Fill out SEPP forms

with AI.

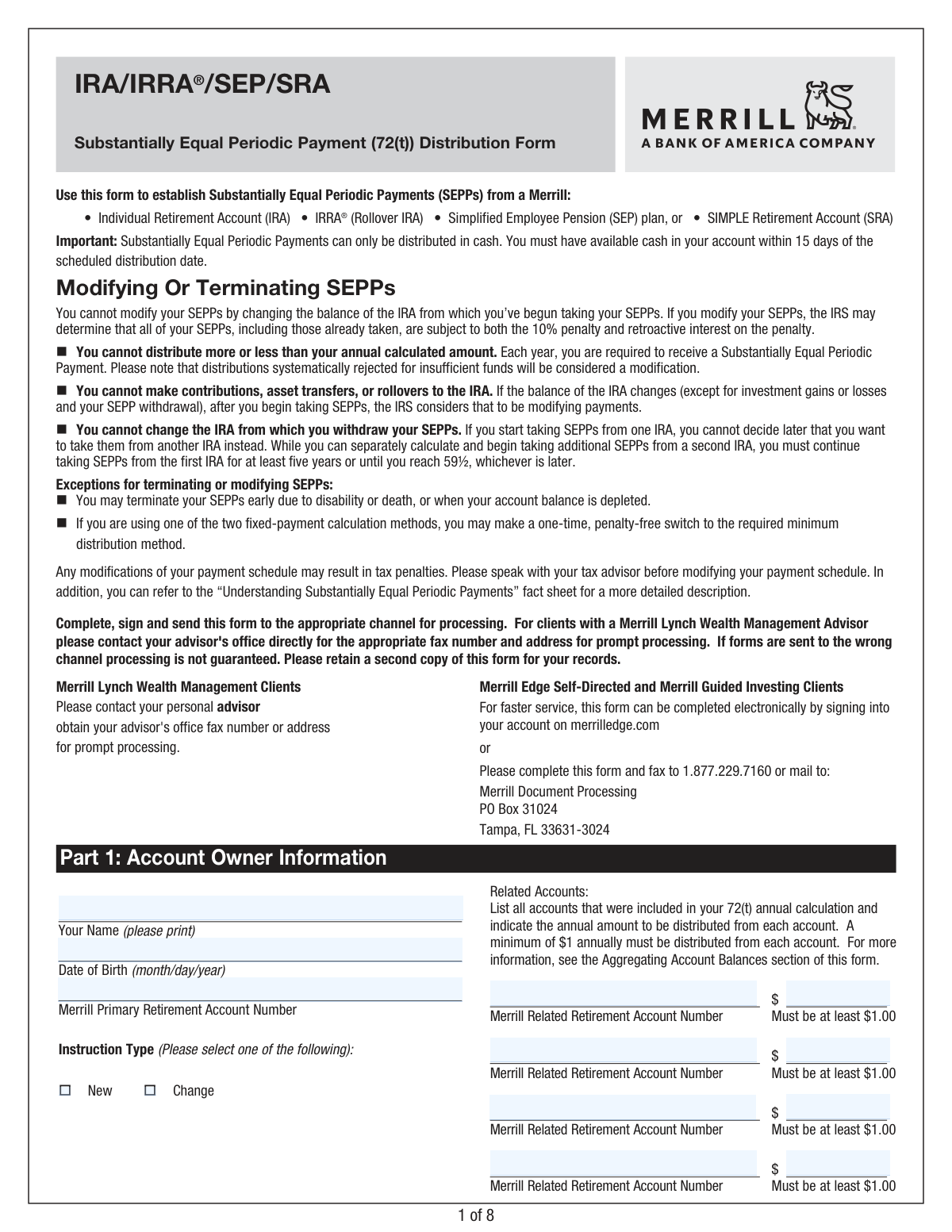

SEPP forms, or Substantially Equal Periodic Payment forms, are specialized documents used by retirement account holders to establish a structured withdrawal plan under IRS Rule 72(t). This rule provides a critical exception for individuals who need to access their retirement savings—such as those in an IRA, SEP, or SRA—before reaching age 59½ without incurring the standard 10% early withdrawal penalty. By committing to a specific schedule of payments based on life expectancy, investors can gain financial flexibility during early retirement or unexpected life transitions while maintaining the tax-advantaged status of their accounts.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About SEPP forms

These forms are typically required by individuals who are retiring early or those who need a steady income stream from their tax-deferred accounts before the federal age threshold. Because the IRS has strict requirements regarding the calculation methods and the duration of these payments, completing these documents accurately is essential to avoid costly tax complications or penalties. Financial institutions require these specific distribution forms to formalize the agreement and ensure that the withdrawal amounts comply with federal regulations.

