Fill out dwelling fire forms

with AI.

Dwelling fire forms are standardized documents used in the property insurance industry to apply for and manage coverage on residential properties. Unlike homeowners insurance, dwelling fire policies are specifically designed for properties that may not qualify for standard homeowners coverage — such as rental homes, vacant properties, seasonal residences, or older homes. These forms capture the detailed information insurers need to evaluate risk, determine appropriate coverage limits, and issue policies that protect against fire, lightning, and other specified perils.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About dwelling fire forms

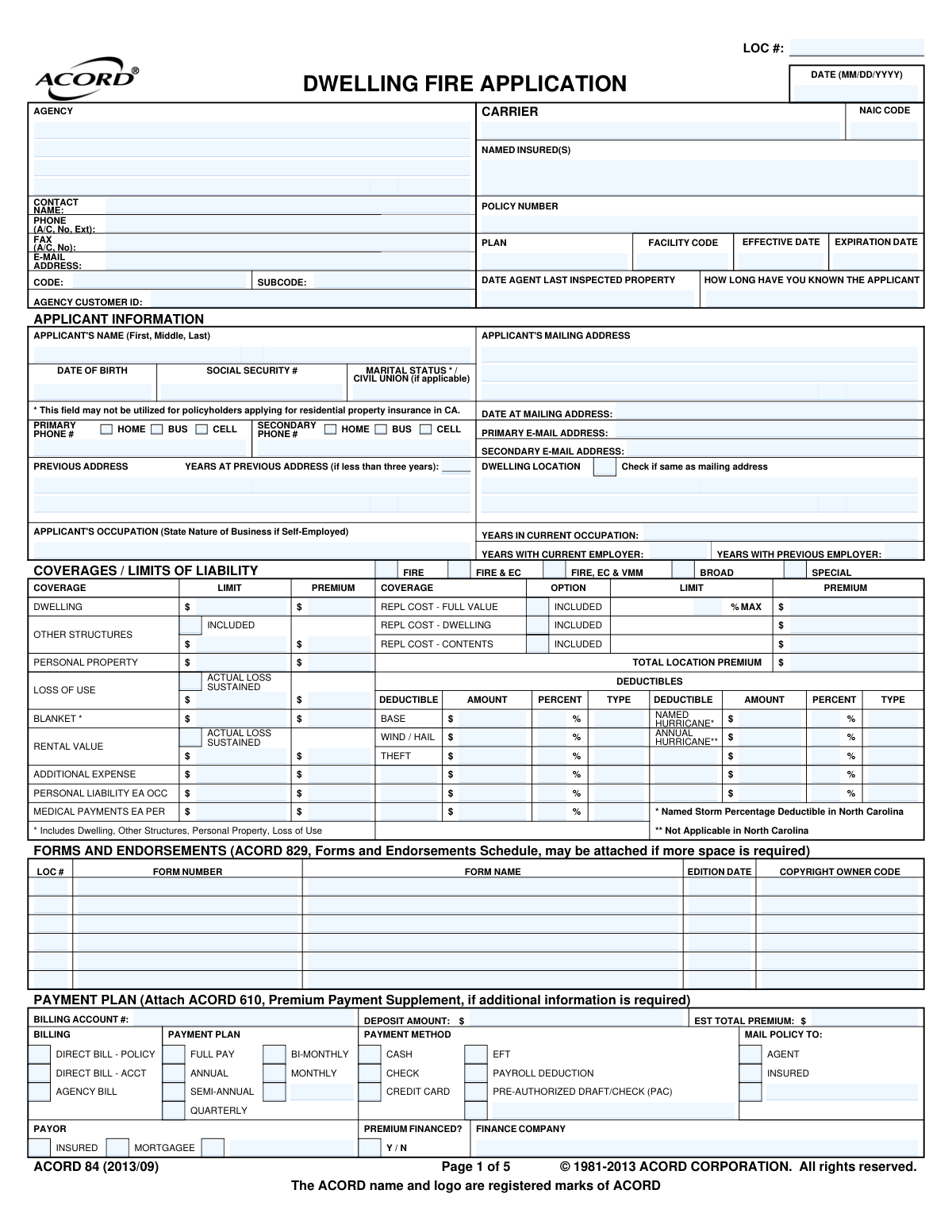

The most widely used form in this category is the ACORD 84 Dwelling Fire Application, a standardized document recognized across the insurance industry. It's typically completed by property owners, landlords, real estate investors, or their insurance agents when applying for a new dwelling fire policy or modifying existing coverage. The form requires detailed information about the property's construction, condition, occupancy, loss history, and desired coverage — all of which underwriters use to assess risk and finalize policy terms.

