Fill out Keogh plan forms

with AI.

Keogh plans, also known as HR-10 plans, are specialized retirement savings vehicles designed specifically for self-employed individuals and owners of unincorporated businesses. Managing these accounts requires specific documentation to ensure compliance with IRS regulations and to maintain the tax-advantaged status of the funds. These forms are essential for administrative tasks ranging from initial plan setup and annual maintenance to complex distribution requests. Because Keogh plans often allow for higher contribution limits than standard IRAs, maintaining accurate records and submitting the correct paperwork is vital for both long-term financial security and accurate tax reporting.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About Keogh plan forms

Typically, these forms are utilized by independent contractors, freelancers, and small business consultants who want to maximize their retirement savings while managing their business's financial health. You might find yourself needing these documents when you need to update your plan details or when you are ready to access your savings. For example, documents such as Form F10110 are used to facilitate cash withdrawals or to roll over funds into different investment vehicles. Navigating these requirements can be time-consuming, especially when dealing with specific institutional requirements that demand precise data entry for successful processing.

To simplify this administrative burden, tools like Instafill.ai use AI to fill these forms in under 30 seconds, ensuring that your data is handled accurately and securely. This technology eliminates the frustration of manual entry and helps you avoid errors, allowing you to manage your retirement documentation efficiently without the usual paperwork stress.

Forms in This Category

| Form Name | Pages | FCI | |

|---|---|---|---|

| 1. | Form F10110, Cash Withdrawal From Your Keogh Plans | 1 | – |

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Navigating retirement distributions for self-employed individuals requires precision to avoid tax penalties and processing delays. If you hold a Keogh plan (also known as an HR-10 plan) through TIAA, selecting the correct paperwork is the first step toward accessing your retirement savings.

