Compliance W-9

Validation Checks by Instafill.ai

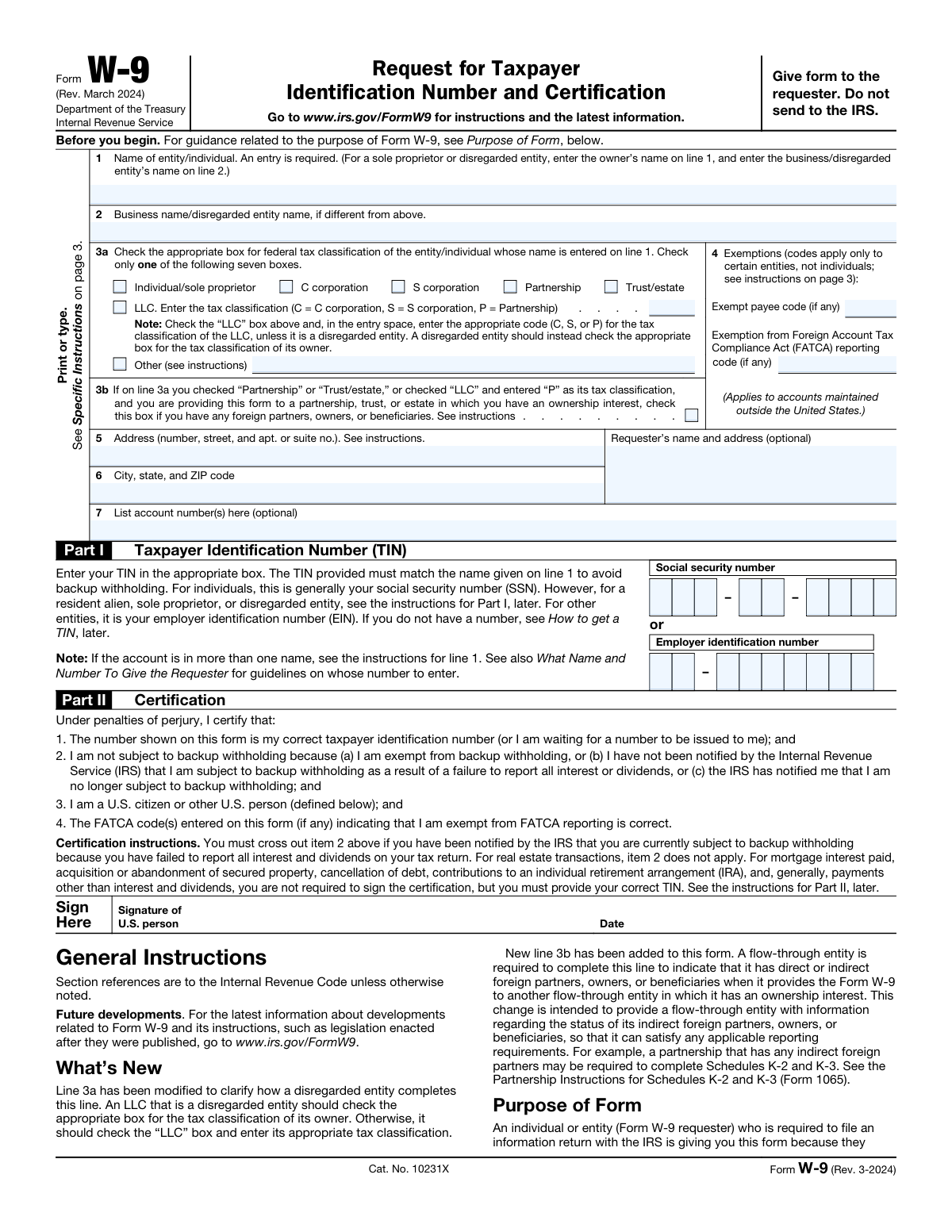

1

Line 1 Name Field Cannot Be Blank

Validates that the Name field on Line 1 is not empty, as the form explicitly states 'An entry is required.' The name entered must match the name shown on the taxpayer's tax return to ensure proper IRS reporting and avoid backup withholding issues. If this field is left blank, the form is considered incomplete and cannot be processed, potentially triggering backup withholding at the 24% rate.

