Fill out employer plan forms

with AI.

Employer plan forms are essential documents for managing retirement assets within corporate or institutional frameworks. This category of paperwork facilitates the movement of money between different accounts, such as 403(b), 401(k), or 457(b) plans, ensuring that retirement savings are consolidated and managed efficiently. These forms serve as the legal bridge between financial institutions, allowing for the secure transfer of wealth while maintaining the necessary tax-advantaged status of your investments.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About employer plan forms

Typically, these forms are required by employees or former employees who are looking to streamline their retirement strategy or access their funds. Common situations include rolling over assets from a previous employer to a new plan or initiating a cash withdrawal through a Transfer Payout Annuity. For example, documents like the Easy Transfer Form (F10462) are vital when individuals need to consolidate assets at TIAA, while Form F10794 is used for managing specific annuity payouts in private employer plans. Navigating these administrative requirements is a key step in long-term financial planning and ensuring that retirement funds are accessible and organized.

Completing these detailed financial documents can be time-consuming and requires high precision to avoid processing delays. Tools like Instafill.ai use AI to fill these forms in under 30 seconds, handling sensitive data accurately and securely to streamline the entire submission process. This practical approach eliminates the manual effort of typing into complex PDFs, allowing you to focus on your financial goals rather than tedious paperwork.

Forms in This Category

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Navigating retirement plan paperwork can be complex, especially when dealing with employer-sponsored plans. To choose the correct form, you first need to determine the direction of your funds: are you consolidating assets into your TIAA account or requesting a payout?

Consolidating Assets into a TIAA Plan

If you have retirement savings sitting in a former employer's 401(k), 403(b), or 457(b) and want to move them into your current TIAA employer-sponsored plan, you should use the Form F10462 series. This process is often referred to as a "direct transfer" or "rollover."