Filling out these forms accurately is important, as errors or omissions can delay policy issuance or affect coverage. Tools like Instafill.ai use AI to complete dwelling fire forms in under 30 seconds, handling the data accurately and securely — a practical time-saver for agents and property owners managing multiple applications.

Forms in This Category

The forms in this category have a median Form Complexity Index of 78/100 (Complex), measured across 1 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

| Form Name | Pages | FCI | |

|---|---|---|---|

| 1. | ACORD 84, Dwelling Fire Application (2013/09) | 5 | Complex 78 |

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

With only one form in this category, the decision is straightforward — but it's worth understanding exactly what this form covers and whether it's the right fit for your situation.

Who Should Use the ACORD 84 Dwelling Fire Application?

The ACORD 84, Dwelling Fire Application (2013/09) is the standard form for applying for dwelling fire insurance coverage. It's the right choice if you need coverage for:

- Single-family homes — including primary residences, vacation homes, or rental properties

- Apartments and condominiums — for owners seeking fire and related hazard protection

- Co-ops — where the unit owner needs their own dwelling fire policy

What This Form Covers

The ACORD 84 is a comprehensive application that gathers everything an underwriter needs, including:

- Applicant and property details — ownership, location, and property type

- Construction and condition information — roof age, building materials, and overall property condition

- Coverage selections — limits, deductibles, and optional endorsements

- Loss history — prior claims that may affect underwriting decisions

- Billing and payment arrangements

Is This Form Right for You?

- ✅ Use the ACORD 84 if you're applying for a new dwelling fire policy or need to provide a completed application to your insurance agent or carrier.

- ❌ If you're looking for a homeowners policy (which includes liability coverage), you'll likely need a different ACORD form, such as the ACORD 80 or ACORD 85 series.

- ❌ If you need commercial property coverage, this form does not apply — look for commercial lines applications instead.

Tip for Filling It Out

The ACORD 84 can be detailed and time-consuming in its paper format. Using an AI-powered tool like Instafill.ai can help you complete it accurately and quickly, even if you're working from a non-fillable PDF version.

Form Comparison

| Form | Purpose | Who Files It | When to Use |

|---|---|---|---|

| ACORD 84, Dwelling Fire Application (2013/09) | Apply for dwelling fire insurance on residential properties | Applicants, agents, or brokers seeking coverage | When insuring homes, apartments, condos, or co-ops |

Tips for dwelling fire forms

Before filling out a dwelling fire application like the ACORD 84, have key property information on hand — including the year built, construction type (frame, masonry, etc.), square footage, and roof age. Missing or estimated details can slow down underwriting or lead to inaccurate coverage quotes. Being prepared upfront prevents multiple rounds of back-and-forth with your insurer.

Dwelling fire applications require a detailed loss history, typically covering the past three to five years. Inaccurate or incomplete loss history is one of the most common reasons applications are delayed or denied. Request a CLUE (Comprehensive Loss Underwriting Exchange) report ahead of time so you have exact dates, claim types, and payout amounts ready.

One of the most frequent mistakes on dwelling fire forms is entering coverage limits that don't reflect the property's actual replacement cost. Make sure the dwelling coverage amount is based on a current replacement cost estimate, not the market value or purchase price. Also confirm that deductible selections match what the property owner can realistically afford out of pocket.

AI-powered tools like Instafill.ai can fill out dwelling fire application forms like the ACORD 84 quickly and accurately, saving significant time — especially when handling multiple properties or clients. The platform keeps your data secure throughout the process and can even convert non-fillable PDF versions into interactive forms. It's a practical time-saver for agents, brokers, and property owners alike.

Dwelling fire forms often include optional endorsements for coverage like liability, theft, or additional living expenses — but not all endorsements are available in every state or for every property type. Review each endorsement option with the insured to ensure they understand what is and isn't included in their base policy. Overlooking this step can leave property owners with unexpected coverage gaps.

Dwelling fire policies cover specific property types — typically non-owner-occupied rentals, seasonal homes, or properties that don't qualify for a standard homeowners policy. Misclassifying the property or applicant (e.g., submitting as owner-occupied when it's a rental) can result in a voided policy or denied claim. Confirm the intended use of the property before selecting coverage options.

Always save a completed copy of your dwelling fire application before submitting it to the insurer. This creates a clear record of what was disclosed at the time of application, which can be critical if a coverage dispute arises later. Organize copies by property address and policy effective date for easy retrieval.

Dwelling fire applications include a section for billing arrangements, and errors here can lead to policy lapses if payments aren't routed correctly. Clarify whether the premium will be paid directly by the insured, through an escrow account, or by a mortgage company before submitting. Getting this right the first time avoids cancellation notices and reinstatement fees.

