Fill out benefit election forms

with AI.

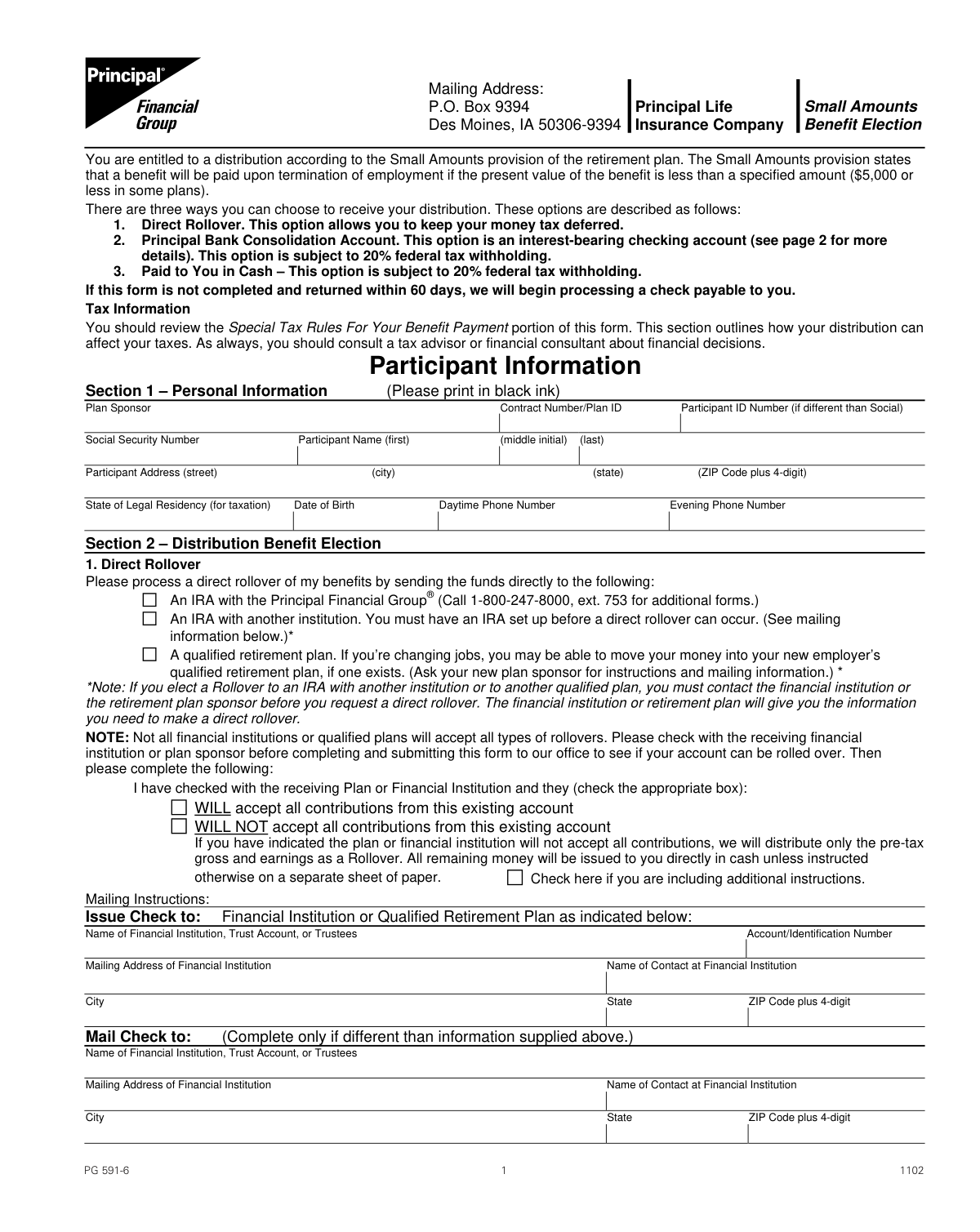

Benefit election forms are essential documents used by employees and plan participants to specify how they wish to receive or manage their employer-sponsored benefits. These forms typically come into play during retirement transitions, job changes, or when specific distribution thresholds are met. By completing these documents, individuals ensure that their financial assets—whether from life insurance policies, pension plans, or 401(k) accounts—are handled according to their specific tax preferences and long-term financial goals.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About benefit election forms

