Compliance Schedule C

Validation Checks by Instafill.ai

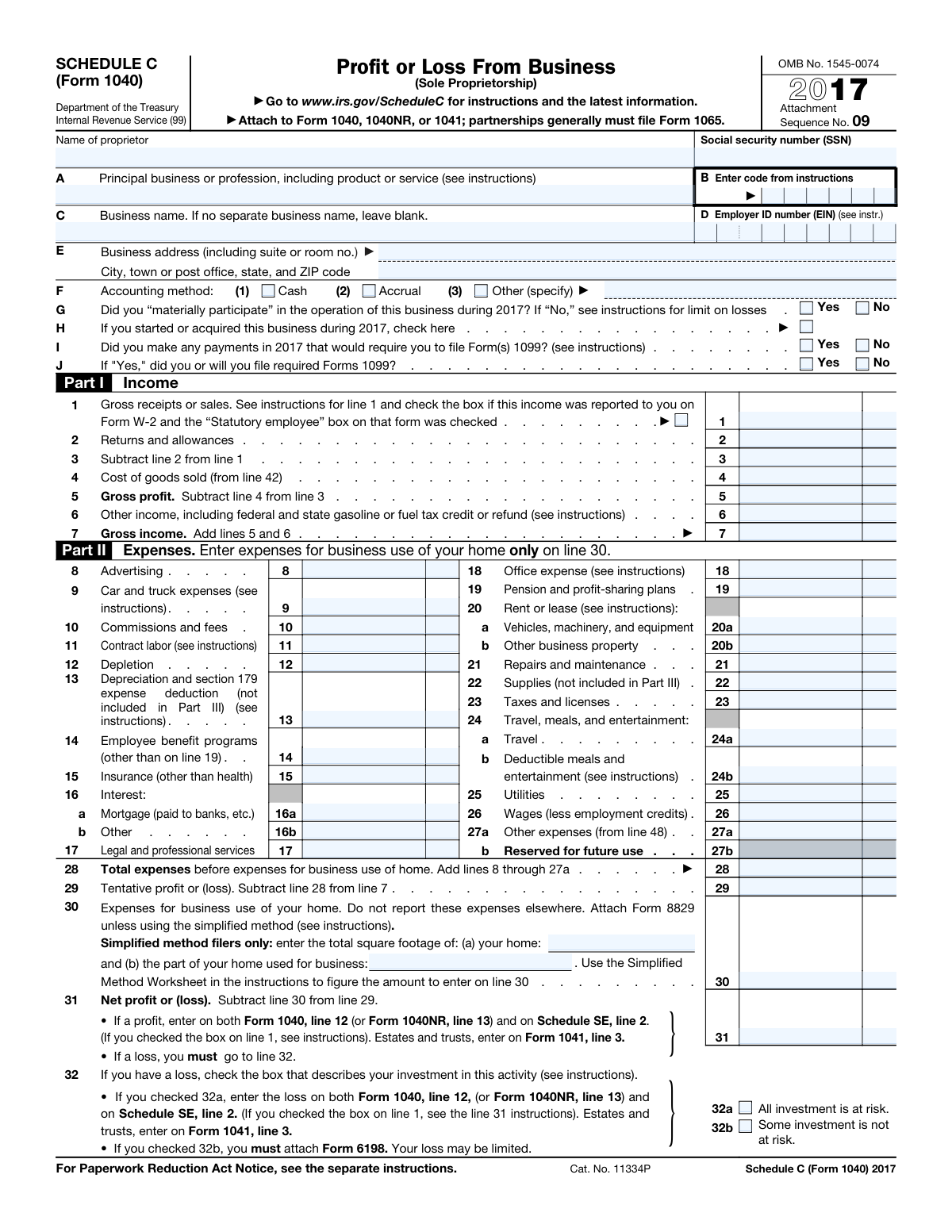

1

Proprietor Social Security Number Format Validation

Validates that the Proprietor Social Security Number (SSN) is entered in the correct 9-digit format (XXX-XX-XXXX) and contains only numeric characters with the appropriate dashes. The SSN is a required field and serves as the primary taxpayer identifier linking Schedule C to the correct Form 1040 filing. If the SSN is missing, incorrectly formatted, or contains non-numeric characters, the form cannot be properly processed by the IRS and may result in filing rejection or misapplication of the tax return.

