Compliance 1099-NEC

Validation Checks by Instafill.ai

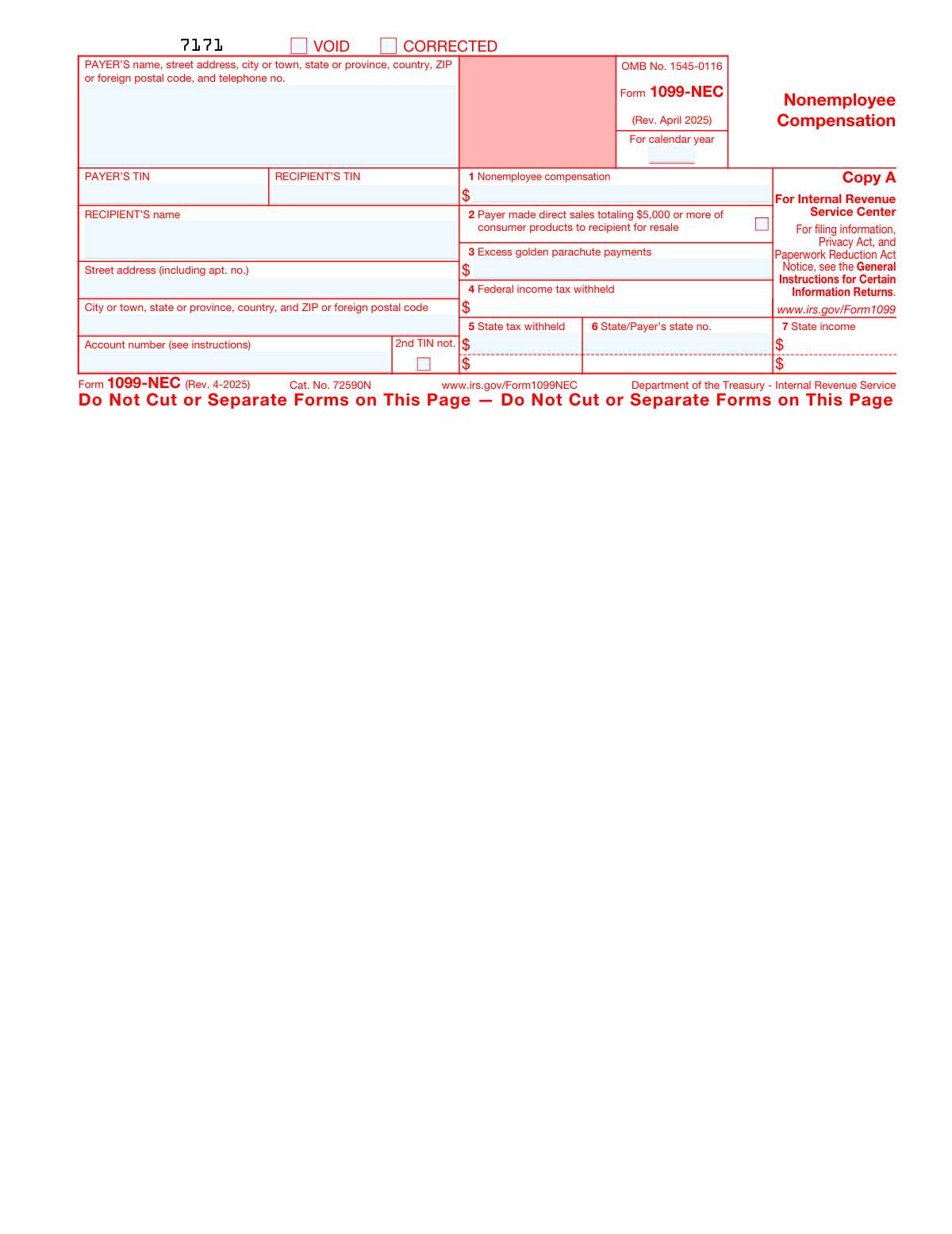

1

Ensures Payer's TIN is in a Valid Format

The Payer's TIN must be entered in a recognized IRS format: either a 9-digit Employer Identification Number (EIN) formatted as XX-XXXXXXX or a Social Security Number (SSN) formatted as XXX-XX-XXXX. This field is required and cannot be left blank, as it uniquely identifies the payer to the IRS. If the TIN is missing, incorrectly formatted, or contains non-numeric characters, the form will be rejected and may result in penalties for the payer.

2

Ensures Recipient's TIN is in a Valid Format

The Recipient's TIN must conform to a valid IRS-recognized format, including SSN (XXX-XX-XXXX), EIN (XX-XXXXXXX), ITIN (9XX-XX-XXXX), or ATIN. This field is required for proper IRS matching and tax reporting. An invalid or missing Recipient TIN may trigger backup withholding requirements and could result in IRS penalties for the payer for failing to obtain and report a correct TIN.

3

Ensures Box 1 Nonemployee Compensation is a Non-Negative Numeric Value

Box 1 (Nonemployee Compensation) must contain a valid non-negative dollar amount with no more than two decimal places, and must not include alphabetic characters or special symbols other than a decimal point. This is the primary reportable amount on Form 1099-NEC and is required when total payments to the recipient meet or exceed $600 for the tax year. A missing, negative, or non-numeric value in this field will cause the form to fail IRS processing and may result in underreporting penalties.

4

Ensures Tax Year is a Valid Calendar Year

The calendar year field must contain a valid four-digit year (e.g., 2024 or 2025) that corresponds to the tax year for which compensation is being reported. The year must not be a future year beyond the current filing period, nor an implausibly historical year. An incorrect or missing tax year will cause the IRS to be unable to match the filing to the correct tax period, potentially resulting in misapplied credits or penalties for both the payer and recipient.

