Fill out underwriting forms

with AI.

Underwriting forms are critical components of the risk assessment process in both the insurance and mortgage industries. These documents collect the technical data points and risk indicators that underwriters need to determine whether a policy or loan should be approved and at what price. Whether you are dealing with property insurance forms for commercial habitational risks or standardized mortgage transmittals, the accuracy of these forms is paramount to ensuring compliance and securing favorable terms.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About underwriting forms

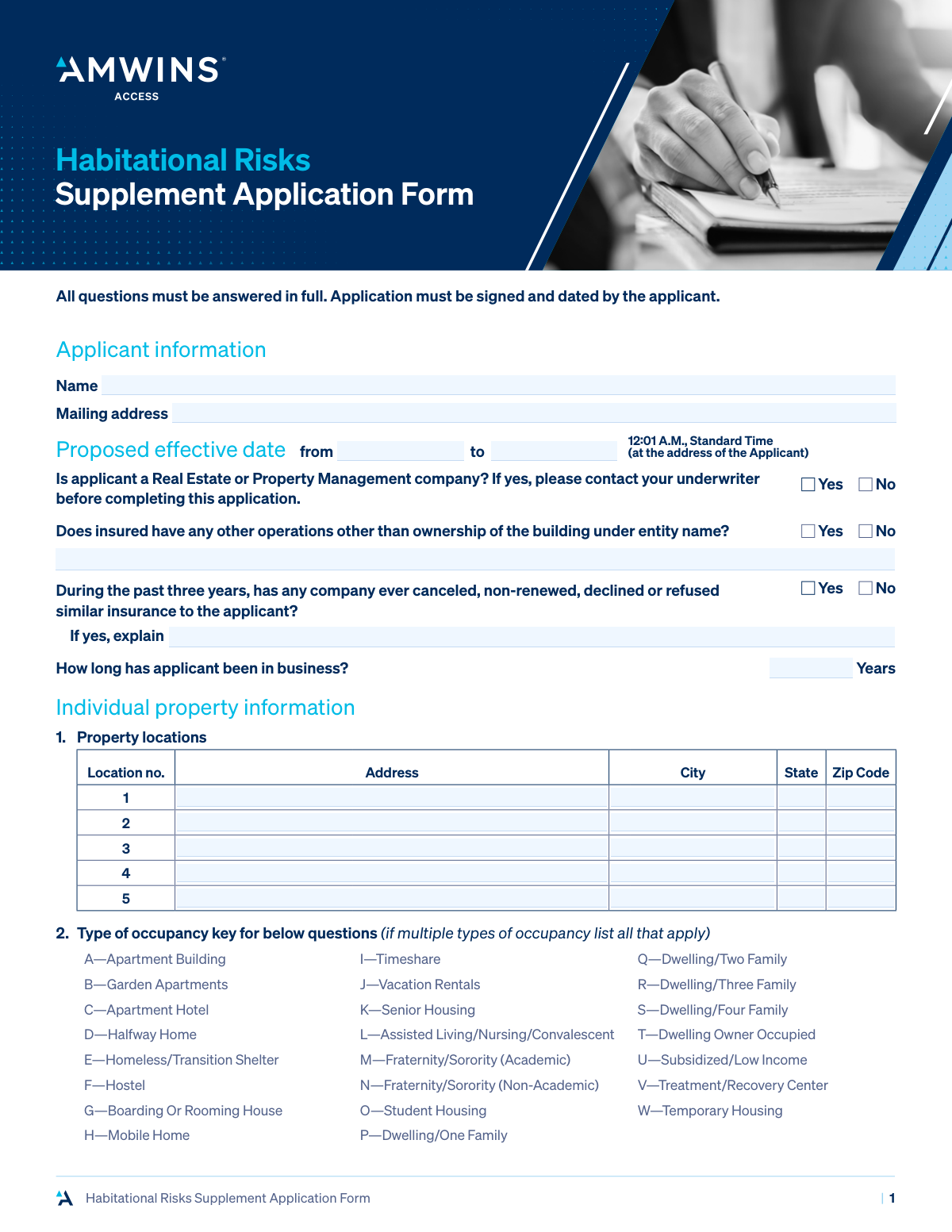

Professionals such as insurance agents, risk managers, and mortgage lenders typically use these forms when submitting new applications or renewing existing coverage. For example, documents like the Habitational Risks Supplement are necessary for evaluating multi-family dwellings, while the Uniform Underwriting and Transmittal Summary (Fannie Mae Form 1008) is a staple for delivering loans to the secondary market. Because these forms serve as the official record for risk analysis, they require precise data entry to avoid processing delays or underwriting errors.