2

Exactly One Federal Tax Classification Box Selected on Line 3a

Validates that one and only one of the seven federal tax classification checkboxes on Line 3a is selected: Individual/sole proprietor, C corporation, S corporation, Partnership, Trust/estate, LLC, or Other. The form explicitly instructs the filer to 'Check only one of the following seven boxes,' and selecting multiple boxes or leaving all boxes unchecked renders the classification ambiguous. Failure to select exactly one box makes the form invalid and prevents the requester from correctly categorizing the payee for tax reporting purposes.

3

LLC Tax Classification Code Is Required When LLC Box Is Checked

Validates that when the LLC checkbox on Line 3a is selected, the adjacent tax classification entry field contains one of the three valid codes: C (C corporation), S (S corporation), or P (Partnership). An LLC that is a disregarded entity should instead check the appropriate box for its owner's tax classification rather than the LLC box. If the LLC box is checked but no valid classification code is entered, the form is incomplete and the requester cannot determine the correct withholding and reporting obligations.

4

Line 3b Foreign Partners Checkbox Conditional Applicability

Validates that Line 3b is only completed when the entity checked Partnership or Trust/estate on Line 3a, or checked LLC and entered 'P' as the tax classification. This checkbox is exclusively for flow-through entities providing the form to another partnership, trust, or estate in which they hold an ownership interest and have foreign partners, owners, or beneficiaries. If Line 3b is checked for an entity type that does not qualify (e.g., a C corporation or individual), it should be flagged as an inconsistency, as incorrect completion may result in erroneous Schedule K-2 and K-3 filing obligations.

5

Other Tax Classification Description Is Required When 'Other' Is Selected

Validates that when the 'Other (see instructions)' checkbox is selected on Line 3a, the accompanying text field for the specific classification description is not left blank. The 'Other' option requires the filer to specify the exact nature of the entity's federal tax classification per the form instructions. Leaving this field empty when 'Other' is checked provides no meaningful classification information to the requester and renders the form incomplete.

6

Mutually Exclusive TIN Entry: SSN or EIN, Not Both

Validates that the filer has provided a Taxpayer Identification Number in only one of the two available fields — either the Social Security Number (SSN) fields or the Employer Identification Number (EIN) fields — but not both simultaneously. The form instructs that individuals generally use an SSN while entities use an EIN, and entering values in both fields creates an ambiguous TIN that cannot be matched to the name on Line 1. If both TIN fields are populated, the form must be rejected or clarified to avoid backup withholding and incorrect IRS reporting.

7

SSN Format Validation: Three Segments Must Form a Complete 9-Digit Number

Validates that when an SSN is provided, all three segments are present and collectively contain exactly 9 numeric digits: the first segment must have 3 digits, the middle segment must have 2 digits, and the final segment must have 4 digits. SSNs must be numeric only and cannot contain letters, spaces, or special characters beyond the standard dashes separating the segments. An incomplete or incorrectly formatted SSN will not match IRS records, triggering backup withholding and potential penalties for furnishing an incorrect TIN.

8

EIN Format Validation: Two Segments Must Form a Complete 9-Digit Number

Validates that when an EIN is provided, both segments are present and collectively contain exactly 9 numeric digits: the prefix segment must have 2 digits and the remaining segment must have 7 digits. EINs must be entirely numeric and cannot contain letters or special characters. An improperly formatted EIN will fail IRS TIN matching, exposing the requester to backup withholding obligations and the payee to a $50 penalty for failure to furnish a correct TIN.