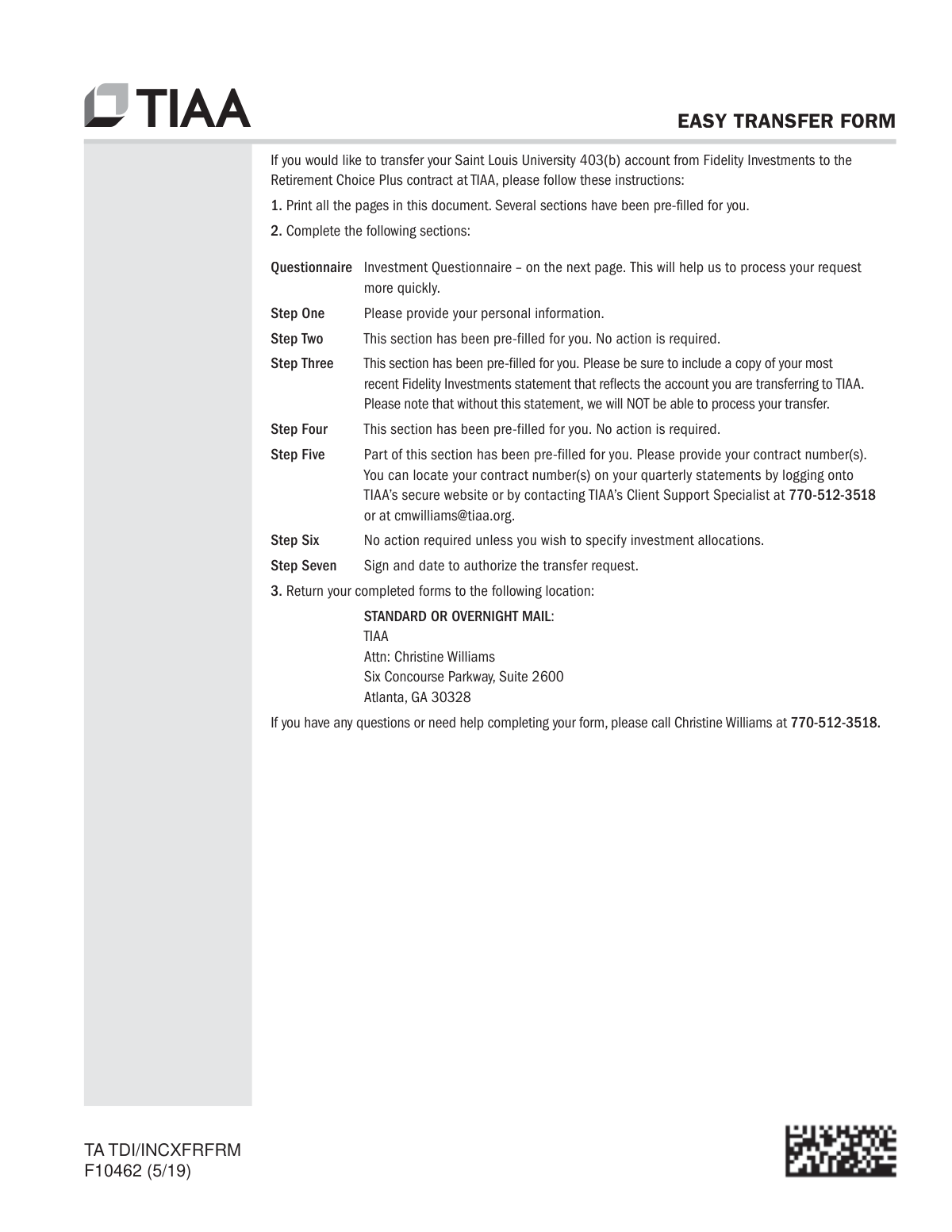

- Easy Transfer Form: Moving Funds to an Employer-Sponsored Retirement Plan at TIAA (Form F10462): Use this if you want a streamlined way to authorize TIAA to request funds from your current financial institution. This is the best choice for consolidating multiple accounts into one place.

- Moving Funds to an Employer-Sponsored Retirement Plan at TIAA: This is the standard version of the document used to authorize TIAA to initiate the transfer process on your behalf. It is essential for managing all your retirement assets under a single employer-sponsored umbrella.

Withdrawing or Rolling Over Private Employer Plan Funds

If you are a participant in a private employer plan and need to access your money or move it elsewhere, the requirements are different, particularly regarding TIAA Traditional accounts which may have specific liquidity rules.

- Form F10794, Cash Withdrawal or Rollover Transfer Payout Annuity for Private Employer Plans: Choose this form if you need to initiate a cash withdrawal or a rollover from a TIAA Traditional account within a private plan.

- Understanding the TPA: Be aware that this form is used to establish a Transfer Payout Annuity (TPA). This means your funds will be disbursed in 10 payments over a 9-year period rather than a single lump sum, adhering to TIAA's long-term investment structure.

By identifying whether you are performing an "inbound" transfer to consolidate your savings (Form F10462) or an "outbound" withdrawal from a private plan (Form F10794), you can ensure your request is processed accurately.

Form Comparison

| Form | Primary Purpose | Fund Direction | Payout Method |

|---|---|---|---|

| Easy Transfer Form: Moving Funds to an Employer-Sponsored Retirement Plan at TIAA | Consolidate retirement savings into a TIAA employer-sponsored plan. | Inbound transfer from an outside financial institution to TIAA. | Direct transfer or rollover of specified retirement account funds. |

| Form F10462, Moving Funds to an Employer-Sponsored Retirement Plan at TIAA | Authorize consolidation of retirement assets into a TIAA account. | Inbound transfer from an outside financial institution to TIAA. | Direct transfer or rollover of specified retirement account funds. |

| Moving Funds to an Employer-Sponsored Retirement Plan at TIAA | Initiate a rollover or transfer from another institution into TIAA. | Inbound transfer from an outside financial institution to TIAA. | Direct transfer or rollover of specified retirement account funds. |

| Form F10794, Cash Withdrawal or Rollover Transfer Payout Annuity for Private Employer Plans | Withdraw or roll over funds from TIAA Traditional accounts. | Outbound movement from a TIAA private employer retirement plan. | Ten payments disbursed over a nine-year period via annuity. |

Tips for employer plan forms

Ensure the name and details on your existing retirement account match your TIAA account exactly to avoid processing delays. Even minor discrepancies in middle initials or suffixes can cause the receiving institution to reject the transfer request, requiring you to restart the paperwork.

If you are using Form F10794, be aware that funds are disbursed in 10 installments over a nine-year period. This is a long-term liquidity commitment, so verify that this specific payout structure fits your retirement strategy before finalizing the withdrawal.

