Fill out W-8 forms

with AI.

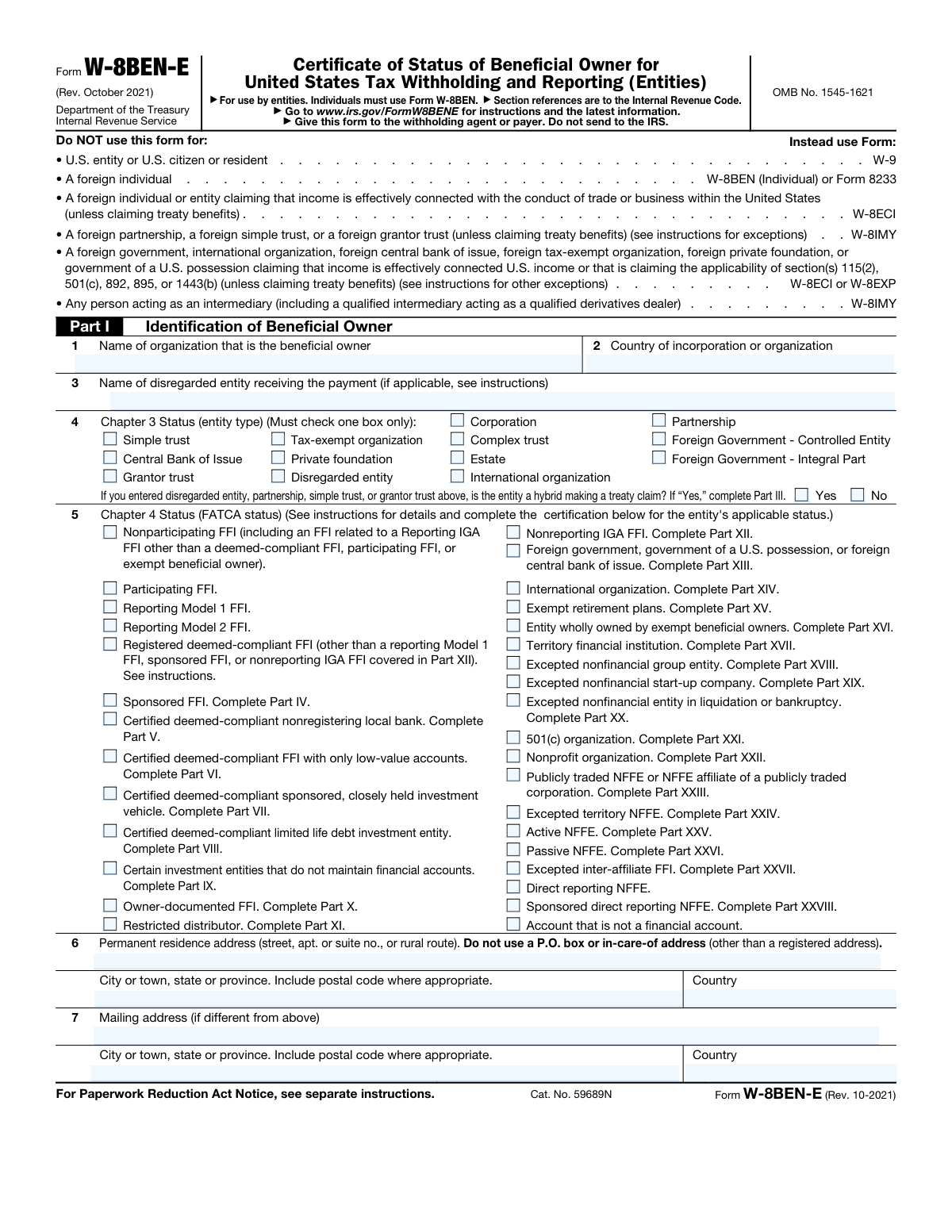

W-8 forms are essential IRS documents used by non-U.S. individuals and entities to certify their foreign status and manage tax withholding on income earned from United States sources. These forms are critical because they determine the correct amount of tax to be withheld from payments like dividends, interest, royalties, or rents. By providing a completed W-8, foreign parties can often claim a reduced rate of withholding or a total exemption based on tax treaties between their home country and the U.S., while also ensuring compliance with the Foreign Account Tax Compliance Act (FATCA).

