Fill out 529 plan forms

with AI.

529 plan forms cover a wide range of administrative and financial transactions related to tax-advantaged education savings accounts. Whether you're opening a new account, requesting a withdrawal for qualified education expenses, rolling over funds from one plan to another, or updating a beneficiary after a life change, there's a specific form required to make it happen correctly. These forms are issued by major financial institutions — including Fidelity, Vanguard, Merrill Lynch, and state-sponsored plans like Ohio's CollegeAdvantage — and must be completed accurately to stay compliant with IRS rules around contribution limits, rollover windows, and tax treatment.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About 529 plan forms

People who typically need these forms include parents and grandparents saving for a child's college education, account owners managing beneficiary changes after a divorce or the birth of a new child, and individuals looking to consolidate multiple 529 accounts or roll funds into a Roth IRA under newer SECURE 2.0 provisions. Trustees, legal representatives, and financial advisors also frequently work with these forms when managing accounts on behalf of others.

Because many of these forms involve precise financial and legal details — account numbers, Social Security numbers, earnings breakdowns, and signatures — accuracy matters. Tools like Instafill.ai use AI to fill these forms in under 30 seconds, reducing the risk of errors that could trigger unexpected tax consequences or processing delays.

Forms in This Category

The forms in this category have a median Form Complexity Index of 41/100 (Basic), measured across 23 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Not all 529 forms serve the same purpose — and using the wrong one can cause delays or tax complications. Here's how to quickly find the right form for your situation.

Opening a New 529 Account

If you're just getting started, you need an account application:

- 529 Plan Account Application — a general-purpose application for establishing a new 529 plan

- Fidelity Institutional CHET Advisor 529 Plan New Account Application — specifically for opening a Connecticut CHET Advisor account through Fidelity

Moving Money In (Rollovers & Transfers)

Consolidating education savings from another plan or account? Use one of these:

- Rollover Request — 529 College Savings Plan — for rolling funds into a Fidelity-managed 529 from another 529, Coverdell ESA, or U.S. Savings Bond

- Vanguard 529 Incoming Direct Rollover Form (529IRF) — to bring funds into a Vanguard 529 from another 529 or ESA

- 529 Plan Account Transfer Form — to transfer all assets from an existing 529 to a Pershing LLC brokerage account

Taking Money Out (Withdrawals)

Need to access your funds? Match the form to your plan provider:

- Fidelity Investments Withdrawals — 529 College Savings Plan — for one-time distributions from a Fidelity 529

- Vanguard 529 Withdrawal Request Form (529DRF) — for qualified or nonqualified withdrawals from a Vanguard 529

- Merrill Lynch 529 College Savings Plan Withdrawal Request Form — for Merrill Lynch account holders

- Vanguard 529 Direct Rollover Out to Roth IRA (529ROR) — specifically for rolling 529 funds into a beneficiary's Roth IRA

