Compliance Form 2106

Validation Checks by Instafill.ai

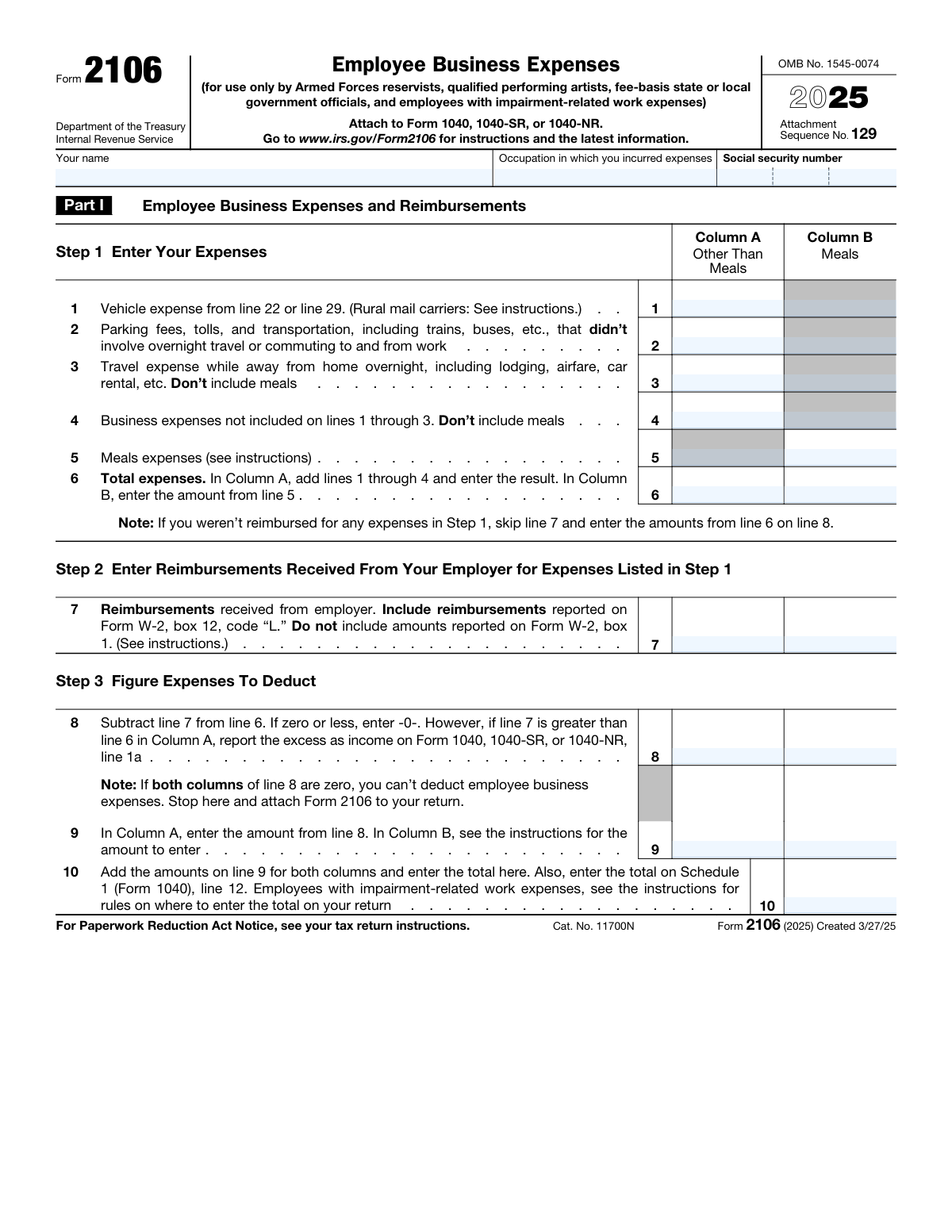

1

Ensures the Social Security Number is in a valid format

Validates that the three SSN fields together form a complete 9-digit Social Security Number in the standard XXX-XX-XXXX format, with the first group containing exactly 3 digits, the middle group exactly 2 digits, and the last group exactly 4 digits. The area number (first group) must not be 000, 666, or in the range 900–999, and the group and serial numbers must not be all zeros. An invalid or incomplete SSN will prevent the IRS from properly identifying the taxpayer and processing the return.