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About W-8 forms

Typically, these forms are required by foreign corporations, partnerships, and non-resident individuals who engage in business or investment activities within the U.S. financial system. For instance, a foreign entity receiving payments for services or an international investor earning dividends will need to submit a specific version of the form, such as the W-8BEN-E, to their withholding agent or payer. Because these documents are legally binding and impact financial obligations, accuracy in reporting entity types and treaty claims is paramount to avoid the maximum 30% withholding tax rate.

Navigating the technical requirements of tax documentation can be a significant administrative burden for international businesses. Tools like Instafill.ai use AI to fill these forms in under 30 seconds, handling the data accurately and securely to simplify the process. This approach provides a practical way to manage complex paperwork quickly, ensuring that all necessary fields are completed correctly without the need for manual data entry.

Forms in This Category

The forms in this category have a median Form Complexity Index of 46/100 (Moderate), measured across 1 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

| Form Name | Pages | FCI | |

|---|---|---|---|

| 1. | Form W-8BEN-E, Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities) | 1 | Moderate 46 |

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Navigating IRS documentation can be complex, especially when dealing with international tax withholding. While there are several types of W-8 forms, the primary form available in this category is specifically designed for non-U.S. organizations rather than individuals.

For Foreign Organizations and Entities

If you are representing a business or organization, Form W-8BEN-E (Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities)) is the document you need. This form is used exclusively by:

- Foreign Corporations: Businesses incorporated outside the United States.

- Partnerships and Trusts: Legal entities formed under foreign laws.

- Other Organizations: Non-profit organizations or government entities seeking to establish their tax status.

The primary purpose of Form W-8BEN-E is to establish your entity's identity, country of incorporation, and FATCA (Foreign Account Tax Compliance Act) status. By providing this form to a U.S. withholding agent, your entity can claim a reduced rate of withholding or a full exemption under an applicable tax treaty.

Are You an Individual?

It is important to note that Form W-8BEN-E is strictly for entities. If you are a foreign individual receiving U.S.-sourced income (such as dividends, royalties, or compensation for services), you likely need the standard Form W-8BEN (without the "-E"), which is the individual version of this certificate. Using the entity version as an individual will result in an invalid submission.

Why Accuracy Matters

Failing to provide the correct W-8 form or submitting an incomplete one can result in the U.S. payer being required to withhold the maximum tax rate (often 30%) from your payments. Using Instafill.ai to complete your Form W-8BEN-E ensures that you address the complex Chapter 3 and Chapter 4 status requirements accurately, helping your organization remain compliant and minimize unnecessary tax burdens.

Form Comparison

| Form | Purpose | Who Files It | Key Benefit |

|---|---|---|---|

| Form W-8BEN-E, Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities) | Establishes foreign entity identity and FATCA status for U.S. tax reporting purposes. | Foreign corporations, partnerships, or trusts receiving income from United States sources. | Allows entities to claim reduced withholding rates or exemptions under applicable tax treaties. |

Tips for W-8 forms

Ensure you are using the W-8BEN-E for business entities rather than the standard W-8BEN, which is reserved for individuals. Using the wrong form version can result in rejected submissions and incorrect tax withholding rates on your U.S.-sourced income.

One of the most complex parts of the W-8BEN-E is determining your Chapter 4 status. Review your organization’s structure to determine if you are a Participating FFI, Passive NFFE, or another category, as this selection determines which subsequent sections of the form you are required to complete.

AI-powered tools like Instafill.ai can complete these forms in under 30 seconds with high accuracy by mapping your business data directly to the correct fields. Your data stays secure during the process, providing a practical and fast solution for entities managing multiple tax documents.

If your entity is located in a country with a U.S. tax treaty, ensure Part III is filled out completely to qualify for reduced withholding. Missing a single checkbox or failing to cite the specific treaty article can lead to the maximum statutory tax rate being applied to your payments.

