Fill out accounting forms

with AI.

Accounting forms serve as the essential framework for financial reporting, tax compliance, and internal record-keeping. These documents, which range from specialized business forms to standard banking and financial forms, allow organizations to maintain transparency and accuracy in their fiscal operations. Proper documentation is critical for ensuring that income, expenses, and liabilities are reported correctly, helping entities stay in alignment with regulatory requirements and professional standards.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About accounting forms

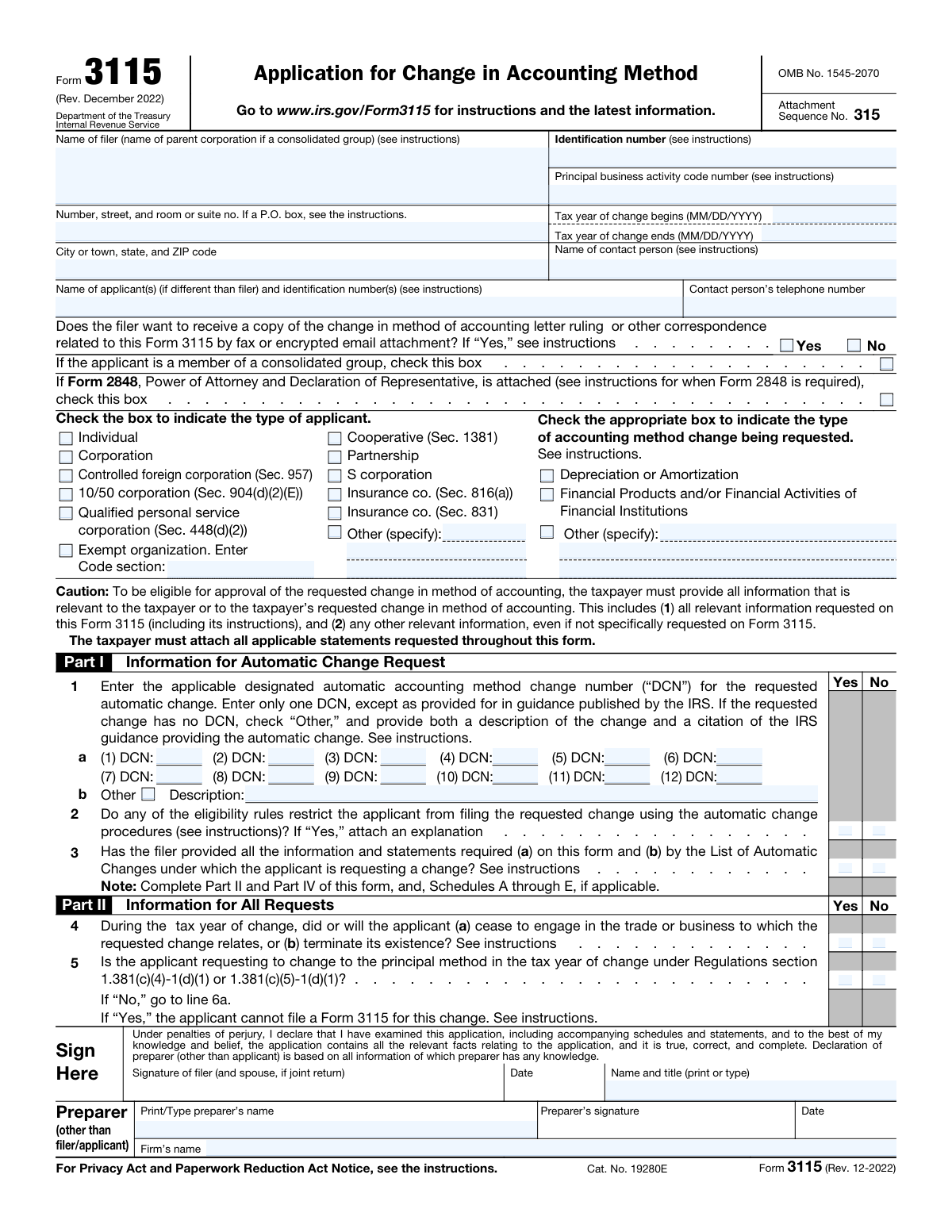

These forms are primarily utilized by business owners, certified public accountants, and tax professionals who must navigate complex financial transitions or meet annual filing deadlines. For example, a company might use specific documentation like Form 3115 when they need to request a formal change in their accounting method to better suit their evolving business model. Whether it is during a routine audit or the height of tax season, having access to the correct paperwork ensures that financial data is communicated clearly to stakeholders and government agencies like the IRS.

While manual data entry for these documents can be tedious, modern technology has made the process much more efficient. Tools like Instafill.ai use AI to fill these accounting forms in under 30 seconds, ensuring the data is handled both accurately and securely. This allows professionals to spend less time on administrative paperwork and more time focusing on high-level financial strategy.

Forms in This Category

The forms in this category have a median Form Complexity Index of 72/100 (Complex), measured across 1 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

| Form Name | Pages | FCI | |

|---|---|---|---|

| 1. | Form 3115, Application for Change in Accounting Method | 8 | Complex 72 |

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Navigating the complexities of accounting and financial documentation requires precision. Whether you are managing daily bookkeeping or preparing for a significant shift in your tax strategy, selecting the correct document is the first step toward compliance and financial clarity.

Requesting IRS Accounting Changes

If your business is moving away from its current financial reporting structure, you will likely need Form 3115, Application for Change in Accounting Method. This is a specialized tax document used to request formal consent from the IRS to change your accounting practices. You should select this form if:

- Switching Methods: You are transitioning from a cash basis to an accrual basis of accounting (or vice versa).