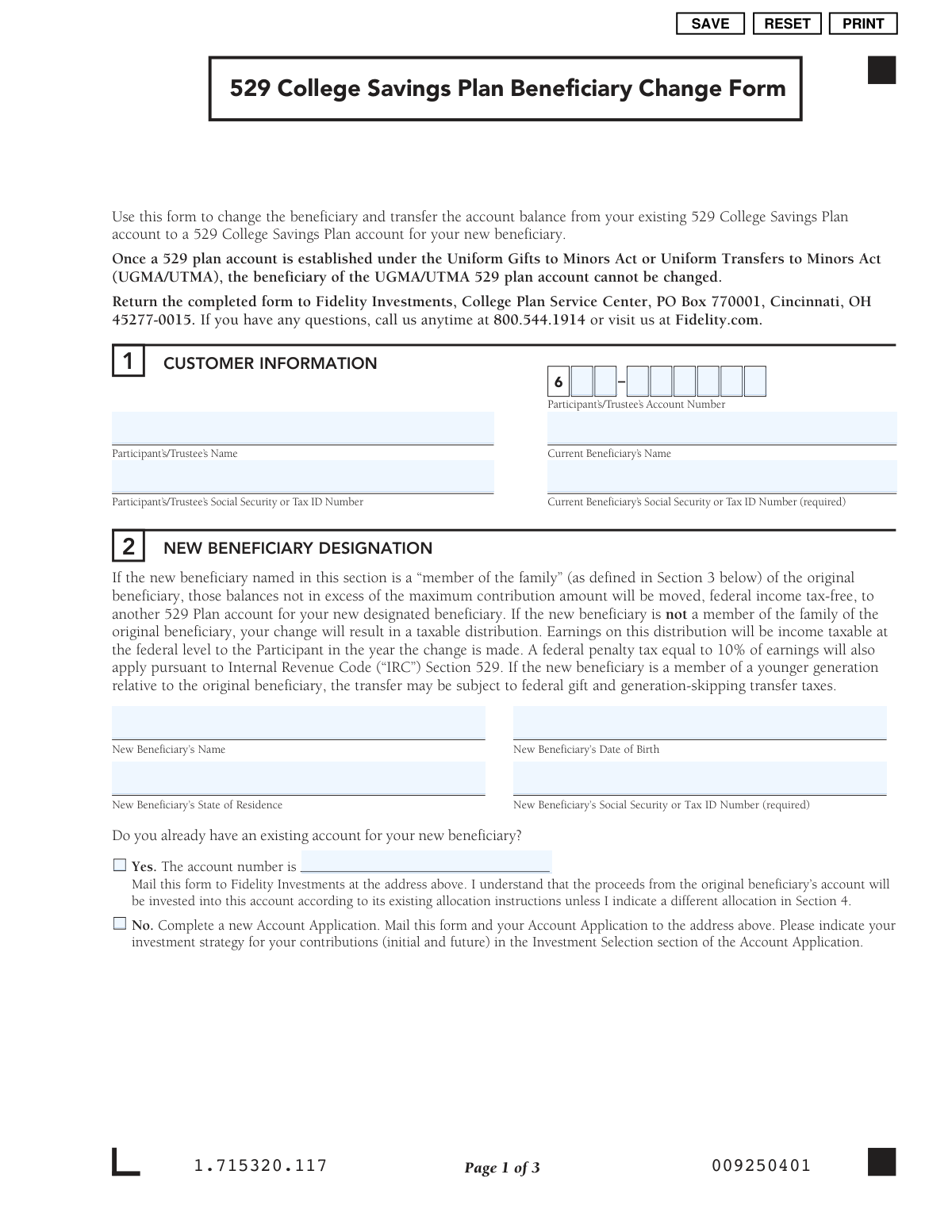

Changing the Beneficiary

- Fidelity Institutional 529 College Savings Plan Beneficiary Change — for Fidelity account holders

- 529 College Savings Plan Beneficiary Change Form — a general beneficiary change and balance transfer form

- CollegeAdvantage Direct 529 Savings Plan Beneficiary Change Form — for Ohio CollegeAdvantage account owners

Account Authority & Legal Documents

For managing who controls the account:

- Vanguard 529 Power of Attorney (529POA) — grants broad authority to an agent

- Vanguard 529 Agent Authorization/Limited Power of Attorney (529LPOA) — grants restricted, specific powers

- Vanguard 529 Trustee Certification (529TCF) — required when a trust holds the account

- IAdvisor 529 Plan Certification of Authorized Individual(s) — for entities like corporations or partnerships managing an IAdvisor account

- Vanguard 529 Transfer Due to Death of Account Owner — for transferring account ownership after the owner's passing

Form Comparison

| Form | Purpose | Who Files It | When to Use |

|---|---|---|---|

| Rollover Request — 529 College Savings Plan | Roll over funds into a Fidelity 529 plan | Existing 529 or ESA account owner | Consolidating education savings from another plan |

| Fidelity Investments Withdrawals—529 College Savings Plan | Request a one-time distribution from Fidelity 529 | Fidelity 529 plan account owner | Paying education expenses or rolling over funds |

| The Vanguard 529 College Savings Plan: Power of Attorney | Grant broad account management authority to an agent | Vanguard 529 account owner | Appointing someone to fully manage the account |

| The Vanguard 529 College Savings Plan Agent Authorization/Limited Power of Attorney | Grant limited, specific account powers to an agent | Vanguard 529 account owner | Delegating restricted account actions to an agent |

| The Vanguard 529 College Savings Plan Direct Rollover Out to Roth IRA Form | Transfer 529 funds directly to beneficiary's Roth IRA | Vanguard 529 account owner | Moving unused 529 funds to a Roth IRA |

| The Vanguard 529 College Savings Plan Transfer Due to Death of Account Owner Form | Transfer account ownership after owner's death | Successor owner or estate representative | When original Vanguard 529 account owner has died |

| The Vanguard 529 College Savings Plan Incoming Direct Rollover Form | Roll over funds into a Vanguard 529 plan | Vanguard 529 account owner | Consolidating education savings into Vanguard plan |

| The Vanguard 529 College Savings Plan: Withdrawal Request Form | Withdraw funds from a Vanguard 529 account | Vanguard 529 account owner | Paying qualified or nonqualified education expenses |

| IAdvisor 529 Plan Certification of Authorized Individual(s) | Certify authorized individuals for entity-owned account | Corporate or organizational account owner | Setting up entity account management authority |