5

Ensures VOID and CORRECTED Checkboxes Are Not Both Selected Simultaneously

The VOID and CORRECTED checkboxes are mutually exclusive: a form cannot be both voided and corrected at the same time, as these statuses represent fundamentally different actions. VOID indicates the form should be disregarded entirely, while CORRECTED indicates it replaces a previously filed form with updated information. If both are checked simultaneously, the IRS cannot determine the intended status of the form, which may lead to processing errors or duplicate reporting issues.

6

Ensures State Tax Withheld Fields Require Corresponding State Identification Number

If a value is entered in Box 5 (State tax withheld) or State 1/State 2 tax withheld fields, the corresponding Box 6 (State/Payer's state no.) or State 1/State 2 state identification number must also be populated. The IRS and state tax authorities require the payer's state ID to properly route and credit state withholding amounts. Reporting state tax withheld without a corresponding state ID number will cause state tax reconciliation failures and may result in the recipient being unable to claim the withheld amount on their state return.

7

Ensures State Income Fields Are Only Populated When State Tax Withheld Is Present

The State 1 and State 2 income fields (Box 7) should only be filled when the corresponding state tax withheld (Box 5) fields contain a value, as state income reporting is contingent on there being a state withholding relationship. Populating state income without a corresponding state tax withheld amount or state ID creates an inconsistent record that may confuse state tax authorities. This check prevents orphaned state income entries that lack the required supporting withholding and identification data.

8

Ensures Payer's Name and Address Fields Are Fully Populated

The Payer's name, street address, city, state, ZIP code, and telephone number fields must all be present and non-empty, as this information is required for the IRS to identify and contact the filing entity. The address must include at minimum a street address, city, state or province, and ZIP or postal code. Missing or incomplete payer address information can result in the IRS being unable to process the form or contact the payer for corrections, potentially leading to penalties.

9

Ensures Recipient's Name is Populated and Not Abbreviated

The Recipient's name field must contain the full legal name of the individual or business entity as it appears on their tax records, and must not be left blank or contain only initials or abbreviations. The IRS uses the recipient's name in combination with their TIN to match the 1099-NEC to the correct tax return. An abbreviated, incomplete, or missing recipient name increases the risk of TIN/name mismatch errors, which can trigger IRS notices and backup withholding requirements.

10

Ensures Federal Income Tax Withheld is a Non-Negative Numeric Value

Box 4 (Federal income tax withheld) must contain a valid non-negative dollar amount if populated, representing backup withholding applied to the recipient's payments. This field should only contain a value if backup withholding was actually applied, and must not be negative or contain non-numeric characters. An erroneous or negative value in this field could cause the recipient to incorrectly claim a tax credit they are not entitled to, and may trigger IRS discrepancy notices.

11

Ensures Excess Golden Parachute Payments is a Non-Negative Numeric Value When Populated

Box 3 (Excess golden parachute payments) must contain a valid non-negative dollar amount if entered, as this represents compensation subject to a 20% excise tax under IRS rules. The field should be left blank rather than entered as zero if no such payments were made, to avoid confusion with intentional zero-dollar reporting. A negative or non-numeric value in this field will cause processing errors and may incorrectly trigger excise tax calculations for the recipient.

12

Ensures Recipient's Address Fields Are Sufficiently Complete

The recipient's street address and city/state/ZIP fields must both be populated with meaningful content to ensure the form can be delivered to the recipient and properly processed. A ZIP or postal code, where applicable, should conform to the standard 5-digit (or 5+4) U.S. format or an appropriate foreign postal code format. Missing or incomplete recipient address information prevents the payer from fulfilling their obligation to furnish a copy of the form to the recipient, which is required by IRS regulations.

13

Ensures the Direct Sales Checkbox (Box 2) Does Not Require a Dollar Amount Entry

Box 2 is a checkbox field only, indicating that direct sales of consumer products totaling $5,000 or more were made to the recipient for resale; it does not require or accept a specific dollar amount. Validation should confirm that no numeric dollar value is entered in association with Box 2, as the IRS form design intentionally uses a checkbox rather than a monetary field for this indicator. Entering a dollar amount where only a checkbox is expected may cause form parsing errors or misinterpretation of the reported data.

14

Ensures Second State Reporting Fields Are Only Populated When First State Fields Are Complete

The State 2 fields (State 2: Tax withheld, State 2: State/Payer's state no., and State 2: State income) should only be populated if the State 1 fields are already fully completed, as the form is designed to report a primary state first before a secondary state. Populating State 2 fields while leaving State 1 fields blank creates an illogical reporting sequence that may confuse state tax authorities and cause reconciliation errors. This check enforces the proper sequential completion of multi-state withholding information.

15

Ensures Payer's Telephone Number is in a Valid Format

The payer's telephone number must be entered in a recognizable format, such as (XXX) XXX-XXXX or XXX-XXX-XXXX for domestic numbers, and must contain the correct number of digits without letters or invalid special characters. A valid telephone number is required so that the IRS or state tax authorities can contact the payer if there are questions about the filing. An improperly formatted or missing telephone number may delay resolution of any discrepancies identified by the IRS during processing.

16

Ensures Nonemployee Compensation Meets the $600 Reporting Threshold When Box 1 Is Populated

When Box 1 (Nonemployee Compensation) is populated, the amount entered should generally be $600 or more, as the IRS requires Form 1099-NEC to be filed only when total payments to a nonemployee recipient meet or exceed this threshold during the tax year. Amounts below $600 in Box 1 may indicate a data entry error or an unnecessary filing, though certain exceptions (such as backup withholding) may apply. This check flags potentially below-threshold entries for review to ensure the form is being filed appropriately and to prevent unnecessary or erroneous submissions.