Managing the paperwork for retirement distributions can be a meticulous process, but modern tools have simplified the task. Platforms like Instafill.ai use AI to fill these forms in under 30 seconds, ensuring that personal and financial data is handled accurately and securely. This allows account holders to focus on their financial planning rather than the complexities of manual form entry.

Forms in This Category

The forms in this category have a median Form Complexity Index of 47/100 (Moderate), measured across 1 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

| Form Name | Pages | FCI | |

|---|---|---|---|

| 1. | Merrill IRA/IRRA®/SEP/SRA Substantially Equal Periodic Payment (72(t)) Distribution Form | 1 | Moderate 47 |

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Substantially Equal Periodic Payments (SEPP) allow you to access retirement funds before age 59½ without incurring the standard 10% IRS early withdrawal penalty. Because these distributions are governed by strict IRS Rule 72(t) regulations, using the correct paperwork for your specific financial institution is critical to maintaining tax compliance.

For Merrill Account Holders

If your retirement assets are managed through Merrill, you should use the Merrill IRA/IRRA®/SEP/SRA Substantially Equal Periodic Payment (72(t)) Distribution Form. This specific document is designed to accommodate several different account structures, including:

- Traditional IRAs and IRRA® accounts: Standard individual retirement arrangements.

- SEP IRAs: Simplified Employee Pension plans for small business owners or the self-employed.

- SRA accounts: Savings Retirement Accounts.

When to Select This Form

You should choose this form if you have already determined your distribution schedule and are ready to commit to a five-year payment plan (or until you reach age 59½, whichever is longer). This form is the right choice when you need to:

- Establish a new series of 72(t) distributions to avoid early withdrawal penalties.

- Formally notify Merrill of your chosen calculation method (such as the amortization, annuitization, or RMD method).

- Designate the frequency of your payments (monthly, quarterly, or annually).

Ensuring Accuracy with AI

Because errors on a 72(t) distribution form can lead to significant tax consequences and retroactive penalties from the IRS, accuracy is paramount. Using Instafill.ai to complete the Merrill IRA/IRRA®/SEP/SRA Substantially Equal Periodic Payment (72(t)) Distribution Form helps ensure that every field is legible and correctly mapped. Before you begin, have your Merrill account number and your calculated annual distribution amount ready to ensure a smooth filing process.

Form Comparison

| Form | Purpose | Eligible Accounts | Primary Benefit |

|---|---|---|---|

| Merrill IRA/IRRA®/SEP/SRA Substantially Equal Periodic Payment (72(t)) Distribution Form | Establishes a schedule of early distributions to avoid the 10% IRS tax penalty. | Traditional IRA, IRRA, SEP, and SRA accounts held with Merrill Lynch. | Allows penalty-free access to retirement funds before age 59½ using IRS Rule 72(t). |

Tips for SEPP forms

The IRS allows three different methods to calculate SEPP payments: required minimum distribution, fixed amortization, or fixed annuitization. Ensure you have calculated your amount correctly based on your preferred method, as switching methods later can be complex and may trigger penalties.

AI-powered tools like Instafill.ai can complete these complex SEPP forms in under 30 seconds with high accuracy. Your sensitive financial data stays secure during the process, providing a fast and reliable way to handle retirement paperwork without manual entry errors.

Since SEPP distributions establish a recurring payment schedule, any error in the account or routing number can lead to missed distributions and potential IRS scrutiny. Always cross-reference your Merrill account number and personal details against your most recent statement before finalizing the document.

Once a SEPP schedule is established, payments must continue for five years or until you reach age 59½, whichever is longer. Avoid making any manual adjustments to the payment amount or frequency, as even a small deviation can result in the IRS retroactively applying the 10% early withdrawal penalty to all prior distributions.

While the 72(t) rule waives the early withdrawal penalty, the distributions are still considered taxable income. Be sure to clearly indicate your federal and state tax withholding preferences on the form to ensure you are not left with a significant tax liability at the end of the year.