| Merrill Lynch 529 College Savings Plan Withdrawal Request Form | Request withdrawal from Merrill Lynch 529 account | Merrill Lynch 529 plan participant | Paying education expenses or rolling over to Roth IRA |

| 529 Plan Account Transfer Form | Transfer all 529 assets to a Pershing LLC account | Existing 529 plan account holder | Switching 529 plan management to a new firm |

| Fidelity Institutional CHET Advisor 529 Plan New Account Application | Open a new CHET Advisor 529 account via Fidelity | New CHET Advisor 529 plan participant | Starting a Connecticut tax-advantaged education savings account |

| Form 529TCF, The Vanguard 529 College Savings Plan, Trustee Certification | Certify trustee identity and authority for trust account | Trustee of a Vanguard 529 trust account | Opening or updating a trust-owned Vanguard 529 account |

| 529 Plan Account Application | Open a new 529 college savings plan account | New 529 plan account owner | Establishing a new education savings account |

| Fidelity Institutional 529 College Savings Plan Beneficiary Change | Change designated beneficiary on Fidelity 529 account | Fidelity Institutional 529 account owner | Updating beneficiary due to family circumstances |

| 529 College Savings Plan Beneficiary Change Form | Change beneficiary and transfer 529 account balance | 529 plan account holder | Redirecting savings to a different family member |

| CollegeAdvantage Direct 529 Savings Plan Beneficiary Change Form | Change beneficiary on Ohio CollegeAdvantage 529 account | Ohio CollegeAdvantage Direct 529 account owner | Transferring full or partial balance to new beneficiary |

Tips for 529 plan forms

When rolling over funds between 529 plans, the IRS requires the transfer to be completed within 60 days of withdrawal to avoid taxes and penalties. Additionally, you're generally limited to one rollover per beneficiary per 12-month period. Missing either rule can result in the entire amount being treated as a taxable distribution.

Many rollover and withdrawal forms require you to break down the amount being transferred into its principal (contributions) and earnings components. Failing to provide this breakdown can cause the IRS to treat the entire amount as earnings, creating unexpected tax liability. Check your account statements before filling out any rollover or withdrawal form.

Changing a 529 beneficiary can have tax implications depending on how closely related the new beneficiary is to the current one. A change to a non-family member may trigger taxes and a 10% penalty on earnings. Always confirm the IRS definition of an eligible family member before submitting a beneficiary change form.

If you're managing several 529 accounts or handling a rollover, withdrawal, and beneficiary change at the same time, AI-powered tools like Instafill.ai can complete these forms in under 30 seconds with high accuracy. Your data stays secure throughout the process, making it a practical time-saver when dealing with a stack of related forms. It can also convert non-fillable PDFs into interactive forms, which is especially useful for older plan documents.

Many 529 forms — especially transfers due to death, trustee certifications, and power of attorney documents — require supporting paperwork such as death certificates, trust agreements, or notarized signatures. Identifying these requirements upfront prevents delays caused by incomplete submissions. Review the full instructions for each form before you start filling it out.

Withdrawals used for qualified education expenses (tuition, fees, books, room and board) are tax-free, while non-qualified withdrawals are subject to income tax and a 10% penalty on earnings. When completing a withdrawal request form, clearly indicate the purpose of the distribution to ensure it's processed correctly. Keep receipts for qualified expenses in case of an IRS audit.

Errors in bank account or routing numbers on withdrawal and rollover forms are one of the most common causes of delayed or misdirected funds. Always verify these details against a voided check or your bank's official documentation rather than relying on memory. A single transposed digit can send funds to the wrong account and require a lengthy correction process.

There's a significant difference between a full Power of Attorney and a Limited Power of Attorney for 529 accounts — one grants broad control while the other restricts the agent to specific actions. Read each form's scope carefully and choose the level of authority that matches your actual needs. Granting more access than intended can put your account at risk.

Frequently Asked Questions

This category includes 17 forms covering a wide range of 529 plan needs, including account applications, withdrawal requests, rollover requests, beneficiary changes, power of attorney designations, trustee certifications, and account transfers. Forms are available from major providers such as Fidelity, Vanguard, Merrill Lynch, and state-specific plans like Ohio's CollegeAdvantage.

The right form depends on what action you want to take with your 529 account. For example, use an account application form to open a new plan, a withdrawal request form to take distributions, a rollover form to move funds between plans, or a beneficiary change form to update who the savings are designated for. Each form listing in this category includes a description to help you identify the correct one.

529 plan forms are generally completed by account owners (participants), their authorized agents, trustees, or legal representatives. In some cases, such as the Transfer Due to Death of Account Owner form, the successor or estate representative would be the one completing the paperwork.