Accessing Your Retirement Savings

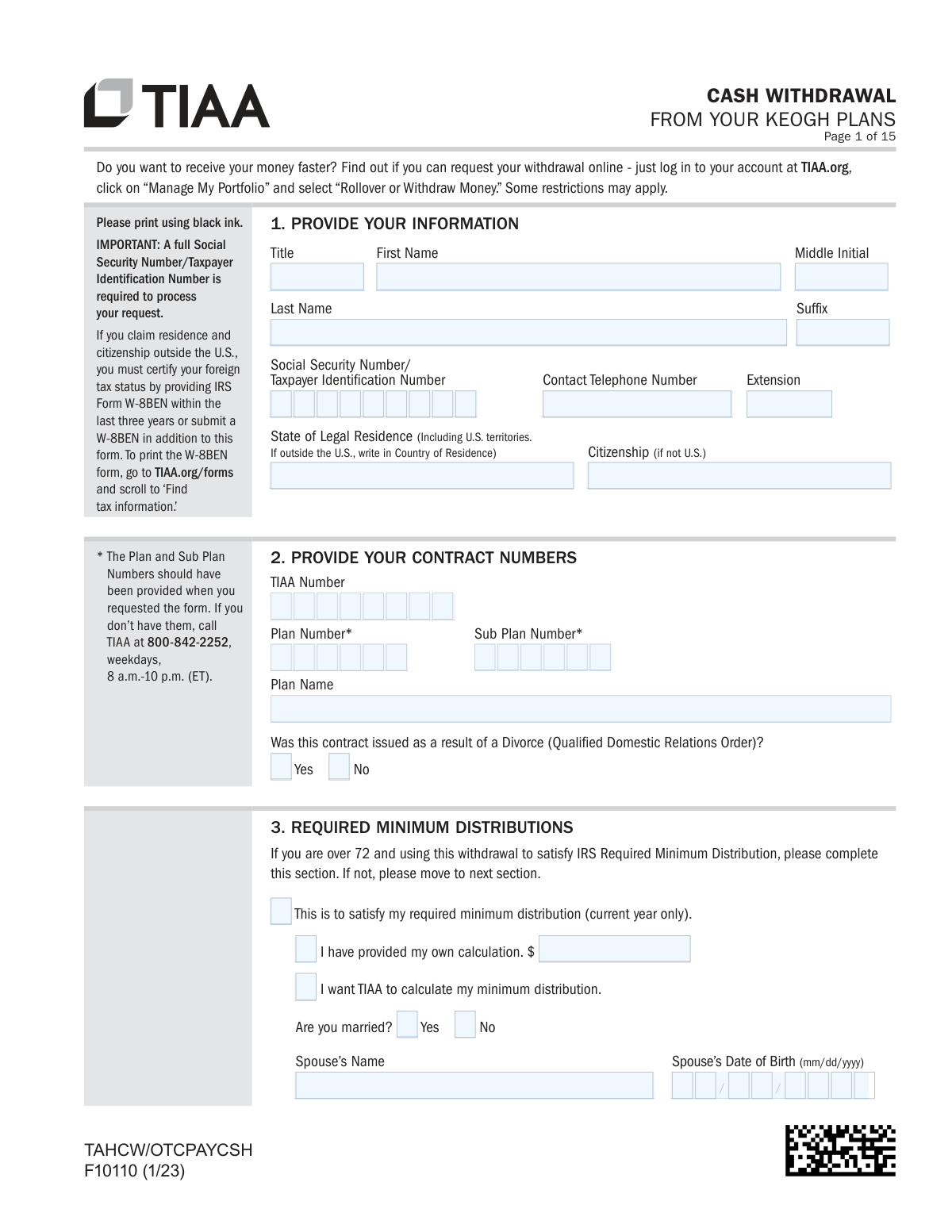

The primary document for this category is Form F10110, Cash Withdrawal From Your Keogh Plans. You should select this form if you are a participant in a TIAA-managed Keogh plan and are ready to initiate a distribution. This single document handles various types of payouts, making it the central tool for managing your plan's liquidity.

Selecting Your Distribution Method

When completing Form F10110, you must identify which withdrawal strategy fits your current financial needs. The form is designed to accommodate three main scenarios:

- Lump Sum Withdrawal: Choose this if you want to withdraw the entire balance of your Keogh plan in one transaction.

- Partial Withdrawal: Use this option if you only need a specific dollar amount while keeping the remainder of your funds invested for future growth.

- Systematic Payments: Select this if you prefer to establish a recurring payment schedule, providing a steady stream of income over time.

Directing Your Funds and Managing Taxes

Beyond just requesting money, Form F10110 allows you to specify the destination of your funds. You can use it to transfer money to a personal bank account, move it to another internal TIAA account, or perform a rollover to a different investment firm to maintain the tax-advantaged status of your savings.

Because Keogh distributions are generally taxable events, it is vital to fill out the tax withholding sections accurately. Using Instafill.ai to complete this form ensures that critical data like account numbers and distribution codes are clearly legible, which helps prevent the form from being rejected by plan administrators.

Form Comparison

| Form | Purpose | Who Files It | Distribution Options | Key Requirements |

|---|---|---|---|---|

| Form F10110, Cash Withdrawal From Your Keogh Plans | Requesting a cash distribution or withdrawal from a TIAA Keogh retirement plan. | Keogh plan participants who need to access their invested retirement funds. | Offers lump sum payments, partial withdrawals, or recurring systematic payment schedules. | Requires specifying payment destination and selecting federal and state tax withholding options. |

Tips for Keogh plan forms

Keogh plan distributions are generally subject to federal and state income taxes. Before submitting your withdrawal request, ensure you have selected the appropriate withholding percentage to avoid potential underpayment penalties during tax season.

If you intend to move your funds to another retirement account without paying taxes, ensure you select the direct rollover option. Taking a cash distribution instead of a rollover may trigger immediate tax liabilities and potential early withdrawal penalties.

Managing complex retirement paperwork can be tedious, but AI-powered tools like Instafill.ai can complete these forms in under 30 seconds with high accuracy. Your sensitive data stays secure during the process, making it a highly efficient way to handle multiple distribution requests.

To avoid significant delays in receiving your funds, verify that your bank's routing and account numbers are entered correctly for electronic transfers. Even a single digit error can cause the transaction to fail, requiring a lengthy manual correction process with the plan administrator.