Managing these complex documents manually can be a significant bottleneck in fast-paced financial environments. Tools like Instafill.ai use AI to fill these underwriting forms in under 30 seconds, handling the data accurately and securely to streamline your workflow. This allows professionals to move from data collection to decision-making much faster without compromising on the integrity of the information provided.

Forms in This Category

The forms in this category have a median Form Complexity Index of 74/100 (Complex), measured across 2 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

| Form Name | Pages | FCI | |

|---|---|---|---|

| 1. | Habitational Risks Supplement Application Form | 7 | Complex 74 |

| 2. | Uniform Underwriting and Transmittal Summary (Fannie Mae Form 1008 / Freddie Mac Form 1077) | 1 | Complex 68 |

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Choosing the right underwriting form depends entirely on whether you are assessing a borrower for a mortgage or evaluating a physical property for insurance coverage. Because underwriting is a critical step in risk management, using the correct documentation ensures compliance with industry standards and facilitates faster approvals.

Mortgage Underwriting and Loan Delivery

If you are a lender, mortgage broker, or loan officer preparing a loan file for the secondary market, you need the Uniform Underwriting and Transmittal Summary (Fannie Mae Form 1008 / Freddie Mac Form 1077). This is a mandatory document for delivering conforming mortgage loans to Fannie Mae or Freddie Mac.

Use this form to:

- Summarize borrower income, credit scores, and qualifying ratios.

- Document property details and loan-to-value (LTV) metrics.

- Provide a concise snapshot of the underwriting analysis for investors.

- Serve as the primary cover sheet for the loan transmittal package.

Property and Liability Risk Assessment

If you are an insurance agent or property owner seeking coverage for multi-unit residential buildings, the Habitational Risks Supplement Application Form is the correct choice. This form acts as a vital addendum to a standard commercial insurance application when the property carries unique risks.

Select this form when you need to provide data on:

- Residential Complexes: Specifically for apartment buildings, student housing, or shelters.

- Safety & Maintenance: Details regarding fire alarms, sprinkler systems, and building construction materials.

- Liability Factors: Information on occupancy rates and potential hazards that affect premium calculations.

Which one do you need?

- Choose the Uniform Underwriting and Transmittal Summary if you are finalizing a residential mortgage loan for sale to Fannie or Freddie.

- Choose the Habitational Risks Supplement Application Form if you are applying for property insurance for a multi-tenant residential building.

Both forms can be complex to complete manually. Using Instafill.ai allows you to use AI to accurately extract data and populate these PDF forms, ensuring that critical underwriting data is documented without errors.

Form Comparison

| Form | Industry Focus | Primary Purpose | Key Information Collected |

|---|---|---|---|

| Habitational Risks Supplement Application Form | Property and Casualty Insurance | Assessing risks for insuring residential properties like apartments or student housing. | Safety features, occupancy details, building construction, and potential liability exposures. |

| Uniform Underwriting and Transmittal Summary (Fannie Mae Form 1008 / Freddie Mac Form 1077) | Mortgage Lending and Finance | Summarizing loan data for delivery to Fannie Mae or Freddie Mac. | Borrower income, qualifying ratios, credit risk findings, and property appraisal data. |

Tips for underwriting forms

Underwriting forms often summarize data from dozens of other documents. Double-check that figures like borrower income on Form 1008 or property square footage on a habitational supplement match your primary source records exactly to avoid processing delays.

For habitational risk forms, clearly document recent improvements to electrical, plumbing, or fire suppression systems. Providing specific dates for these upgrades can significantly influence the underwriter’s risk assessment and potentially lower your premiums.

