing official provided on the form or on the official government website. If there is any uncertainty, contacting the local assessor's office for confirmation can prevent this mistake. Accurate submission ensures that the appeal is processed in a timely and efficient manner.

Omitting contact information such as email addresses and telephone numbers can hinder communication regarding the appeal. This information is essential for the assessing officials to reach out to the taxpayer with updates, requests for additional information, or scheduling of hearings. Taxpayers should ensure that all contact fields are filled out completely and legibly on the appeal form. It is also advisable to provide multiple forms of contact to facilitate easier communication. Keeping contact information up to date and checking it regularly will help maintain an open line of communication throughout the appeal process.

Incorrectly classifying the property type can lead to processing delays and potential rejection of the appeal. It is crucial to accurately determine whether the property in question is real property, such as land and buildings, or personal property, which includes movable items like vehicles and equipment. To avoid this mistake, carefully review the definitions of real and personal property provided by the tax authority. Double-check the classification against your property records and consult with a professional if you are uncertain about the correct category for your property.

An appeal without a strong justification for the requested change in valuation or assessment is likely to be unsuccessful. It is essential to provide clear and compelling evidence to support your claim. To prevent this oversight, gather relevant documentation, such as comparable property assessments, market analyses, or expert appraisals. Make sure to articulate the reasons for your appeal logically and coherently, linking your evidence directly to the points of contention.

Skipping preliminary informal meetings with the assessor can be detrimental to your appeal process. These meetings are an opportunity to resolve disagreements without formal proceedings. To avoid this misstep, make it a priority to attend all scheduled meetings. Prepare for the discussions by reviewing your property assessment and compiling any questions or concerns you may have. Engaging in these meetings can lead to a quicker and more favorable resolution.

Underestimating the burden of proof needed to support your appeal can result in an unfavorable outcome. The taxpayer is typically responsible for proving that the assessment is incorrect. To address this, thoroughly prepare your case by collecting all necessary evidence and organizing it in a clear and persuasive manner. Consider consulting with a tax professional or attorney who can help you understand the burden of proof and assist in building a strong case.

Neglecting to consider the option of further appeals to the Indiana Board of Tax Review (IBTR) or Tax Court can limit your chances for a successful resolution. If the initial appeal does not yield the desired result, be aware of the additional steps available. Familiarize yourself with the timelines and requirements for filing further appeals. Keep track of all correspondence and decisions related to your case, and seek legal advice to navigate the appeals process effectively.