These forms are most commonly required by individuals who are navigating the complexities of retirement plan distributions or small balance payouts. For example, when a participant has a balance that qualifies for a distribution, they must decide whether to roll those funds into a tax-deferred IRA, move them to a consolidation account, or take a direct cash payout. Properly documenting these choices is critical to avoiding unintended tax penalties and ensuring that funds are transferred to the correct financial institutions without delay.

Managing these administrative tasks can be time-consuming, especially when dealing with non-interactive PDF documents. Tools like Instafill.ai use AI to fill these forms in under 30 seconds, handling sensitive data accurately and securely to streamline the election process. This allows participants to focus on their financial planning rather than the tedious manual entry of personal and account information.

Forms in This Category

| Form Name | Pages | FCI | |

|---|---|---|---|

| 1. | Principal Life Insurance Company Small Amounts Benefit Election | 1 | – |

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Choosing the right benefit election form depends on your specific retirement plan provider and the total value of your account balance. In this category, the focus is on small-balance distributions specifically for accounts managed by Principal Life Insurance Company.

When to Use the Principal Small Amounts Benefit Election Form

You should select the Principal Life Insurance Company Small Amounts Benefit Election form if your retirement plan balance is considered a 'Small Amount'—typically $5,000 or less. This form is necessary when you are leaving an employer or the plan is being terminated, and you need to decide where those funds should go. If your balance exceeds $5,000, you will likely need a standard distribution or rollover form instead.

Deciding on Your Distribution Method

Once you have identified that you need this form, the document requires you to choose one of three primary paths for your funds. Your choice depends on your long-term financial goals and immediate tax needs:

- Direct Rollover: Choose this if you want to maintain the tax-deferred status of your savings. This option moves your balance into an Individual Retirement Account (IRA) or another qualified employer plan without triggering a tax bill.

- Principal Bank Consolidation Account: This option transfers your funds into a consolidated account managed by Principal Bank. While it keeps your money within the Principal ecosystem, it is important to review the specific tax withholding rules associated with this transfer.

- Direct Cash Payment: Select this only if you need immediate access to the funds. Be aware that this is a taxable event; federal taxes will be withheld automatically, and you may be subject to additional state taxes or early withdrawal penalties.

Filling Out Your Form Accurately

Financial documents like the Principal Life Insurance Company Small Amounts Benefit Election form require precision to avoid processing delays. By using Instafill.ai, you can quickly convert the static PDF into a fillable format, ensuring that your account numbers and election choices are legible and correctly formatted for the plan administrator.

Form Comparison

| Form | Purpose | Distribution Options | Eligibility Criteria |

|---|---|---|---|

| Principal Life Insurance Company Small Amounts Benefit Election | Select a payout method for retirement plan benefits from small account balances. | Direct Rollover, Principal Bank Consolidation Account, or a direct cash payment. | Retirement plan participants with account balances typically valued at $5,000 or less. |

Tips for benefit election forms

Before selecting a payout method, consider that direct cash distributions are typically subject to mandatory tax withholding. Opting for a direct rollover to an IRA or another qualified retirement plan can help you avoid immediate taxes and preserve the growth of your savings.

Using AI-powered tools like Instafill.ai can help you complete benefit election forms in under 30 seconds with high accuracy. These tools intelligently map your data to the correct fields while ensuring your sensitive information stays secure throughout the entire process.

If you choose to move your funds to another provider, double-check the receiving institution's name and your account number. Even a minor typo in these fields can result in the funds being returned to the original plan, causing significant processing delays.

Many small amount distributions are still issued as physical checks if a consolidation account isn't chosen. Ensure the address provided on the form is current and matches the records held by your plan administrator to prevent the check from being lost in the mail.

