Yes! You can use AI to fill out Arizona Form 285-I, Individual Income Tax Disclosure/Representation Authorization Form

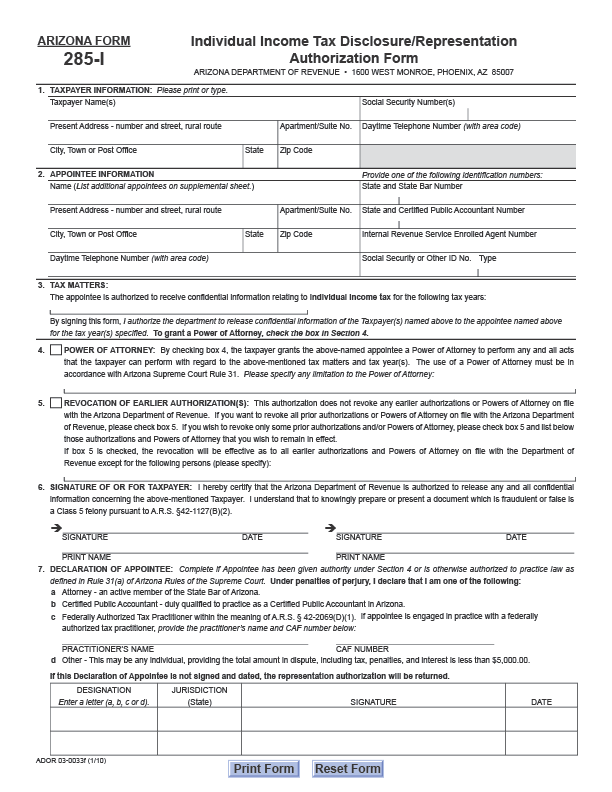

Arizona Form 285-I is an authorization form used by individual taxpayers to name an appointee (such as an attorney, CPA, enrolled agent, or other eligible representative) who may receive confidential Arizona individual income tax information. The taxpayer can also optionally grant the appointee Power of Attorney to act on the taxpayer’s behalf for specified tax matters and tax years, subject to Arizona Supreme Court Rule 31. The form can be used to keep prior authorizations in place or to revoke earlier authorizations and powers of attorney on file with the Arizona Department of Revenue. It is important because ADOR generally cannot discuss or release taxpayer information to third parties without a valid authorization on file.

Arizona Form 285-I is part of the

disclosure forms, tax forms, individual tax forms, authorization forms, income forms and income tax forms categories on Instafill.

Form specifications

| Form name: | Arizona Form 285-I, Individual Income Tax Disclosure/Representation Authorization Form |

| Number of pages: | 1 |

| Language: | English |

Our AI automatically handles information lookup, data retrieval, formatting, and form filling.

It takes less than a minute to fill out Arizona Form 285-I using our AI form filling.

Securely upload your data. Information is encrypted in transit and deleted immediately after the form is filled out.

Instafill Demo: How to fill out PDF forms in seconds with AI

How to Fill Out Arizona Form 285-I Online for Free in 2026

Are you looking to fill out a ARIZONA FORM 285-I form online quickly and accurately? Instafill.ai offers the #1 AI-powered PDF filling software of 2026, allowing you to complete your ARIZONA FORM 285-I form in just 37 seconds or less.

Follow these steps to fill out your ARIZONA FORM 285-I form online using Instafill.ai:

- 1 Enter taxpayer information: taxpayer name(s), Social Security number(s), current address, city/state/ZIP, and daytime phone number.

- 2 Enter appointee information: appointee name, address, phone number, and one qualifying identification number (e.g., AZ State Bar number, AZ CPA number, IRS enrolled agent number, or SSN/other ID with type).

- 3 Specify the tax matters and tax year(s) for which the appointee is authorized to receive confidential individual income tax information.

- 4 If you want the appointee to act for you (not just receive information), check the Power of Attorney box in Section 4 and list any limitations to the authority granted.

- 5 Decide whether to revoke earlier authorizations/powers of attorney: check the revocation box if desired and list any prior authorizations that should remain in effect.

- 6 Sign and date the taxpayer signature section (and print names) for all required taxpayers/authorized signers.

- 7 If Power of Attorney is granted or the appointee will represent the taxpayer under Rule 31, have the appointee complete the Declaration of Appointee (designation, jurisdiction, signature, and date; include practitioner name/CAF number if applicable).

Our AI-powered system ensures each field is filled out correctly, reducing errors and saving you time.

Why Choose Instafill.ai for Your Fillable Arizona Form 285-I Form?

Speed

Complete your Arizona Form 285-I in as little as 37 seconds.

Up-to-Date

Always use the latest 2026 Arizona Form 285-I form version.