2

Ensures the Taxpayer Name is present and not left blank

Validates that the 'Your name' field is populated with a non-empty string representing the taxpayer's full legal name as it appears on their tax return. The name should include at least a first and last name and should not consist solely of whitespace or special characters. A missing or invalid name makes it impossible for the IRS to associate the form with the correct taxpayer account.

3

Ensures the Occupation field is completed and descriptive

Validates that the 'Occupation in which you incurred expenses' field is filled in with a meaningful job title or occupational description and is not left blank or filled with placeholder text. The occupation must correspond to one of the eligible categories for Form 2106 (Armed Forces reservist, qualified performing artist, fee-basis state or local government official, or employee with impairment-related work expenses). Leaving this field blank or entering a non-qualifying occupation could result in the deduction being disallowed upon IRS review.

4

Ensures Line 6 Column A equals the sum of Lines 1 through 4 in Column A

Validates that the value entered on Line 6, Column A (Total expenses, Other Than Meals) is mathematically equal to the sum of Lines 1, 2, 3, and 4 in Column A. This arithmetic check ensures the taxpayer has correctly totaled all non-meal business expenses before proceeding to the reimbursement and deduction steps. A discrepancy between the entered total and the computed sum indicates a data entry error that would cause downstream calculations on Lines 8, 9, and 10 to be incorrect.

5

Ensures Line 6 Column B equals the amount from Line 5 Column B

Validates that the value entered on Line 6, Column B (Total expenses, Meals) matches exactly the amount entered on Line 5, Column B, as required by the form instructions. Column B of Line 6 is not a sum of multiple lines but a direct carry-forward of the meals expense amount. Any deviation between these two fields indicates a transcription error that would distort the meals expense deduction calculation.

6

Ensures Line 8 correctly reflects the subtraction of Line 7 from Line 6 in both columns

Validates that Line 8 in each column equals Line 6 minus Line 7 for that column, and that if the result is zero or negative, the field contains zero (not a negative number). Additionally, if Line 7 Column A exceeds Line 6 Column A, the form should flag that the excess must be reported as income on Form 1040/1040-SR/1040-NR Line 1a. Failure to correctly compute Line 8 will result in an overstated or understated deduction and potential underreporting of income.

7

Ensures Line 10 equals the sum of Line 9 Column A and Line 9 Column B

Validates that the total entered on Line 10 is exactly equal to the sum of the amounts on Line 9, Column A and Line 9, Column B. Line 10 represents the total employee business expense deduction carried to Schedule 1 (Form 1040), Line 12, so any arithmetic error here directly affects the taxpayer's adjusted gross income. If both columns of Line 9 are zero, the form should indicate that no deduction is available and the taxpayer should stop and attach the form without entering a Line 10 amount.

8

Ensures Vehicle miles on Lines 12, 13, 16, and 17 are internally consistent

Validates that for each vehicle, the sum of business miles (Line 13) and commuting miles (Line 16) does not exceed total miles driven (Line 12), and that the other miles on Line 17 equal Line 12 minus the sum of Lines 13 and 16. All mileage fields must contain non-negative whole numbers, and Line 13 and Line 16 individually must each be less than or equal to Line 12. Inconsistent mileage figures would produce an incorrect business-use percentage on Line 14 and invalidate the vehicle expense deduction.

9

Ensures the Vehicle Business-Use Percentage on Line 14 is correctly calculated

Validates that the percentage entered on Line 14 for each vehicle equals Line 13 (business miles) divided by Line 12 (total miles), expressed as a percentage rounded appropriately, and falls between 0% and 100% inclusive. The business-use percentage is a critical multiplier used in Lines 27, 32, and 37 to determine the deductible portion of actual expenses and depreciation. An incorrect percentage will cascade errors through all subsequent actual-expense and depreciation calculations in Sections C and D.

