Fill out hardship withdrawal forms

with AI.

Hardship withdrawal forms are essential financial documents for individuals who need to access their retirement savings before reaching the standard retirement age. These forms are typically used when a person faces an immediate and heavy financial burden that cannot be met through other resources. Accessing these funds is a serious decision, as it often involves tax implications and potential penalties, but it provides a critical lifeline for those dealing with urgent life events that require immediate capital.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About hardship withdrawal forms

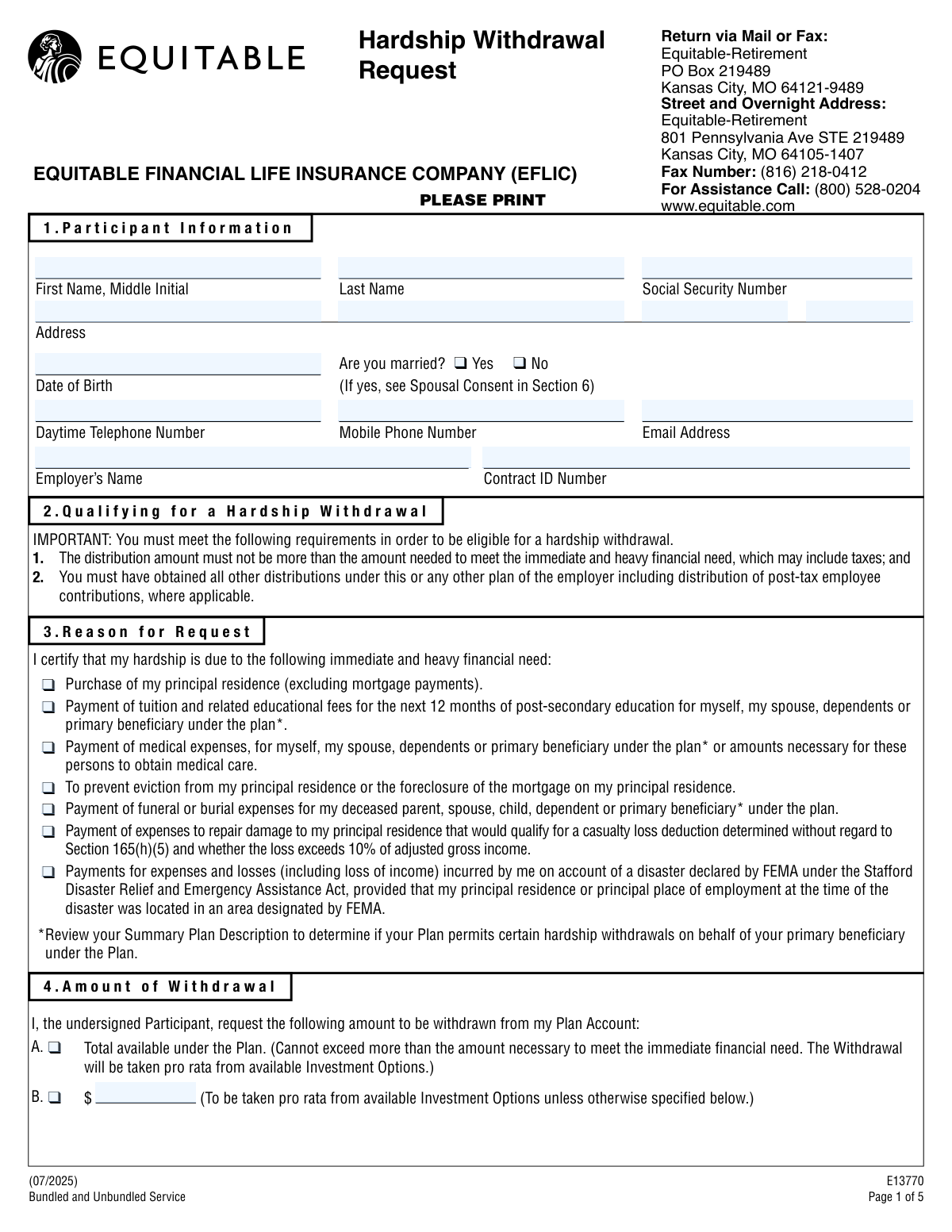

Commonly used by participants in 401(k), 401(a), or other employer-sponsored plans, these forms are required to prove eligibility under IRS-approved categories. This includes situations such as preventing foreclosure or eviction from a primary residence, paying for unreimbursed medical expenses, or covering post-secondary tuition costs. Whether you are using a TIAA Request for Hardship Withdrawal or an Equitable Form E13770, the application process requires precise personal information and specific certifications regarding the nature of the financial emergency. Completing these documents accurately is vital to avoid processing delays during a crisis.