No — most forms in this category are provider-specific, meaning a Fidelity withdrawal form is designed for Fidelity-managed 529 accounts, and a Vanguard rollover form is intended for Vanguard 529 plans. Always make sure you are using the form that matches your specific 529 plan provider to ensure your request is processed correctly.

Yes, several IRS regulations apply to 529 plan transactions. For example, rollovers must generally be completed within 60 days and are subject to a once-per-12-months rule, and withdrawals for non-qualified expenses may be subject to taxes and penalties. It is advisable to consult a tax professional or your plan provider to ensure compliance before submitting any form.

Completed forms are typically submitted directly to your 529 plan provider — either by mail, fax, or through the provider's online portal. Each provider (Fidelity, Vanguard, Merrill Lynch, etc.) has its own submission process, so refer to the instructions included with the specific form or contact your plan administrator for guidance.

Errors on 529 plan forms can cause processing delays or, in some cases, unintended tax consequences — for example, an incorrectly completed rollover form could result in the entire amount being treated as earnings. It is important to review all information carefully before submitting, and many providers will require a corrected form if errors are identified.

Yes — AI-powered tools like Instafill.ai can fill out 529 plan forms in under 30 seconds by accurately extracting and placing data from your source documents. This reduces the risk of manual entry errors and speeds up the process significantly, whether you are completing a rollover request, withdrawal form, or account application.

Filling out 529 plan forms manually can take anywhere from a few minutes to longer depending on the complexity of the form. Using AI-powered services like Instafill.ai, these forms can typically be completed in under 30 seconds, as the AI automatically extracts and populates the required fields from your existing documents.

A rollover involves the account owner receiving the funds and then depositing them into another 529 plan within 60 days, while a direct rollover or transfer moves funds directly between plans without the owner taking possession. Direct rollovers are generally simpler and carry less risk of triggering taxes or penalties, and separate forms exist in this category for each type of transaction.

Yes, 529 plan account owners can typically change the designated beneficiary, and this category includes several beneficiary change forms from providers like Fidelity, Vanguard, and the Ohio CollegeAdvantage plan. Tax implications may vary depending on the relationship between the current and new beneficiary, so it is worth reviewing IRS guidelines or consulting a tax advisor before making the change.

Some forms require supporting documentation — for example, the Transfer Due to Death of Account Owner form may require a death certificate or estate authorization documents, and trustee certification forms require evidence of the trust's legal standing. Always review the specific form's requirements and gather any necessary documents before submitting.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 41/100 (Basic). See exactly how it is calculated.

- 529 Plan

- A tax-advantaged savings account sponsored by a state or institution, designed to encourage saving for future education costs. Earnings grow tax-free, and withdrawals for qualified education expenses are not subject to federal income tax.

- Beneficiary

- The individual (typically a student) designated to use the 529 plan funds for qualified education expenses. The account owner can usually change the beneficiary to another eligible family member without tax penalties.

- Qualified Education Expenses

- IRS-approved costs that can be paid with 529 plan funds without triggering taxes or penalties, including tuition, fees, books, room and board, K-12 tuition (up to $10,000/year), and registered apprenticeship programs.

- Nonqualified Withdrawal

- A distribution from a 529 plan used for expenses that do not meet IRS guidelines. The earnings portion of a nonqualified withdrawal is subject to ordinary income tax plus a 10% federal penalty.

- Direct Rollover

- A tax-free transfer of funds moved directly from one 529 plan (or eligible account) to another, without the money passing through the account owner's hands. This avoids the 60-day rollover window and reduces the risk of tax penalties.

- 60-Day Rollover Rule

- An IRS rule requiring that funds withdrawn from a 529 plan and intended for rollover to another 529 plan must be deposited into the new account within 60 days to avoid taxes and penalties.

- Once-Per-12-Months Rollover Rule

- An IRS restriction limiting indirect (non-direct) rollovers for the same beneficiary to once every 12 months. Exceeding this limit can result in the rolled-over amount being treated as a taxable distribution.

- Coverdell Education Savings Account (ESA)

- A tax-advantaged savings account (formerly called an Education IRA) that can be rolled over into a 529 plan. Like a 529, it allows tax-free growth and withdrawals for qualified education expenses but has lower annual contribution limits.

- ABLE Account

- A tax-advantaged savings account for individuals with disabilities (Achieving a Better Life Experience). Certain 529 plan funds can be rolled over into an ABLE account for the beneficiary without incurring taxes or penalties.

- Successor Account Owner

- The individual designated to take control of a 529 plan account if the original account owner dies or becomes incapacitated. This person assumes all rights and responsibilities of managing the account on behalf of the beneficiary.