Yes! You can use AI to fill out Form 5472 (Rev. December 2023), Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business

| Fillable fields | 144 |

| Pages | 3 |

| Fields per page | 48 |

| Sections | 68 |

| Conditional rules | 56 |

| Tables & lists | 2 |

| Instruction pages | — |

| OMB Control No. | 1545-0123 |

| Instafill Form ID | IF-FORM-5472-REV-DECEMBER-2023-INFORMATION-RETURN-OF |

Form specifications

| Form name: | Form 5472 (Rev. December 2023), Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business |

| Number of fields: | 144 |

| Number of pages: | 3 |

| FCI: | Complex (78/100) |

| Field instructions: | Form 5472 Instructions |

| Filled form examples: | Form 5472 Examples |

| Language: | English |

Instafill Demo: How to fill out PDF forms in seconds with AI

How to Fill Out Form 5472 Online for Free in 2026

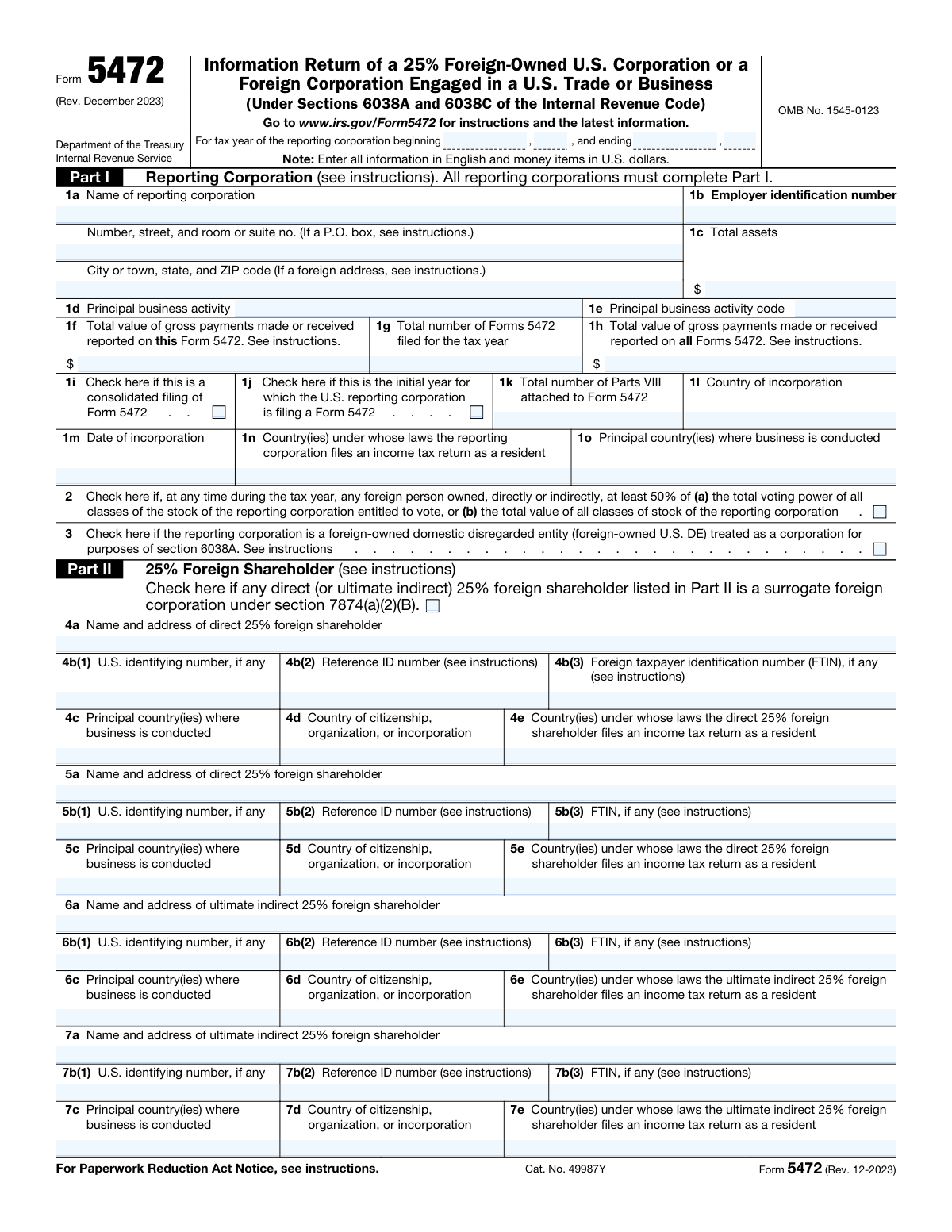

- 1 Enter the tax year covered and complete Part I with the reporting corporation’s legal name, address, EIN, total assets, business activity/code, incorporation details, and totals for gross payments and number of Forms 5472 filed.

- 2 Complete Part II by listing each direct and ultimate indirect 25% foreign shareholder, including names/addresses, U.S. identifying number or reference ID, FTIN (if any), and countries of incorporation/residency and where business is conducted.

- 3 Complete Part III by identifying the related party involved in the reportable transactions, indicating whether the related party is a foreign person or U.S. person, and providing identifying numbers, business activity/code, relationship checkboxes, and residency/business countries.

- 4 If the related party is foreign, complete Part IV by entering U.S.-dollar amounts for each category of monetary transactions (receipts and payments), including inventory/property sales and purchases, services, rents/royalties, intangibles, loans/interest, insurance, guarantees, and other amounts, then total the sections.

- 5 If applicable, complete Parts V and VI by attaching required statements describing other reportable transactions for a foreign-owned U.S. disregarded entity and any nonmonetary or less-than-full-consideration transactions, and check the corresponding boxes.

- 6 Answer Part VII additional information questions (imports, cost sharing participation, section 267A disallowed interest/royalty, FDII-related amounts, safe-haven interest rate loans, and covered debt instrument questions) and complete a separate Part VIII for each cost sharing arrangement if required.