10

Ensures the Vehicle Placed-in-Service Date is a valid calendar date not later than December 31, 2025

Validates that the month, day, and year fields for each vehicle's placed-in-service date (Line 11) together form a valid calendar date, with the month between 01 and 12, the day appropriate for the given month and year, and the year not later than 2025 (the tax year of the form). The placed-in-service date determines eligibility for depreciation and special allowances, so a date in a future year or an impossible date (e.g., February 30) would render the depreciation calculations invalid. If Vehicle 2 information is entered, its placed-in-service date must also be fully and validly completed.

11

Ensures Question 21 (Written Evidence) is answered only when Question 20 (Evidence) is answered Yes

Validates that Line 21 ('If Yes, is the evidence written?') is answered only when Line 20 ('Do you have evidence to support your deduction?') is answered Yes, and that Line 21 is left blank or unanswered when Line 20 is answered No. This conditional dependency reflects the form's own instructions and ensures logical consistency in the evidence attestation section. Answering Line 21 when Line 20 is No, or failing to answer Line 21 when Line 20 is Yes, creates an inconsistency that may trigger IRS scrutiny of the vehicle expense deduction.

12

Ensures Line 22 (Standard Mileage Rate) is correctly computed as Line 13 multiplied by $0.70

Validates that the amount entered on Line 22 equals the business miles on Line 13 multiplied by the 2025 standard mileage rate of $0.70 per mile, and that this amount is also carried forward to Line 1. The standard mileage rate is set by the IRS for the applicable tax year, and any deviation from the correct rate or arithmetic error will result in an incorrect vehicle expense deduction. This check also confirms that a taxpayer completing Section B has not simultaneously completed Section C for the same vehicle, as only one method may be used.

13

Ensures Line 24c equals Line 24a minus Line 24b for each vehicle

Validates that the value on Line 24c for each vehicle is exactly equal to Line 24a (vehicle rentals) minus Line 24b (inclusion amount), and that the result is not negative. The inclusion amount is required by the IRS to prevent taxpayers from claiming excessive deductions on luxury leased vehicles, and the subtraction must be performed correctly before the result is carried into the Line 26 total. A negative result or arithmetic error on Line 24c would overstate or understate the deductible rental expense.

14

Ensures Line 26 equals the sum of Lines 23, 24c, and 25 for each vehicle

Validates that Line 26 for each vehicle equals the arithmetic sum of Line 23 (gasoline, oil, repairs, insurance), Line 24c (net vehicle rentals), and Line 25 (employer-provided vehicle value) for that vehicle. This total represents the gross actual vehicle expenses before applying the business-use percentage, and an incorrect total will cause Line 27 and ultimately Line 29 to be wrong. All component lines must contain non-negative values, and any blank component line should be treated as zero in the summation.

15

Ensures Line 38 (Allowable Depreciation) is the smaller of Line 35 or Line 37, or equals Line 35 if Lines 36 and 37 are skipped

Validates that Line 38 for each vehicle contains the lesser of the amounts on Line 35 (total of Section 179/special allowance and computed depreciation) and Line 37 (applicable limit adjusted for business use), unless Lines 36 and 37 were intentionally skipped, in which case Line 38 must equal Line 35. This cap ensures compliance with IRS luxury automobile depreciation limits and prevents taxpayers from claiming depreciation in excess of the statutory ceiling. The Line 38 amount must also match the depreciation amount entered on Line 28 in Section C for the same vehicle.

16

Ensures that Section B (Standard Mileage) and Section C (Actual Expenses) are not both completed for the same vehicle

Validates that for each vehicle, the taxpayer has completed either Section B (Standard Mileage Rate) or Section C (Actual Expenses), but not both, as the IRS requires the use of only one method per vehicle per tax year. If Line 22 contains a value for a vehicle, Lines 23 through 29 for that same vehicle should be blank, and vice versa. Completing both sections for the same vehicle would result in a double-counted or ambiguous vehicle expense on Line 1 and could trigger an IRS examination.