Keogh plans are specifically designed for self-employed individuals and small businesses, so you must accurately provide the plan name and number. Referencing your most recent plan statement can help ensure these identification details match the administrator's records exactly.

Decide whether you need a one-time lump sum or a series of systematic payments before you begin the form. Selecting systematic payments can provide a steady income stream while keeping the remainder of your Keogh balance invested for continued growth.

Always save a digital or physical copy of your signed distribution request before submitting it to the plan administrator. Having a record of your specific instructions is essential for resolving any future discrepancies regarding the amount or timing of your withdrawal.

Frequently Asked Questions

A Keogh plan is a tax-deferred pension plan available to self-employed individuals or unincorporated businesses for retirement purposes. It functions similarly to a 401(k) but is specifically designed for those who work for themselves or own a small business.

These forms are used by self-employed individuals, freelancers, and small business owners who have established a Keogh retirement account. Employees of these small businesses may also be eligible to use these forms if their employer has established the plan on their behalf.

Withdrawal forms are typically used when a participant reaches retirement age, experiences a qualifying financial hardship, or decides to roll over funds into another qualified retirement account. They are necessary to legally authorize the movement or distribution of funds out of the plan.

Yes, Keogh plans generally fall into two categories: defined-benefit plans and defined-contribution plans. While the withdrawal forms may look similar, the contribution limits and calculation of benefits differ depending on which type of plan was established.

When submitting withdrawal forms, you may need to provide proof of identity, bank account details for electronic transfers, and tax identification numbers. Depending on the specific institution, additional documentation regarding your retirement status or hardship may be requested.

In most cases, distributions from a Keogh plan are treated as taxable income in the year they are received. If a withdrawal is made before the age of 59½, an additional 10% federal tax penalty may apply unless a specific IRS exception is met.

Completed forms should be submitted directly to the financial institution or plan administrator managing the account, such as TIAA. Many administrators offer secure online portals for digital submission, though some may still require physical mail for certain types of distributions.

Yes, you can fill out Keogh plan forms using AI tools like Instafill.ai. These tools accurately extract data from your source documents and place it into the required fields, which helps ensure the form is completed correctly and ready for submission to your plan administrator.

Using AI-powered services, filling out Keogh plan forms online usually takes under 30 seconds. This process automates manual data entry, significantly reducing the time required to prepare the document while minimizing the risk of errors that could delay your distribution.

If you wish to change from a lump sum to systematic payments or vice versa, you will generally need to file a new withdrawal or amendment form. It is important to contact your plan administrator to see which specific form is required to update your payment preferences.

Glossary

- Keogh Plan (H.R. 10 Plan)

- A tax-deferred retirement savings plan designed for self-employed individuals and unincorporated businesses. These plans allow for higher contribution limits than traditional IRAs but come with more complex reporting requirements.

- Distribution

- The official withdrawal of funds from a retirement account. Distributions can be taken in various forms, including one-time payments or recurring installments, and are generally subject to income tax.

- Direct Rollover

- A transaction where retirement funds are moved directly from your Keogh plan to another eligible retirement plan or IRA. This method is used to avoid immediate tax liabilities and the mandatory 20% federal withholding.

- Tax Withholding

- The portion of a withdrawal that is sent directly to the IRS as a payment toward your federal income tax. For many retirement distributions, the law requires a mandatory 20% withholding unless the funds are rolled over.

- Systematic Payments

- A distribution option that allows you to receive regular, scheduled payments from your account over a set period. This provides a steady income stream rather than a single large payment.

- Lump-Sum Distribution

- A single payment representing the entire balance or a specific fixed amount from your retirement plan. Choosing this option may result in a higher tax burden for the year the funds are received.

- Qualified Domestic Relations Order (QDRO)

- A legal order, typically resulting from a divorce, that grants a person the right to a portion of their former spouse's retirement plan assets. This must be submitted to the plan administrator to authorize a payout to a non-participant.

- Participant

- The individual who is covered by the Keogh plan and has accumulated savings within the account. The participant is typically the person authorized to request withdrawals or designate beneficiaries.