- 7 If applicable, complete Part IX for base erosion payments and tax benefits under section 59A, then review for consistency, ensure all required attachments are included, and file Form 5472 with the reporting corporation’s income tax return (or as required for foreign-owned U.S. disregarded entities).

Our AI-powered system ensures each field is filled out correctly, reducing errors and saving you time.

Why Choose Instafill.ai for Your Fillable Form 5472 Form?

Speed

Complete your Form 5472 in as little as 37 seconds.

Up-to-Date

Always use the latest 2026 Form 5472 form version.

Cost-effective

No need to hire expensive lawyers.

Accuracy

Our AI performs 10 compliance checks to ensure your form is error-free.

Security

Your personal information is protected with bank-level encryption.

Frequently Asked Questions About Form 5472

Form 5472 has a Form Complexity Index of 78 out of 100, placing it in the complex complexity tier. This score is calculated deterministically from the form’s own structure using Instafill’s published Form Complexity Index methodology, so it can be reproduced and independently verified — it is not a subjective estimate.

For Form 5472 specifically, the score reflects 144 fillable fields across 3 pages, grouped into 68 sections, and 56 conditional fields that only apply depending on earlier answers, 2 tables or repeating lists. The number of fields is the largest factor in the base score (weighted 36%), followed by how difficult those fields are to complete based on their type, where free-text and signature fields count for more than simple checkboxes (26%). The number of pages that actually contain fields (15%), the amount of conditional “fill-only-if” logic (16%), and how many sections the form is divided into (7%) account for the rest of the base. On top of that base, the index adds points for tables and repeating lists, bundled instruction pages, and dense page layouts — capturing difficulty the base alone can miss.

In practical terms, a complex score means the form is demanding, with many fields, multiple pages and branching rules that are easy to get wrong. Instafill removes that effort entirely: our AI reads your information, maps each value to the correct field — including the conditional ones — and completes Form 5472 accurately in under a minute, with every field available for you to review before you download. See exactly how the Form Complexity Index is calculated.

Compliance Form 5472

Validation Checks by Instafill.ai

Common Mistakes in Completing Form 5472

“I was never sure if my IRS forms like W-9 were filled correctly. Now, I can complete the forms accurately without any external help.”

Your data stays secure with advanced protection from Instafill and our subprocessors