Navigating these complex retirement forms can be stressful during an already difficult time. Tools like Instafill.ai use AI to fill these forms in under 30 seconds, ensuring that data is handled accurately and securely so you can focus on resolving your financial situation. By automating the data entry process, these tools help streamline the submission of these important financial documents.

Forms in This Category

The forms in this category have a median Form Complexity Index of 59/100 (Moderate), measured across 8 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

| Form Name | Pages | FCI | |

|---|---|---|---|

| 1. | Equitable Hardship Withdrawal Request (Form E13770) | 1 | Moderate 55 |

| 2. | Form 2938, Hardship Withdrawal Request | 1 | Moderate 59 |

| 3. | Hardship Withdrawal Request 401(a) Plan | 1 | – |

| 4. | Hardship Withdrawal Request - Empower | 1 | – |

| 5. | MassMutual Application for Hardship Withdrawal | 1 | – |

| 6. | Request for Hardship Withdrawal | 1 | – |

| 7. | Streamlined Hardship Withdrawal Service Letter of Instruction | 1 | Moderate 59 |

| 8. | TIAA Form F11270, Request for Hardship Withdrawal | 1 | – |

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Navigating financial emergencies requires the right paperwork to access your retirement savings quickly. To select the correct form, you must first identify your specific plan provider or the specific IRS code governing your account, as these withdrawals are strictly regulated.

Forms for Specific Plan Providers

Most retirement plan administrators require a form tailored to their internal processing systems. If your employer uses one of the following major providers, select the corresponding document to ensure your request is not rejected:

- Empower: Use the Hardship Withdrawal Request - Empower for 401(k) or similar plans managed by this company.

- MassMutual: Choose the MassMutual Application for Hardship Withdrawal to access vested account balances for medical or housing needs.

- Equitable: Select the Equitable Hardship Withdrawal Request (Form E13770) if your assets are managed specifically by Equitable.

- TIAA: Use the TIAA Form F11270, Request for Hardship Withdrawal for education-related or other TIAA-CREF accounts.

- Transamerica: Look for Form 2938, Hardship Withdrawal Request, which is the standard application for Transamerica-managed plans.

Choosing by Plan Type or Process

If you are not using a standard provider-specific form, your selection may depend on the specific legal structure of your retirement account or the level of documentation required:

- 401(a) Plans: If you are a participant in a government or non-profit 401(a) plan rather than a standard 401(k), use the Hardship Withdrawal Request 401(a) Plan.

- Simplified Instructions: For plans that utilize a simplified instruction process, the Streamlined Hardship Withdrawal Service Letter of Instruction provides a framework for certifying your need quickly.

Key Considerations

Regardless of which form you choose, ensure you have documentation ready for IRS-approved "heavy financial needs," such as medical bills, tuition, or preventing eviction. Most forms, including Form 2938 and the Empower request, will require you to acknowledge potential tax penalties and a temporary suspension of your ability to contribute to the plan. Using AI-powered tools like Instafill.ai can help you complete these complex fields accurately to avoid processing delays during a crisis.

Tips for hardship withdrawal forms

Hardship withdrawals require proof of an immediate and heavy financial need, such as medical bills, tuition invoices, or eviction notices. Having these digital files ready will prevent you from having to restart the application process once you have begun filling out the form.

AI-powered tools like Instafill.ai can complete these complex hardship forms in under 30 seconds with high accuracy. This is a major time-saver for those dealing with urgent financial emergencies, and your sensitive data stays secure during the entire process.

Many filers forget that hardship withdrawals are generally taxable as income and may be subject to a 10% penalty for early distribution. Ensure you calculate the net amount you will receive after withholdings to confirm it actually covers your specific financial need.