Keep a copy of the specific calculations and interest rate data used to determine your payment amount alongside your submitted form. Having this documentation organized and accessible is vital for proving compliance if the IRS ever audits the 'substantially equal' nature of your distributions.

Frequently Asked Questions

SEPP forms, such as those used for Merrill accounts, allow retirement account holders to take early distributions without incurring the standard 10% IRS penalty. By following Section 72(t) of the tax code, individuals agree to receive a series of substantially equal periodic payments over a specific timeframe.

These forms are typically used by individuals under the age of 59½ who need to access funds from their IRA, SEP, or similar retirement accounts before reaching the standard retirement age. It is a strategic option for those who have retired early or need a steady stream of income from their investments.

The IRS provides three specific methods for calculating these payments: the amortization method, the annuitization method, and the required minimum distribution method. You must choose one of these methods when filling out your distribution form to ensure compliance with tax regulations.

Yes, modern AI tools like Instafill.ai can automatically populate these forms by extracting relevant data from your financial records and source documents. This technology ensures that complex information is accurately placed into the correct fields, reducing the risk of manual entry errors.

Using AI-powered services like Instafill.ai, you can complete these forms in under 30 seconds. The system accurately identifies the required fields and maps your data instantly, making the process much faster than manual handwriting or typing.

If you modify or stop the payments before five years have passed or before you reach age 59½ (whichever is later), you may be required to pay the 10% penalty retroactively. This includes interest on the taxes that would have been due in previous years.

This specific form is designed for several types of accounts, including Traditional IRAs, Individual Retirement Rollover Accounts (IRRA), Simplified Employee Pension (SEP) IRAs, and Savings Retirement Accounts (SRA). It is important to ensure your specific account type is supported before initiating the distribution process.

Generally, you submit the completed distribution form directly to your financial institution, such as Merrill, to initiate the payment schedule. While the IRS monitors these distributions through your annual tax filings, the institution is responsible for executing the transfers based on the form you provide.

Yes, the IRS generally requires you to stick to the chosen payment schedule and calculation method for the duration of the SEPP plan. Making unauthorized changes can result in the loss of the penalty exemption and lead to significant back taxes and interest.

No, SEPP forms are specifically for establishing a recurring series of payments designed to last for several years. If you only need a single, one-time distribution, you would typically use a standard early withdrawal form, though it would likely be subject to the 10% early withdrawal penalty.

Yes, platforms like Instafill.ai can take non-fillable or static PDF versions of these distribution forms and convert them into interactive, fillable documents. This allows you to type directly into the form or use AI to populate the fields digitally.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 47/100 (Moderate). See exactly how it is calculated.

- SEPP (Substantially Equal Periodic Payments)

- A method of withdrawing funds from an IRA or other qualified retirement plan before age 59.5 without paying the 10% early withdrawal penalty. To qualify, you must take a series of annual payments for at least five years or until you reach age 59.5, whichever period is longer.

- IRS Rule 72(t)

- The specific section of the Internal Revenue Code that outlines the requirements for penalty-free early distributions from retirement accounts. It serves as the legal basis for the SEPP program.

- 10% Early Withdrawal Penalty

- An additional tax normally imposed by the IRS on retirement account distributions taken before the owner reaches age 59.5. Filling out a SEPP form is a primary way to legally avoid this penalty.

- Amortization Method

- One of the three IRS-approved ways to calculate SEPP payments, which determines a fixed annual amount based on the account balance, an approved interest rate, and life expectancy tables.

- Life Expectancy Method (RMD Method)

- A calculation method where the annual payment is recalculated each year by dividing the account balance by the owner's remaining life expectancy as defined by IRS tables.

- Modification

- Any change to the distribution amount or schedule during the required SEPP period that is not specifically allowed by the IRS. If a modification occurs, the account owner may be required to pay all avoided penalties plus interest retroactively.

- IRRA (Individual Retirement Rollover Account)

- A specific type of IRA used to hold funds that have been moved from a former employer's retirement plan, such as a 401(k), into a personal Merrill account.

- Annuitization Method

- A calculation method that uses an annuity factor based on IRS mortality tables and interest rates to determine a fixed annual distribution amount for the duration of the SEPP plan.