- Correcting Errors: You have consistently used an incorrect accounting method and need to bring your filings into compliance.

- Operational Shifts: Your business model has changed, necessitating a different way of reporting income and expenses to accurately reflect your financial status.

General Business and Financial Needs

While Form 3115 is highly specific to tax reporting, other business forms and banking forms in this category serve broader purposes. When deciding which document to use, identify your primary goal:

- Tax Compliance: Focus on IRS-specific documents like the Application for Change in Accounting Method to ensure you are meeting federal requirements.

- Operational Management: Use general financial forms for internal audits, expense tracking, and year-end summaries.

- Banking & Credit: Look for specialized banking forms when dealing with loan applications, line of credit adjustments, or corporate account updates.

Simplify Complex Filing

Forms like Form 3115 are notoriously detailed and can be difficult to navigate manually. Using Instafill.ai allows you to transform these static PDFs into interactive, AI-powered documents. This ensures that your Application for Change in Accounting Method is filled out accurately, reducing the risk of IRS rejection and saving your team valuable time during tax season.

Form Comparison

| Form | Purpose | Who Files It | When to Use |

|---|---|---|---|

| Form 3115, Application for Change in Accounting Method | Request IRS consent to change accounting method | Businesses or individuals changing financial reporting practices | When altering how income or expenses are reported for taxes |

Tips for accounting forms

Inaccurate calculations or transposed numbers are the most common errors in accounting forms. Always cross-reference your entries with your general ledger or bank statements to ensure every decimal point and figure is accurately placed before submission.

Most financial and business forms require supplementary evidence, such as balance sheets or income statements. Keep these documents organized in a digital folder so you can quickly reference specific data points while filling out the primary application.

AI-powered tools like Instafill.ai can complete complex accounting forms in under 30 seconds with high accuracy. This technology ensures your sensitive financial data stays secure during the process, providing a massive time-saver for business owners dealing with multiple forms.

When changing accounting methods or reporting business data, ensure the information aligns with your prior years' tax returns. Significant discrepancies between current and past forms can often lead to requests for clarification or processing delays.

Many business and banking forms must be signed by a specific officer, such as a CFO or a managing member. Identify who is legally authorized to sign early in the process to avoid last-minute delays during the submission phase.

When filling out forms for accounting method changes, clearly define whether the change is considered automatic or requires a specific ruling. Misclassifying the type of change can lead to the form being rejected or processed under the wrong regulatory framework.

Frequently Asked Questions

These forms are used to document financial practices and request official changes in how income or expenses are reported to regulatory bodies. Specifically, forms like the 3115 allow taxpayers to seek IRS consent when transitioning between different accounting methods to ensure ongoing tax compliance.

Business owners, corporations, partnerships, and self-employed individuals are generally responsible for filing these forms when their financial reporting needs change. If a taxpayer's structure or reporting style evolves, they must submit the appropriate documentation to the IRS or relevant tax authority to remain in good standing.

Yes, AI tools like Instafill.ai can process complex accounting forms by accurately extracting data from your source documents and placing it into the correct fields. This technology ensures that even detailed financial forms are completed with high precision, significantly reducing the risk of manual entry errors.

While manual completion can take a significant amount of time due to the technical nature of financial data, AI-powered services can fill these forms in under 30 seconds. By automating the data mapping process, users can quickly move from a blank PDF to a completed, ready-to-file document.

A change is often necessary when a business grows, changes how it tracks inventory, or moves from a cash-based system to an accrual-based system. Filing the correct accounting form ensures that the transition is officially recognized by the IRS and prevents discrepancies in future tax returns.

Most of these forms are submitted directly to the Internal Revenue Service (IRS), often as an attachment to an annual tax return. Some specific forms may require an additional copy to be sent to a dedicated IRS office, so it is important to review the general instructions provided by the agency for the current tax year.

You will generally need your Taxpayer Identification Number (TIN), detailed descriptions of your current and proposed accounting methods, and specific figures from your financial records. Having your previous year's tax returns and current balance sheets ready will make the data entry process much smoother.

While AI tools can help you physically fill out and format the forms quickly, many businesses consult with a CPA or tax professional to determine which accounting method is most beneficial. These forms involve complex tax laws, and professional guidance can help ensure your filing strategy aligns with your long-term financial goals.

Yes, the accounting category includes various forms tailored to specific needs such as depreciation, inventory valuation, or general method changes. Identifying the specific section of the tax code your change falls under will help you select the correct form from the available category list.

Keeping a copy of your filed accounting forms is vital for future audits and for maintaining a consistent financial history for your business. These records serve as proof that you received consent for your reporting methods and help explain any significant shifts in your year-over-year financial data.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 72/100 (Complex). See exactly how it is calculated.

- Accounting Method

- A consistent set of rules used to determine when and how income and expenses are reported for tax and financial purposes.

- Accrual Method

- An accounting system where income is recorded when it is earned and expenses are recorded when they are incurred, regardless of when cash is actually exchanged.

- Cash Method

- An accounting system where income is reported only when it is received and expenses are deducted only when they are paid.

- Section 481(a) Adjustment

- A financial calculation required when changing accounting methods to ensure that items of income or expense are not duplicated or omitted.

- Automatic Consent

- A streamlined IRS procedure that allows taxpayers to change certain accounting methods by following specific instructions without waiting for a formal approval letter.

- Non-Automatic Change

- A request to change an accounting method that requires a manual review by the IRS National Office and typically involves the payment of a user fee.

- Internal Revenue Code (IRC)

- The official body of federal tax laws in the United States that dictates the rules for filing accounting and financial forms.

- Fiscal Year

- A one-year period used by a business for financial reporting and budgeting that may end on a date other than December 31.