Cost-effective

No need to hire expensive lawyers.

Accuracy

Our AI performs 10 compliance checks to ensure your form is error-free.

Security

Your personal information is protected with bank-level encryption.

Frequently Asked Questions About Arizona Form 285-I

Form 285-I authorizes the Arizona Department of Revenue (ADOR) to disclose a taxpayer’s confidential individual income tax information to an appointee. If you also check Section 4, it can grant the appointee Power of Attorney to act on the taxpayer’s behalf for the tax matters and years listed.

Any individual taxpayer who wants ADOR to share their Arizona individual income tax information with someone else (such as an attorney, CPA, enrolled agent, or other representative) should complete it. It is also used when you want that person to represent you before ADOR (Power of Attorney).

Disclosure authorization (Section 3) allows ADOR to release confidential information to the appointee. Power of Attorney (Section 4) goes further by allowing the appointee to perform acts the taxpayer could perform regarding the specified tax matters and years, subject to Arizona Supreme Court Rule 31.

No. If you only want ADOR to share information with your appointee, you can leave Section 4 unchecked. Check Section 4 only if you want the appointee to represent you and act for you regarding the listed tax matters and years.

List the specific tax year(s) for which you want ADOR to release information and/or allow representation. If a year is not listed, the authorization generally will not apply to that year.

You must provide the taxpayer name(s), Social Security number(s), current address, and a daytime phone number. If the return involves two taxpayers (e.g., joint filers), include both names and both SSNs.

The appointee must provide a qualifying identification number such as a State Bar number (attorney), Arizona CPA number, IRS Enrolled Agent number, or another Social Security/ID number and type as applicable. The form indicates you should provide one of the listed identification numbers.

Yes. The form allows additional appointees to be listed on a supplemental sheet. Make sure each appointee’s required identifying information is included.

In Section 4, you can specify limitations to the Power of Attorney. Use that space to clearly describe any restrictions (for example, limiting authority to a specific issue, year, or action).

No. By default, this authorization does not revoke earlier authorizations or Powers of Attorney on file with ADOR. To revoke prior authorizations, you must check box 5 and follow the instructions in Section 5.

To revoke all prior authorizations/POAs, check box 5. If you want to revoke only some, check box 5 and list the persons whose authorizations/POAs should remain in effect in the space provided.

The taxpayer(s) must sign and date in Section 6; if there are two taxpayers listed, both should sign. If Power of Attorney is granted (Section 4) or the appointee is otherwise authorized under Rule 31, the appointee must also sign and date the Declaration of Appointee in Section 7.

Section 7 must be completed if the appointee has been given authority under Section 4 (Power of Attorney) or is otherwise authorized to practice law as defined in Arizona Supreme Court Rule 31(a). If it is required and not signed and dated, the representation authorization will be returned.

Yes, under the “Other” designation in Section 7, an individual may be an appointee if the total amount in dispute (including tax, penalties, and interest) is less than $5,000.00. The appointee must still complete and sign the Declaration of Appointee if representation authority applies.

Yes. Section 6 states that knowingly preparing or presenting a fraudulent or false document is a Class 5 felony under A.R.S. §42-1127(B)(2). Provide accurate information and only grant authority you intend to give.

Compliance Arizona Form 285-I

Validation Checks by Instafill.ai

1

Taxpayer name(s) presence and character validation

Verify that at least one taxpayer name is provided and that the field contains plausible name characters (letters, spaces, hyphens, apostrophes) rather than only numbers or symbols. This is important to correctly associate the authorization with the taxpayer’s account and avoid misrouting confidential information. If validation fails, the submission should be rejected and the user prompted to enter the full taxpayer name(s) as shown on the tax return.

2

Taxpayer Social Security Number(s) format and count consistency

Validate that each taxpayer SSN is exactly 9 digits (optionally formatted as XXX-XX-XXXX) and not all zeros or an obviously invalid pattern. If multiple taxpayer names are provided (e.g., joint filers), ensure the number of SSNs matches the number of taxpayers listed or that the form explicitly supports a single SSN entry for both (depending on system rules). If validation fails, block processing because the department cannot reliably identify the taxpayer account.

3

Taxpayer address completeness (street, city, state, ZIP) and ZIP format

Ensure the present address includes street number/name (or rural route), city, state, and ZIP code, and that ZIP is 5 digits or ZIP+4 (##### or #####-####). This is necessary for identity verification, correspondence, and record matching. If incomplete or malformed, the form should be returned for correction or flagged for manual review.