2

Accounting Method Mutual Exclusivity Check

Ensures that exactly one accounting method is selected among Cash, Accrual, or Other, and that no more than one option is checked simultaneously. If 'Other' is selected, the corresponding text field specifying the method must also be populated with a valid description. Selecting multiple accounting methods or leaving this field blank is invalid because the IRS requires a single, consistent accounting method to be declared for the business. Failure to select exactly one method or to specify the 'Other' method will result in an incomplete and potentially rejected filing.

3

Line 3 Net Receipts Arithmetic Consistency Check

Validates that the value entered on Line 3 (Net Receipts) equals Line 1 (Gross Receipts or Sales) minus Line 2 (Returns and Allowances), including both dollar and cents components. This is a required arithmetic relationship defined explicitly on the form and ensures the income section is internally consistent. If the calculated value does not match the entered value, it indicates a data entry error that could misrepresent the taxpayer's income and trigger an IRS audit or notice.

4

Line 5 Gross Profit Arithmetic Consistency Check

Validates that the value on Line 5 (Gross Profit) equals Line 3 (Net Receipts) minus Line 4 (Cost of Goods Sold), verifying both the dollar and cents portions. This arithmetic relationship is explicitly defined on the form and is critical for accurately representing the business's profitability. An inconsistency between these values suggests a calculation error that could understate or overstate taxable income, potentially resulting in penalties or an IRS inquiry.

5

Line 7 Gross Income Arithmetic Consistency Check

Validates that the value on Line 7 (Gross Income) equals the sum of Line 5 (Gross Profit) and Line 6 (Other Income), including both dollars and cents. This is a fundamental arithmetic check that ensures the total gross income figure used throughout the rest of the form is accurate. If this value is inconsistent with its component lines, all downstream calculations including tentative profit, net profit, and tax liability will be incorrect.

6

Line 28 Total Expenses Summation Validation

Validates that Line 28 (Total Expenses Before Business Use of Home) equals the sum of all individual expense lines 8 through 27a, including advertising, car and truck expenses, commissions, contract labor, depletion, depreciation, employee benefits, insurance, interest, legal services, office expense, pension plans, rent, repairs, supplies, taxes, travel, utilities, wages, and other expenses. This check ensures the total expenses figure is arithmetically correct before it is used to calculate tentative profit or loss. An incorrect total will cascade errors into Lines 29 and 31, ultimately affecting the net profit or loss reported on Form 1040.

7

Line 29 Tentative Profit or Loss Arithmetic Consistency Check

Validates that Line 29 (Tentative Profit or Loss) equals Line 7 (Gross Income) minus Line 28 (Total Expenses), verifying both dollar and cents components. This is a required arithmetic relationship that bridges the income and expense sections of the form. If the tentative profit or loss is inconsistent with its component lines, the final net profit or loss figure on Line 31 will also be incorrect, leading to an inaccurate tax liability on Form 1040.

8

Line 31 Net Profit or Loss Arithmetic Consistency Check

Validates that Line 31 (Net Profit or Loss) equals Line 29 (Tentative Profit or Loss) minus Line 30 (Expenses for Business Use of Home), and that either the Net Profit or Net Loss field is populated but not both. If a loss is reported on Line 31, the form must proceed to Line 32 where the taxpayer must indicate whether all or some investment is at risk. Failure to correctly compute or report this value directly impacts the amount transferred to Form 1040 Line 12 and Schedule SE Line 2, affecting both income tax and self-employment tax calculations.

