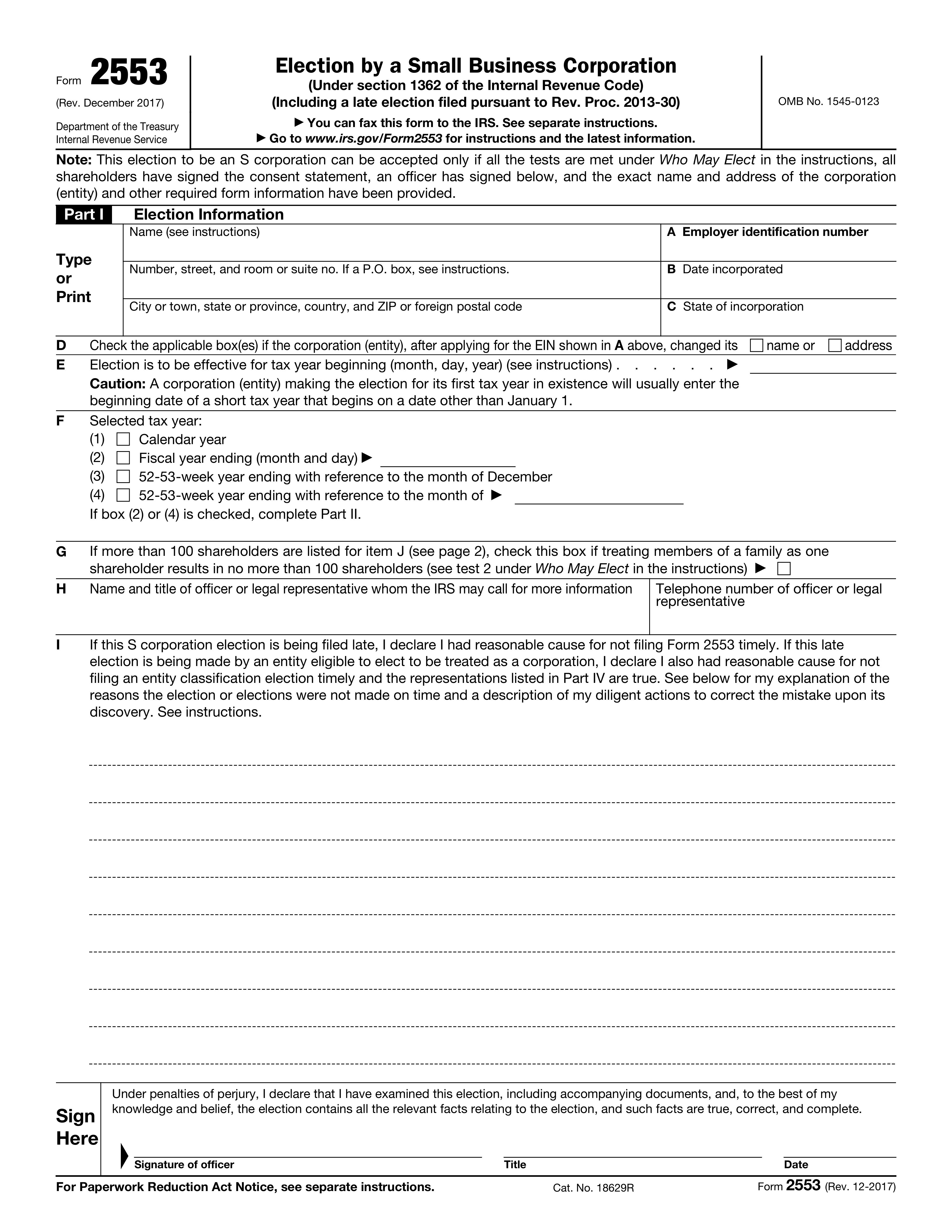

An incorrect or missing Employer Identification Number (EIN) is a frequent error when filling out Form 2553. The EIN is crucial for the IRS to identify the business entity making the election. To avoid this mistake, ensure that the EIN provided matches exactly with the one issued by the IRS. Double-check the EIN on any correspondence received from the IRS or on the EIN confirmation letter. If you're unsure about your EIN, contact the IRS directly for verification before submitting the form.

Failing to meet all the 'Who May Elect' tests is a common oversight that can invalidate the S corporation election. These tests include requirements related to the number of shareholders, types of shareholders, and the type of stock issued. To prevent this mistake, thoroughly review the eligibility criteria outlined in the IRS instructions for Form 2553. Ensure your corporation meets all the specified conditions before proceeding with the election. Consulting with a tax professional can also help verify your corporation's eligibility.