4

Taxpayer daytime phone number format validation

Check that the daytime telephone number includes a valid 10-digit US number (optionally with parentheses/dashes) and does not contain letters or too few digits. A valid phone number is important for resolving processing issues and confirming authorization details. If invalid, require correction or allow submission only if phone is not mandatory per business rules.

5

Appointee name and address completeness validation

Confirm the appointee name is present and that the appointee address includes street, city, state, and ZIP in valid formats. This ensures the authorization is tied to a specific representative and supports contact and compliance requirements. If missing or incomplete, the authorization should not be accepted because the recipient of confidential information is not clearly identified.

6

Appointee identification number requirement (exactly one type provided)

Validate that the appointee provides at least one identification number from the allowed set (State Bar number, AZ CPA number, IRS Enrolled Agent number, or SSN/Other ID with a specified type), and that conflicting multiple IDs are handled per policy (e.g., allow multiple but require one primary). This is critical to confirm eligibility and uniquely identify the representative. If no acceptable ID is provided or the ID type is missing, the form should be rejected.

7

Appointee ID format validation by type

Apply type-specific format rules: State Bar number should match the expected numeric pattern; CPA number should match Arizona CPA numbering rules; Enrolled Agent number should match IRS EA formatting; SSN should be 9 digits; and “Other ID” must include a non-empty type descriptor. Correct formatting reduces misidentification and prevents unauthorized disclosure. If the ID fails validation, require correction or route to manual verification.

8

Tax matters tax year(s) presence and valid year/range validation

Ensure at least one tax year is specified and that each year is a valid four-digit year within an acceptable range (e.g., not in the far future and not unreasonably old per retention rules). This is necessary because the authorization is limited to the years listed and determines what information can be released. If missing or invalid, the form should be returned because the scope of disclosure cannot be determined.

9

Power of Attorney (Section 4) checkbox and limitation text consistency

If the Power of Attorney box in Section 4 is checked, allow optional limitation text but validate that any limitation text is within length limits and does not contain prohibited characters. If the box is not checked, ensure the system does not treat the submission as granting POA even if limitation text is present. If inconsistent (e.g., limitation text provided but box not checked), flag for correction to prevent granting unintended authority.

10

Revocation (Section 5) checkbox and exceptions list consistency

If box 5 is checked, validate whether the user intends to revoke all prior authorizations or only some by checking for an exceptions list; if exceptions are provided, ensure at least one person/entity is clearly identified. If box 5 is not checked, ensure no exceptions list is processed as effective revocation instructions. If inconsistent, reject or require clarification to avoid accidentally revoking or preserving prior authorizations.

11

Taxpayer signature(s) and printed name(s) requirement

Require at least one taxpayer signature and date, and require the corresponding printed name for each signature line used. For joint taxpayers, enforce business rules on whether both spouses must sign (commonly required for joint matters) and ensure the number of signatures aligns with the number of taxpayers listed. If signatures/dates are missing or mismatched, the authorization is not legally effective and must be returned.

12

Signature date format and logical validity

Validate that all dates (taxpayer and appointee) are in an accepted format (e.g., MM/DD/YYYY) and represent real calendar dates. Also check that signature dates are not in the future and are not unreasonably old if the agency imposes timeliness rules. If invalid, the form should be rejected because the execution date is required to establish validity.

13

Appointee declaration (Section 7) required when POA or Rule 31 representation applies

If Section 4 grants Power of Attorney (or if the submission indicates representation beyond simple disclosure), require Section 7 to be completed, signed, and dated by the appointee. This is important because the form states the representation authorization will be returned if the declaration is not signed and dated. If missing, automatically reject/return the submission as incomplete.

14

Appointee designation letter validation (a/b/c/d) and jurisdiction requirement

Validate that the designation is exactly one of the allowed letters (a, b, c, or d) and that the jurisdiction (state) is provided when required by the designation (e.g., attorney licensing jurisdiction). This ensures the appointee’s authority category is clearly established and supports compliance with Arizona Supreme Court Rule 31. If invalid or missing, the form should be returned for correction.

15

Designation-specific conditional fields (Practitioner name and CAF number for 7(c))

If designation 7(c) is selected and the appointee indicates they are engaged in practice with a federally authorized tax practitioner, require the practitioner’s name and CAF number and validate CAF number format (commonly numeric, fixed length per system rules). This is necessary to identify the supervising/associated practitioner and support authorization verification. If required fields are missing or malformed, reject or route to manual review.

16

“Other” designation (7(d)) dispute amount threshold acknowledgment

If designation 7(d) “Other” is selected, require an explicit confirmation or captured value that the total amount in dispute (tax, penalties, and interest) is less than $5,000, if the system collects dispute amount data. This is important because the form limits who may be an “Other” representative based on the dispute amount. If the threshold cannot be confirmed or is exceeded, the submission should be rejected or require a different qualified designation.