If your entity is a Foreign Financial Institution (FFI), you will need your Global Intermediary Identification Number (GIIN) to complete the form. Having this number ready before you begin will prevent interruptions and ensure your FATCA status is properly documented for the withholding agent.

W-8 forms generally remain valid for three full calendar years after the year in which they were signed. It is a best practice to set a reminder to review and renew your forms periodically to avoid unexpected withholding issues caused by expired documentation.

Frequently Asked Questions

W-8 forms are used by non-U.S. individuals and entities to certify their foreign status for tax purposes. These documents help withholding agents determine the correct amount of U.S. tax to withhold from payments made to foreign persons, ensuring compliance with IRS regulations and international tax treaties.

Any foreign person or business entity receiving U.S.-sourced income, such as dividends, interest, royalties, or rent, must typically provide a W-8 form. This includes foreign corporations, partnerships, and individuals who do not hold U.S. citizenship or residency.

The correct form depends on your legal status and the type of income you are receiving. For example, foreign individuals generally use Form W-8BEN, while foreign entities like corporations or trusts use Form W-8BEN-E. Other specialized forms exist for foreign governments, intermediaries, or those claiming income is effectively connected to a U.S. trade or business.

Generally, you do not file W-8 forms directly with the IRS. Instead, you submit the completed and signed form to the withholding agent, payer, or financial institution that is responsible for making payments to you.

Yes, AI tools like Instafill.ai can fill out complex W-8 forms in under 30 seconds by accurately extracting data from your source documents. This technology ensures that information is placed in the correct fields, significantly reducing the risk of errors that could lead to incorrect tax withholding.

While manually completing these forms can be time-consuming due to their technical nature, using an AI-powered service can complete the process in less than a minute. Instafill.ai automates the data entry process, allowing you to generate a professional, accurate PDF quickly.

Most W-8 forms remain valid for the year they are signed plus the three succeeding calendar years. However, if your circumstances change and the information on the form becomes inaccurate, you must provide a new, updated form to your withholding agent immediately.

If you do not provide a valid form, the withholding agent may be legally required to withhold tax at the maximum rate, which is typically 30%. Providing the form allows you to claim a reduced rate of withholding or an exemption based on an applicable tax treaty.

A U.S. TIN or a foreign tax identifying number is often required if you are claiming benefits under a tax treaty. While not always mandatory for the form to be valid for general identification, it is usually necessary to qualify for reduced withholding rates.

Form W-8BEN is a shorter document intended for foreign individuals, whereas W-8BEN-E is a more detailed form for foreign entities like corporations and partnerships. The entity version includes additional sections for FATCA classification and more complex treaty claim requirements.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 46/100 (Moderate). See exactly how it is calculated.

- Beneficial Owner

- The person or entity that is the ultimate owner of the income and has the right to use and enjoy it, rather than just acting as a nominee or agent for someone else.

- Withholding Agent

- The person or organization responsible for deducting U.S. tax from payments made to foreign entities and reporting those amounts to the IRS.

- FATCA (Foreign Account Tax Compliance Act)

- A U.S. law requiring foreign financial institutions and other entities to report on assets held by U.S. account holders to prevent tax evasion.

- GIIN (Global Intermediary Identification Number)

- A unique identification number assigned by the IRS to financial institutions and other entities that have registered for FATCA reporting purposes.

- Tax Treaty

- An agreement between the U.S. and another country that may provide a reduced rate of withholding tax or an exemption for certain types of income.

- Chapter 3 Status

- The classification of a foreign entity (such as a corporation or partnership) used to determine how U.S. tax should be withheld from U.S.-sourced income.

- Chapter 4 Status

- The classification of an entity under FATCA, which determines whether the entity is subject to specific reporting requirements or a 30% withholding tax.

- NFFE (Non-Financial Foreign Entity)

- A foreign entity that is not a financial institution; these are typically categorized as 'active' or 'passive' to determine their FATCA reporting obligations.