Depending on your specific retirement plan, your spouse may need to sign the form in the presence of a notary public. Check the signature section of your Empower or TIAA form early so you can arrange for a notary witness if your plan requires one.

Incorrect plan IDs or bank routing numbers are the leading causes of significant payment delays. Always verify these numbers against your latest account statement or a voided check to ensure the funds are transferred to the correct account without interruption.

Some retirement plans may temporarily suspend your ability to make new contributions after a hardship withdrawal is processed. Review the 'Letter of Instruction' for your specific plan to understand how this withdrawal might impact your long-term retirement savings strategy.

Financial institutions like Equitable or MassMutual frequently update their forms to comply with changing IRS regulations. Always use the latest version available in this category to avoid having your application rejected for using an obsolete document.

Frequently Asked Questions

A hardship withdrawal is an emergency distribution from a retirement account, like a 401(k) or 403(b), made to meet an immediate and heavy financial need. These are typically restricted to specific circumstances defined by the IRS and your plan administrator, and they are generally considered a last resort for financial relief.

You should select the form that corresponds to your specific plan provider, such as Empower, TIAA, or Equitable. If you are unsure who manages your retirement account, check your most recent account statement or contact your employer's Human Resources department to identify the correct administrator.

Most plans follow IRS guidelines which include expenses for medical care, costs related to the purchase of a principal residence, tuition and related educational fees, and payments necessary to prevent eviction or foreclosure. Some plans may also allow withdrawals for funeral expenses or certain repairs to a principal residence due to a casualty loss.

Yes, modern AI tools like Instafill.ai can help you complete these complex financial forms in under 30 seconds. The AI accurately extracts relevant data from your source documents and places it directly into the required fields, reducing the risk of manual entry errors that could delay your application.

While manually filling out these multi-page documents can take 20 to 30 minutes, using an AI-powered service like Instafill.ai allows you to complete the process in less than a minute. This ensures your request is ready for submission much faster than traditional manual methods.

Yes, most plan administrators require proof of the financial hardship, such as medical bills, tuition statements, or foreclosure notices. You should keep copies of all supporting documents as you will likely need to provide them to your plan sponsor or the IRS to justify the distribution.

Completed forms are generally submitted directly to your plan administrator or through your employer's benefits portal. Check the specific instructions on your specific form, such as TIAA Form F11270 or Equitable Form E13770, for the correct mailing address, fax number, or digital upload instructions.

Withdrawing funds early usually results in the amount being treated as taxable income, and you may be subject to an additional 10% early distribution penalty if you are under age 59½. Additionally, taking a withdrawal reduces your total retirement savings and may impact your long-term financial goals.

While the reasons for withdrawal are often similar, the specific plan rules and tax treatments can vary between 401(a) and 401(k) accounts. You must use the specific form designated for your account type to ensure the request is processed correctly by the plan administrator.

Eligibility is typically limited to active participants in an employer-sponsored retirement plan who can demonstrate an immediate financial need that cannot be met by other reasonably available resources. Some plans may require you to have exhausted all available plan loans before you are permitted to apply for a hardship withdrawal.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 59/100 (Moderate). See exactly how it is calculated.

- Hardship Withdrawal

- A distribution from a retirement plan taken before the age of 59½ to meet an immediate and heavy financial need as defined by the IRS.

- Immediate and Heavy Financial Need

- The legal standard required to qualify for a withdrawal, covering specific emergencies like medical expenses, funeral costs, or tuition.

- Vested Balance

- The portion of your retirement account that you legally own, including your contributions and any employer matches you have earned over time.

- Plan Administrator

- The entity or individual responsible for managing the retirement plan and reviewing withdrawal applications to ensure they meet plan and IRS rules.

- Safe Harbor Distribution

- A withdrawal that is automatically considered necessary by the IRS if used for specific reasons, such as preventing eviction or paying for a primary home.

- 10% Early Withdrawal Penalty

- An additional federal tax typically applied to retirement account distributions taken before the age of 59½, in addition to standard income taxes.

- Principal Residence

- The primary home where a participant lives; hardship withdrawals are often permitted for costs related to purchasing or preventing foreclosure on this property.

- Income Tax Withholding

- The amount of a withdrawal that is set aside and sent directly to the IRS to cover taxes, which may be optional or mandatory depending on the plan type.