Before initiating a move with Form F10462, check with your current employer's plan administrator to ensure your specific plan accepts incoming rollovers. Not all employer-sponsored plans allow for the consolidation of outside assets like IRAs or previous 401(k) funds.

AI-powered tools like Instafill.ai can complete these employer plan forms in under 30 seconds with high accuracy. Your financial data stays secure during the process, providing a massive time-saving benefit for those managing multiple retirement accounts simultaneously.

Keep your latest account statement from the 'sending' institution nearby while filling out these forms. You will need the exact account number and the full legal name of the institution to ensure the funds are routed correctly without manual intervention.

When selecting a withdrawal or rollover option, verify the tax implications of your choice. Selecting a direct rollover usually avoids immediate tax withholding, whereas a cash withdrawal may trigger mandatory federal and state tax deductions that reduce your final payout.

Frequently Asked Questions

Employer plan forms are documents used to manage retirement assets within company-sponsored accounts, such as 401(k) or 403(b) plans. They typically facilitate the movement of funds between financial institutions, withdrawals, or the consolidation of various retirement savings into a single managed plan.

Consolidating accounts into a single plan can simplify your financial management by reducing the number of statements you receive and making it easier to track your investment performance. It may also allow you to take advantage of specific investment options or lower administrative fees offered through your current employer's plan.

A direct transfer involves moving funds directly from one financial institution to another without the account holder receiving the money, which typically avoids tax implications. A rollover involves moving funds from a retirement plan to the participant, who then has a limited window to deposit those funds into another qualified plan to maintain tax-deferred status.

These forms are generally intended for employees or former employees who have retirement accounts through TIAA or are looking to move assets into a TIAA-managed employer plan. This includes participants in private employer plans, 403(b) plans for non-profits, and other institutional retirement programs.

A Transfer Payout Annuity is a specific method used by TIAA to disburse funds from certain accounts, such as TIAA Traditional, over a set period. For private employer plans, this often involves receiving the total value in ten installments over nine years, ensuring a steady payout while adhering to the plan's liquidity rules.

You will generally need your personal identification details, your current TIAA account number, and the details of the external financial institution from which you are moving funds. If you are initiating a rollover, you may also need information regarding the specific plan type and the mailing address for the receiving institution.

Yes, AI tools like Instafill.ai can fill these forms in under 30 seconds by accurately extracting and placing data from your source documents. This automation helps ensure that complex account numbers and transfer details are entered correctly, reducing the likelihood of processing errors.

Using AI-powered services, you can complete these forms in under 30 seconds. By automating the data entry process, you can move from a blank document to a finalized form ready for submission much faster than manual typing would allow.

Completed forms are typically submitted directly to the financial institution managing the plan, such as TIAA, or to your employer's human resources department. Submission methods often include secure online uploads, fax, or traditional mail, depending on the specific requirements of the plan administrator.

Generally, if you perform a direct transfer or a timely rollover into another qualified retirement plan, the transaction is not considered a taxable event. However, failing to follow specific IRS guidelines or taking a cash withdrawal instead of a rollover may result in income taxes and potential early withdrawal penalties.

You should file these forms when you change jobs, when you want to consolidate multiple retirement accounts, or when you are preparing for retirement and need to establish a payout schedule. It is advisable to start the process early, as fund transfers between institutions can sometimes take several weeks to finalize.

Glossary

- Rollover

- The process of moving funds from one tax-advantaged retirement account to another, typically to maintain the tax-deferred status of the savings.

- Direct Transfer

- A transaction where retirement funds are moved directly between financial institutions without the participant receiving the money, avoiding mandatory tax withholding.

- Employer-Sponsored Plan

- A retirement savings program, such as a 401(k) or 403(b), provided by an employer for the benefit of its employees.

- 403(b) Plan

- A retirement plan specifically designed for employees of public schools, certain non-profits, and religious organizations.

- Transfer Payout Annuity (TPA)

- A TIAA-specific distribution method that pays out funds from a fixed annuity in multiple installments over a set period, such as nine years.

- 457(b) Plan

- A tax-advantaged retirement plan typically offered to state and local government employees and some non-profit executives.

- TIAA Traditional

- A fixed annuity product that offers guaranteed growth and principal protection, often requiring specific payout methods like a TPA for withdrawals.

- Consolidation

- The act of combining multiple retirement accounts from various previous employers into a single plan to simplify management and tracking.