Ensure the distribution amount listed on the form aligns with your expectations based on your most recent statement. If the 'Small Amount' figure seems incorrect, contact your plan administrator to verify your vested balance before submitting your election.

Always save a digital copy of the signed and completed form for your personal files. Having a record of your specific election—whether it was a rollover or a cash payout—is essential for accurate tax reporting when you receive your 1099-R at the end of the year.

Frequently Asked Questions

Benefit election forms are used by retirement plan participants to officially choose how they want their plan assets distributed. These forms provide a legal record of whether the individual prefers a direct cash payout, a rollover to another qualified account, or a transfer to a consolidation account.

These forms are typically required for individuals who have left an employer and have a remaining retirement plan balance that is below a specific threshold, often $5,000 or less. Completing the form allows the participant to control the movement of these funds rather than having the plan administrator make a default selection.

Most forms offer three primary options: a tax-deferred direct rollover to an IRA or another employer's qualified plan, a transfer to a designated bank consolidation account, or a direct cash payout. Selecting a rollover is generally the preferred method for avoiding immediate taxes and penalties.

A rollover moves funds directly between financial institutions, which preserves the tax-deferred status of the retirement savings. A direct cash payout sends the money directly to the participant but is subject to mandatory federal income tax withholding and potential early withdrawal penalties.

You should submit the form as soon as you receive notice from your plan provider regarding your eligibility for a distribution. If you do not return the form within the timeframe specified by your plan, the administrator may automatically roll the funds into a default IRA on your behalf.

You will generally need your social security number, your plan participant ID, and the details of the receiving financial institution if you are choosing a rollover. It is helpful to have your most recent account statement available to ensure all account numbers and plan names are entered correctly.

Completed forms are typically submitted to the plan administrator or the insurance company managing the assets, such as Principal Life Insurance Company. Many providers accept these forms through secure online portals, though some may still require submission via mail or fax.

Yes, AI tools like Instafill.ai can assist in filling out these forms by accurately extracting data from your source documents and placing it into the correct fields on the PDF. This helps ensure that sensitive information like account numbers and personal details are transferred without manual entry errors.

Once the completed form is received and verified, processing usually takes between two to four weeks. The exact timing depends on the plan provider's internal procedures and the method of distribution you selected.

Yes, choosing a cash payout typically triggers a mandatory 20% federal tax withholding, and you may be liable for an additional 10% penalty if you are under age 59½. Direct rollovers to an IRA or another qualified plan generally do not result in immediate tax liabilities.

While manual entry can take significant time, using AI-powered services like Instafill.ai allows you to fill these forms in under 30 seconds. The AI quickly parses your information and populates the form accurately, making the process much more efficient than traditional methods.

Errors on a benefit election form can lead to processing delays or incorrect tax withholdings. If you realize an error was made after submission, you should contact your plan administrator immediately to see if the distribution can be corrected before the funds are moved.

Glossary

- Direct Rollover

- The process of transferring retirement funds directly from one plan to another or into an IRA without the money being paid to you first, which avoids immediate taxes and penalties.

- Qualified Plan

- A retirement savings plan, such as a 401(k) or pension, that meets specific IRS requirements and provides tax advantages to the account holder.

- Tax Withholding

- The portion of a cash distribution that an employer or financial institution is legally required to send directly to the IRS as a prepayment of your income taxes.

- IRA (Individual Retirement Account)

- A personal tax-advantaged savings account that allows individuals to save for retirement independently of an employer-sponsored plan.

- Tax-Deferred

- A status where taxes on investment earnings or contributions are not paid until the funds are withdrawn in the future, allowing the balance to grow faster.

- Lump Sum Distribution

- A one-time payment for the entire balance of a retirement account, rather than receiving the funds in smaller installments over a period of time.

- Consolidation Account

- A specific type of financial account where small retirement balances are held and managed, often used to prevent small amounts from being lost or forgotten.

- Small Amount Threshold

- The specific dollar limit, often $5,000 or $7,000, that allows a retirement plan to process a payout or rollover without the participant's active consent if they do not make a choice.