Frequently Asked Questions

Dwelling fire forms are used to apply for insurance coverage that protects residential properties against fire and related perils. They collect information about the property, the applicant, and desired coverage so that insurers can assess risk and issue an appropriate policy.

The ACORD 84 is a standardized form used across the insurance industry to apply for dwelling fire policies. It covers residential properties such as single-family homes, apartments, condominiums, and co-ops, and captures details about the property's construction, condition, coverage limits, and loss history.

Property owners, landlords, or renters seeking fire insurance coverage on a residential property typically need to complete a dwelling fire application. Insurance agents and brokers also use these forms on behalf of their clients when submitting applications to insurers.

A dwelling fire policy primarily covers the structure of a residential property against fire and specific named perils, while a homeowners policy typically provides broader coverage including personal liability and personal property. Dwelling fire policies are commonly used for rental properties or vacant homes where a standard homeowners policy may not apply.

You will generally need details about the property's physical characteristics (construction type, roof age, square footage), the applicant's contact and ownership information, desired coverage limits and deductibles, any optional endorsements, and prior loss history. Having mortgage or lienholder information on hand is also helpful.

Completed dwelling fire applications are typically submitted to your insurance agent, broker, or directly to the insurance carrier you are applying with. The insurer's underwriting department will review the form to assess risk and determine policy terms.

ACORD forms are widely recognized standardized documents used throughout the insurance industry, and most carriers accept them. However, some insurers may have their own proprietary forms or supplemental requirements, so it is advisable to confirm with your specific insurer.

Yes, AI-powered tools like Instafill.ai can fill out dwelling fire forms such as the ACORD 84 in under 30 seconds by accurately extracting and placing data from your source documents. These tools can also convert non-fillable PDF versions into interactive fillable forms, making the process faster and less error-prone.

Manually completing a dwelling fire application can take anywhere from 15 to 30 minutes depending on how much property and coverage information you have readily available. Using an AI-powered service like Instafill.ai, the form can be populated in under 30 seconds by automatically extracting relevant data from your documents.

A single dwelling fire application form like the ACORD 84 is generally completed for one property at a time. If you need coverage for multiple properties, a separate application would typically be required for each location.

Dwelling fire policies can cover a range of residential property types, including single-family homes, duplexes, apartments, condominiums, and co-ops. These policies are especially common for non-owner-occupied properties such as rental homes or seasonal residences.

The ACORD 84 is the primary application form for dwelling fire coverage, but depending on your insurer and situation, you may also need supplemental forms for specific endorsements, additional coverages, or unique property characteristics. Your insurance agent can advise you on any additional documentation required.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 78/100 (Complex). See exactly how it is calculated.

- Dwelling Fire Policy

- A type of property insurance that covers a residential structure (and sometimes its contents) against fire and other specified perils. Unlike a standard homeowners policy, it typically offers more limited coverage and is commonly used for rental properties, vacant homes, or secondary residences.

- ACORD

- Association for Cooperative Operations Research and Development — an insurance industry standards organization that creates standardized forms used by insurers, agents, and brokers to streamline data collection and processing across the industry.

- Underwriting

- The process by which an insurance company evaluates the risk of insuring a property and determines whether to issue a policy and at what premium. Information collected on the dwelling fire application is used by underwriters to make this assessment.

- Named Perils

- A coverage structure in which the insurance policy only protects against specific risks (perils) explicitly listed in the policy, such as fire, lightning, or windstorm. Dwelling fire policies are often written on a named perils basis.

- Endorsement

- An optional add-on or modification to a standard insurance policy that expands, restricts, or clarifies coverage. On the ACORD 84 form, applicants can select endorsements to customize their dwelling fire coverage beyond the base policy.

- Coverage Limit

- The maximum dollar amount an insurance company will pay for a covered loss under a policy. Applicants must specify coverage limits for the dwelling structure and any additional coverages when completing a dwelling fire application.

- Deductible

- The amount the policyholder must pay out of pocket before the insurance company begins covering a claim. Higher deductibles typically result in lower premium costs.

- Loss History

- A record of prior insurance claims filed by the applicant or associated with the property, typically covering the past three to five years. Insurers use loss history to assess risk and determine eligibility and pricing.

- Replacement Cost Value (RCV)

- The cost to repair or rebuild a damaged structure using materials of similar kind and quality at current prices, without deducting for depreciation. This is a common basis for setting coverage limits on dwelling fire policies.

- Actual Cash Value (ACV)

- The value of a property or item at the time of loss, calculated as replacement cost minus depreciation. Policies written on an ACV basis typically pay out less than RCV policies in the event of a claim.