Missing or incorrect shareholder consents can lead to the rejection of the S corporation election. Each shareholder must consent to the election, and their consent must be accurately documented. To avoid this issue, ensure that all shareholders have provided their consent in writing and that these consents are correctly attached to the Form 2553. It's advisable to use the consent statement provided in the IRS instructions or consult with a tax advisor to ensure all consents are properly executed and documented.

Providing an incorrect or missing corporation name and address is a mistake that can cause delays or rejection of the S corporation election. The name and address must match exactly with the information on file with the IRS. To avoid this error, verify the corporation's name and address using the EIN confirmation letter or any recent correspondence from the IRS. If there have been any changes, ensure that the IRS has been notified prior to submitting Form 2553.

Failing to indicate a name or address change after the EIN application is a common mistake that can lead to processing issues. If the corporation's name or address has changed since the EIN was issued, this information must be updated with the IRS before submitting Form 2553. To prevent this oversight, review the corporation's current information with the IRS and file the necessary forms to update any changes. Ensuring the IRS has the most current information will facilitate a smoother election process.

A frequent error is not specifying the correct effective date of the election or omitting it entirely. The effective date is crucial as it determines when the S corporation election begins. To avoid this mistake, carefully review the instructions provided by the IRS for Form 2553, ensuring the date aligns with the intended start of the S corporation status. It's advisable to consult with a tax professional to confirm the appropriate effective date based on your specific circumstances.

Another common oversight is failing to accurately specify the type of tax year the corporation intends to adopt. This can lead to complications with the IRS and potential delays in processing the election. To prevent this, thoroughly understand the different tax year options available and select the one that best fits your business operations. Consulting with a tax advisor can provide clarity and ensure the correct tax year type is chosen.

Mistakenly treating family members as a single shareholder is a common error that can affect the eligibility and benefits of the S corporation election. Each family member must be considered an individual shareholder with their own shares and voting rights. To avoid this mistake, ensure that each family member's ownership is accurately represented and documented. Seeking guidance from a legal or tax professional can help navigate the complexities of shareholder classification.

Omitting or providing incorrect contact information for the officer or representative can lead to communication issues with the IRS. This includes errors in phone numbers, addresses, or email addresses. To prevent this, double-check all contact information for accuracy before submitting Form 2553. It's also beneficial to include multiple forms of contact to ensure the IRS can reach the appropriate person if needed.

Not declaring a reasonable cause for a late S corporation election is a mistake that can result in the rejection of the election. The IRS requires a detailed explanation and evidence of reasonable cause for elections filed after the deadline. To avoid this, prepare a comprehensive statement explaining the circumstances that led to the late filing, supported by relevant documentation. Consulting with a tax professional can help articulate a compelling case for reasonable cause.

A frequent oversight when completing Form 2553 is the omission of necessary signatures or the incorrect dating of the form. This can lead to the rejection of the election by the IRS. To avoid this, ensure that all required parties sign the form and that the date reflects when the form was actually signed. Double-check the instructions for specific signature requirements, as they can vary depending on the entity type. It's also advisable to review the form for any additional signature lines that may be overlooked.

Part II of Form 2553 is crucial for selecting the fiscal tax year, yet it is often left incomplete or filled out incorrectly. This section must accurately reflect the corporation's desired fiscal year-end. To prevent errors, carefully review the IRS guidelines on fiscal year selection and consult with a tax professional if necessary. Ensure that the chosen fiscal year aligns with the corporation's accounting practices and business needs. Incorrectly completing this part can result in unintended tax consequences and delays in processing the election.

Part III of Form 2553 pertains to the Qualified Subchapter S Trust (QSST) election, which is often either incorrectly completed or entirely omitted. This section is vital for trusts that are shareholders in the S corporation. To avoid mistakes, thoroughly understand the requirements for a QSST election and ensure that all necessary information is accurately provided. Consulting with a tax advisor or legal professional can help clarify any uncertainties and ensure compliance with IRS regulations. An incorrect or missing QSST election can jeopardize the S corporation status and lead to adverse tax implications.

Part IV of Form 2553 is designated for late corporate classification elections, but it is frequently filled out incompletely or inaccurately. This section requires detailed information about the corporation's history and the reasons for the late election. To ensure accuracy, provide a comprehensive explanation and all requested details regarding the late election. It's beneficial to seek guidance from a tax professional to navigate the complexities of late classification elections. Errors in this part can result in the denial of the late election request, affecting the corporation's tax status.

A common mistake is the failure to attach all required documents and statements to Form 2553. This oversight can lead to the rejection of the S corporation election. To prevent this, carefully review the form instructions to identify all necessary attachments, such as shareholder consents and corporate resolutions. Ensure that each document is complete, accurate, and properly formatted according to IRS guidelines. Organizing and reviewing all attachments before submission can help avoid delays and ensure the successful processing of the election.