9

TIN Must Be Provided or 'Applied For' Must Be Indicated

Validates that the TIN section is not entirely blank — either a valid SSN or EIN must be entered, or the phrase 'Applied For' must be indicated to signal that a TIN application is pending. Leaving the TIN section completely empty without any indication means the form cannot fulfill its core purpose of providing a correct taxpayer identification number to the requester. A blank TIN will immediately subject the payee to backup withholding at the 24% rate on applicable payments.

10

Exempt Payee Code Must Be a Valid Code (1–13) If Provided

Validates that if an exempt payee code is entered on Line 4, it must be one of the 13 recognized numeric codes (1 through 13) as defined in the form instructions. Individuals and sole proprietors are generally not eligible for an exempt payee code, so the system should flag a potential inconsistency if an exempt payee code is entered alongside an Individual/sole proprietor tax classification on Line 3a. An invalid or inapplicable exempt payee code could result in incorrect withholding treatment and potential IRS penalties.

11

FATCA Exemption Code Must Be a Valid Letter Code (A–M) If Provided

Validates that if a FATCA exemption code is entered on Line 4, it must be one of the 13 recognized letter codes (A through M) as defined in the form instructions. This field is only applicable to accounts maintained outside the United States by certain foreign financial institutions, and entering an invalid code or a code that does not correspond to the entity's actual status constitutes a false certification. An incorrect FATCA code could expose the filer to civil penalties of $500 for false statements and potential criminal penalties for willful falsification.

12

Line 5 Street Address Must Be Present and Properly Formatted

Validates that Line 5 contains a street address including a building or house number, street name, and any applicable apartment or suite number, and that the field is not left blank. The address on Line 5 is where the requester will mail information returns such as 1099 forms, making it critical for the payee to receive their tax documents. An absent or clearly malformed address (e.g., containing only letters with no numeric component) should be flagged to ensure information returns are deliverable.

13

Line 6 City, State, and ZIP Code Must Be Present and Properly Formatted

Validates that Line 6 contains a city name, a valid two-letter U.S. state or territory abbreviation, and a ZIP code consisting of either 5 digits or the ZIP+4 format (5 digits, a hyphen, and 4 digits). All three components — city, state, and ZIP — must be present for the address to be complete and deliverable. A missing or improperly formatted ZIP code or an unrecognized state abbreviation should trigger a validation error, as an incomplete address prevents the requester from mailing required information returns to the payee.

14

Tax Classification and TIN Type Consistency Check

Validates that the type of TIN provided in Part I is consistent with the federal tax classification selected on Line 3a. Specifically, individuals and sole proprietors should generally provide an SSN, while corporations, partnerships, trusts, and estates should provide an EIN; providing an SSN for a corporation or an EIN for an individual (without a valid exception) indicates a likely data entry error. This consistency check helps prevent TIN-to-name mismatches in IRS records that would trigger backup withholding and could indicate an incorrectly completed form.

15

Disregarded Entity Owner Name Consistency on Line 1 vs. Line 2

Validates that when the entity type is a disregarded entity (e.g., a single-member LLC not electing corporate status), the owner's legal name — not the disregarded entity's name — is entered on Line 1, and the disregarded entity's name is placed on Line 2. Entering the disregarded entity's name on Line 1 instead of the owner's name is a common error that causes TIN-to-name mismatches because the TIN must belong to the owner, not the disregarded entity. If the same name appears on both Line 1 and Line 2, or if the Line 1 name appears to be a business entity name while the LLC classification is selected as a disregarded entity, the form should be flagged for review.

16

S Corporation Must Not Enter an Exempt Payee Code for Broker Transactions

Validates that if the S corporation tax classification is selected on Line 3a, no exempt payee code is entered in the exempt payee code field on Line 4, particularly in the context of broker transactions. Per the form instructions, S corporations must not enter an exempt payee code because they are only exempt for sales of noncovered securities acquired prior to 2012, and entering a general exempt payee code would incorrectly signal broader exemption from backup withholding. Flagging this combination prevents incorrect withholding treatment and ensures the requester applies the correct reporting rules for S corporation payees.