9

Loss on Line 32 Investment Risk Selection Requirement

Validates that when a net loss is reported on Line 31, exactly one of the two investment risk checkboxes on Line 32 (32a: All investment is at risk, or 32b: Some investment is not at risk) is selected. If 32b is checked, the form must have Form 6198 attached to limit the loss. Leaving Line 32 blank when a loss exists, or checking both boxes, renders the loss reporting incomplete and may result in the IRS disallowing the loss deduction or requiring additional documentation.

10

Form 1099 Filing Consistency Check

Validates that if 'Yes' is selected for Line I (payments requiring Form 1099 were made), then Line J (whether Form 1099 was or will be filed) must also be answered with either 'Yes' or 'No'. Conversely, if 'No' is selected for Line I, then Line J should not be answered. This conditional logic ensures the taxpayer's 1099 filing obligations are fully and consistently disclosed. Leaving Line J blank when Line I is 'Yes' creates an incomplete disclosure that may trigger IRS follow-up.

11

Part IV Vehicle Information Completeness When Car Expenses Claimed

Validates that if a non-zero amount is entered on Line 9 (Car and Truck Expenses) and Form 4562 is not required, then all fields in Part IV must be completed, including the vehicle service date (month, day, year), business miles, commuting miles, other miles, and all Yes/No questions on lines 45 through 47b. The IRS requires this information to substantiate vehicle expense deductions. Incomplete vehicle information when car expenses are claimed may result in disallowance of the deduction.

12

Vehicle Service Date Format and Tax Year Validity Check

Validates that the vehicle service date entered in Part IV (Line 43) is in a valid date format with a real calendar month (01-12), day (01-31 appropriate to the month), and a four-digit year. Additionally, the service date must be on or before December 31, 2017, since this is a 2017 tax year form, and if the business was not started or acquired in 2017 (Line H unchecked), the vehicle service date should be consistent with prior-year use. An invalid or future date would indicate a data entry error that could invalidate the vehicle expense deduction.

13

Total Vehicle Miles Reasonableness and Consistency Check

Validates that the sum of business miles (Line 44a), commuting miles (Line 44b), and other miles (Line 44c) in Part IV represents a plausible total annual mileage, and that business miles are greater than zero when car and truck expenses are claimed on Line 9. The total mileage should not exceed a reasonable annual maximum (e.g., approximately 100,000 miles) and business miles must be a positive number to justify the deduction. If business miles are zero or the total mileage is implausibly high, the car and truck expense deduction may be flagged for review or disallowed.

14

Cost of Goods Sold Cross-Reference Consistency Check

Validates that the value entered on Line 4 (Cost of Goods Sold) matches the value calculated on Line 42 in Part III (Cost of Goods Sold = Line 40 minus Line 41), including both dollar and cents components. The form explicitly instructs that Line 42 should be entered on Line 4, making this a required cross-reference. A discrepancy between these two values indicates either a transcription error or an arithmetic mistake in Part III that would misstate the gross profit and all downstream income calculations.

15

Part III Cost of Goods Sold Arithmetic Validation

Validates that Line 40 in Part III equals the sum of Lines 35 through 39 (Inventory at Beginning of Year + Purchases Less Cost + Cost of Labor + Materials and Supplies + Other Costs), and that Line 42 equals Line 40 minus Line 41 (Inventory at End of Year). Both arithmetic relationships are explicitly defined on the form and must be internally consistent. Errors in these calculations will propagate to Line 4 and ultimately distort the gross profit, gross income, and net profit or loss figures reported on the form.

16

Total Other Expenses Line 48 and Line 27a Cross-Reference Check

Validates that the Total Other Expenses amount entered on Line 48 in Part V matches the value entered on Line 27a, and that Line 48 equals the sum of all individual other expense amounts listed in Part V. The form explicitly instructs that Line 48 should be entered on Line 27a, making this a required cross-reference that ensures all itemized other expenses are correctly totaled and carried forward. A mismatch between Line 48 and Line 27a, or between Line 48 and the sum of its component expenses, will result in an incorrect total expenses figure on Line 28.