On the Uniform Underwriting and Transmittal Summary, even small errors in Debt-to-Income (DTI) or Loan-to-Value (LTV) ratios can lead to a loan rejection. Re-calculate these figures carefully to ensure they align with secondary market requirements.

AI-powered tools like Instafill.ai can complete complex underwriting forms in under 30 seconds with high accuracy. This is a major time-saver for professionals handling multiple loan or insurance files, and your sensitive data remains secure throughout the process.

Underwriters often return forms that contain empty fields, assuming the information was overlooked. If a section does not apply to your specific risk or loan, enter 'N/A' or '0' rather than leaving it blank to show the form is intentionally complete.

Organize your completed underwriting summaries and supplements in a centralized digital folder. Having a clear record of what was submitted allows you to quickly reference data if an underwriter requests additional clarification or a follow-up audit.

Frequently Asked Questions

Underwriting forms are used by lenders and insurance companies to evaluate the risk associated with a specific applicant or property. They consolidate financial, safety, and background data into a standardized format so underwriters can determine whether to approve a policy or loan and at what rate.

These forms are generally required by property owners, commercial landlords, or insurance brokers representing them. For habitational or commercial insurance, the applicant must provide detailed information about the building's usage, construction, and safety features to secure coverage.

The Uniform Underwriting and Transmittal Summary, also known as Fannie Mae Form 1008 or Freddie Mac Form 1077, is necessary when a mortgage lender intends to sell or deliver a conforming loan to the secondary market. It acts as a concise summary of the borrower's income, property details, and the lender's final risk assessment findings.

Insurers use this supplement to evaluate specific risks inherent in multi-unit residential properties, such as apartment complexes, student housing, or shelters. It helps identify safety measures like fire alarms and sprinkler systems, which directly impact the premium costs and the insurer's decision to offer coverage.

Yes, AI tools like Instafill.ai can fill out complex underwriting forms in under 30 seconds by accurately extracting and placing data from your source documents into the PDF fields. This technology helps ensure that data-heavy forms are completed without the manual errors often associated with traditional data entry.

While manually typing in every field can take 15 to 30 minutes, using an AI-powered service like Instafill.ai allows you to complete these forms in seconds. The system automates the process by identifying where information belongs and populating the form instantly.

Most underwriting forms require supporting documents such as financial statements, property inspection reports, or borrower credit histories. Ensuring these attachments are organized and ready alongside your filled form helps prevent delays in the final underwriting decision.

Completed forms are typically submitted directly to the insurance carrier's underwriting department or to secondary market agencies via secure electronic portals. If you are working with a broker or loan officer, they will usually handle the final submission on your behalf after you have verified the information.

Mortgage-related forms like the 1008 are highly standardized to meet Fannie Mae and Freddie Mac requirements. However, property insurance supplements can vary between different insurance carriers, though they generally focus on the same core safety and occupancy data points.

Accuracy is best maintained by double-checking all financial figures and property specifications against original records before submission. Using automated tools can also help by pulling data directly from verified source files, reducing the risk of typos in critical fields like loan-to-value ratios or square footage.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 74/100 (Complex). See exactly how it is calculated.

- Underwriting

- The formal process used by lenders and insurers to evaluate the risk of a potential client to determine if they qualify for a loan or policy.

- Habitational Risk

- A category of risk used in property insurance to describe multi-unit residential buildings such as apartments, condos, or student housing.

- Debt-to-Income Ratio (DTI)

- A qualifying ratio that compares a borrower's total monthly debt payments to their gross monthly income to determine loan eligibility.

- Loan-to-Value Ratio (LTV)

- A percentage representing the loan amount divided by the property's appraised value, used to assess the level of risk for the lender.

- Secondary Market

- The financial market where mortgage loans are sold by original lenders to entities like Fannie Mae and Freddie Mac to free up capital.

- Conforming Loan

- A mortgage that meets the specific underwriting guidelines and dollar limits set by government-sponsored enterprises for purchase on the secondary market.

- Transmittal Summary

- A standardized cover sheet, such as Fannie Mae Form 1008, that summarizes the key underwriting data and risk assessments for a loan file.

- Loss History

- A record of previous insurance claims made on a property, which underwriters use to predict future claims and determine premium costs.