Common Mistakes in Completing Arizona Form 285-I

People often submit this form expecting it to cover business taxes, withholding, transaction privilege tax, or other ADOR matters, but it is specifically for individual income tax disclosure/representation. When the tax type doesn’t match, ADOR may not honor the authorization and will continue communicating only with the taxpayer. To avoid this, confirm the issue is individual income tax and that Form 285-I is the correct authorization for the years and matters involved before submitting.

A frequent error is leaving off a spouse’s name/SSN on a joint return, transposing digits, or using a nickname that doesn’t match ADOR records. This can prevent ADOR from locating the account or releasing information, delaying resolution and correspondence. Always enter the full legal name(s) exactly as filed and verify SSNs digit-by-digit (especially for joint filers).

Taxpayers commonly omit the apartment/suite number, provide an old address, or forget the daytime phone number with area code. This can cause notices to go to the wrong place and makes it harder for ADOR to verify identity or resolve questions quickly. Use the current mailing address exactly as used for tax filings and include a reliable daytime phone number with area code.

In Section 2, filers sometimes provide only a name and address but fail to include one of the required identification numbers (AZ Bar number, AZ CPA number, IRS Enrolled Agent number, or SSN/Other ID with type). Without a valid identifier, ADOR may reject or delay processing because the representative cannot be properly verified. Ensure the appointee’s credential number is included and corresponds to the correct credential type.

Many people assume that naming an appointee automatically grants full authority to act, but Section 3 primarily authorizes disclosure of confidential information. If Box 4 is not checked, the appointee may be unable to negotiate, sign agreements, or take actions on the taxpayer’s behalf. Decide whether you need representation authority; if so, check Box 4 and complete any limitations clearly.

A common mistake is leaving the tax years blank, writing vague ranges (e.g., “all years”) without clarity, or listing the wrong years. ADOR may limit disclosure/representation to only the years explicitly stated, which can block the representative from discussing the correct period. List each tax year (or a clearly defined range if accepted) and double-check it matches the years under review or in dispute.

Taxpayers sometimes check Box 4 but forget to describe limits (e.g., “information only,” “no settlement authority,” or “only for audit correspondence”). This can unintentionally grant broader authority than intended, creating risk and confusion for both ADOR and the representative. If you want restrictions, write them explicitly in Section 4; if you want full authority, leave the limitation area blank rather than adding ambiguous notes.

People often check Box 5 thinking it is required, not realizing it revokes earlier authorizations/POAs unless exceptions are listed. This can accidentally cancel an existing representative relationship or remove access for someone still needed on the case. Only check Box 5 if you truly want to revoke prior authorizations, and if keeping some in effect, list the specific persons who should remain authorized.

For joint matters, one spouse may sign while the other does not, or signatures are provided without printed names and dates. ADOR may treat the authorization as incomplete for the non-signing taxpayer, limiting what can be disclosed or represented. Ensure each taxpayer listed signs and dates in Section 6 and prints their name in the corresponding print-name fields.

Section 7 is often skipped even when Box 4 is checked or when the appointee is otherwise required to certify eligibility under Arizona Supreme Court Rule 31. The form itself warns that if the Declaration of Appointee is not signed and dated, the representation authorization will be returned. To avoid rejection, the appointee must select the correct designation (a/b/c/d), provide jurisdiction where applicable, and sign/date the declaration.

Non-attorney/non-CPA/non-EA representatives sometimes choose “Other” without realizing it is only allowed when the total amount in dispute (tax, penalties, and interest) is less than $5,000. If the dispute exceeds the limit, ADOR may reject the representation authority, causing delays and requiring a qualified representative. Confirm the representative’s credential category and, if using “Other,” verify the dispute amount is under the stated threshold.

Saved over 80 hours a year

“I was never sure if my IRS forms like W-9 were filled correctly. Now, I can complete the forms accurately without any external help.”

Kevin Martin Green

Your data stays secure with advanced protection from Instafill and our subprocessors

Robust compliance program

Transparent business model

You’re not the product. You always know where your data is and what it is processed for.

ISO 27001, HIPAA, and GDPR

Our subprocesses adhere to multiple compliance standards, including but not limited to ISO 27001, HIPAA, and GDPR.

Security & privacy by design

We consider security and privacy from the initial design phase of any new service or functionality. It’s not an afterthought, it’s built-in, including support for two-factor authentication (2FA) to further protect your account.

Fill out Arizona Form 285-I with Instafill.ai

Worried about filling PDFs wrong? Instafill securely fills individual-income-tax-disclosure-representation-authorization-form forms, ensuring each field is accurate.