Fill out homeowners association forms

with AI.

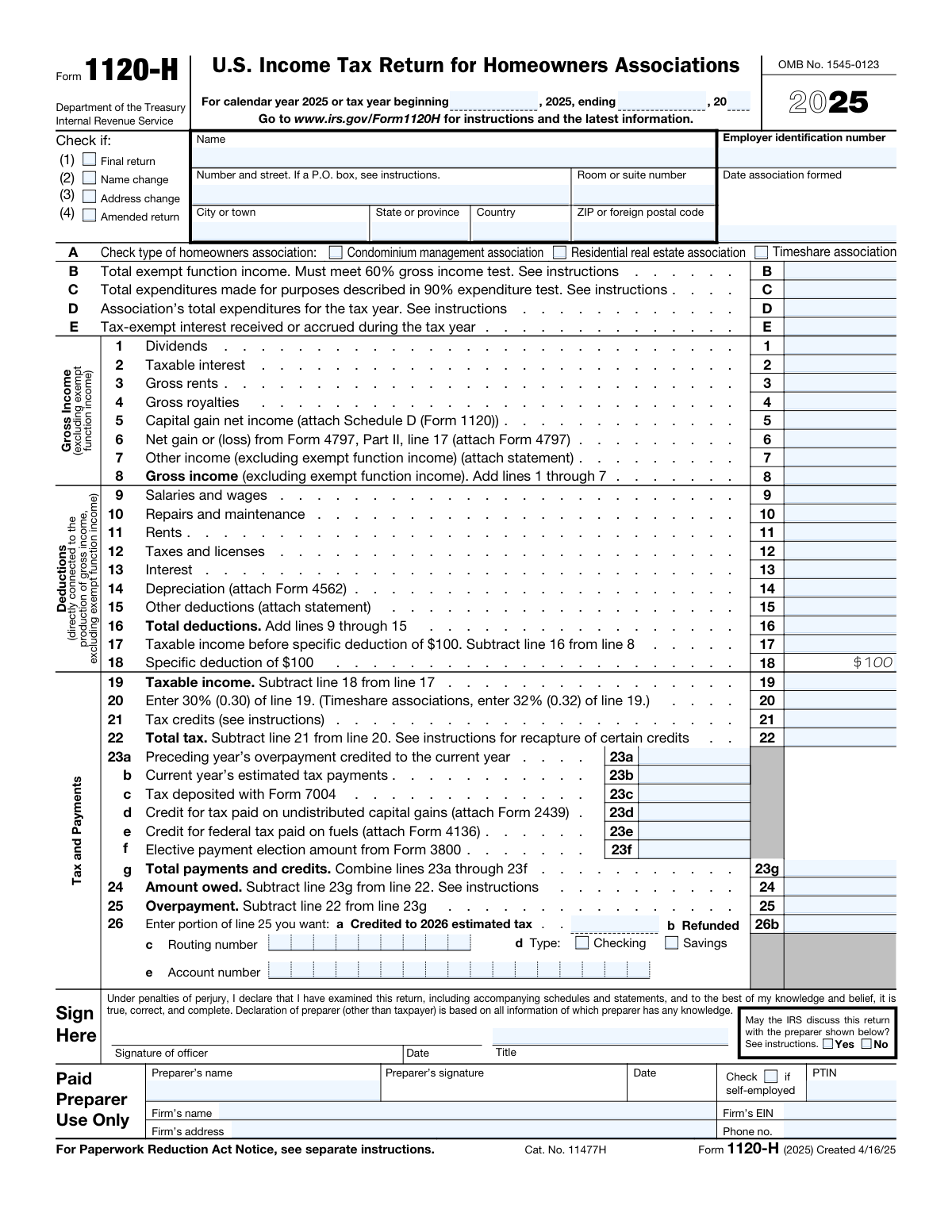

Homeowners association forms cover the administrative and financial paperwork that HOAs, condominium associations, and timeshare associations need to manage their legal and tax obligations. One of the most important documents in this category is IRS Form 1120-H, the U.S. Income Tax Return for Homeowners Associations. This form allows qualifying associations to take advantage of tax benefits under Section 528 of the Internal Revenue Code, separating exempt member-related income from taxable non-exempt income and paying a flat tax rate on the latter.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About homeowners association forms

These forms are typically needed by elected HOA boards, property managers, and the accountants or tax professionals who handle association finances. Filing Form 1120-H correctly is critical — errors or missed deadlines can result in losing the tax election status, which could significantly increase an association's tax liability. Whether you manage a small residential community or a large condominium complex, understanding and accurately completing these forms is an essential part of responsible HOA governance.

For associations handling this paperwork without a dedicated accounting team, tools like Instafill.ai use AI to fill these forms in under 30 seconds, helping ensure the data is entered accurately — a practical time-saver during busy tax seasons.

Forms in This Category

The forms in this category have a median Form Complexity Index of 67/100 (Complex), measured across 1 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

| Form Name | Pages | FCI | |

|---|---|---|---|

| 1. | Form 1120-H, U.S. Income Tax Return for Homeowners Associations | 1 | Complex 67 |

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

With only one form in this category, the decision is straightforward — but it's worth confirming your HOA qualifies before filing.

Who Should File Form 1120-H

Form 1120-H, U.S. Income Tax Return for Homeowners Associations is the right choice if your organization is:

- A condominium management association

- A residential real estate management association

- A timeshare association

...and you want to elect tax-exempt treatment under Section 528 of the Internal Revenue Code.

Key Reasons to Use This Form

- Separate exempt income from taxable income — Member dues, fees, and assessments used for community management are generally excluded from taxation.

- Flat tax rate — Non-exempt income is taxed at a straightforward 30% rate (or 32% for timeshare associations), avoiding the complexity of standard corporate tax brackets.

- Annual election — Filing Form 1120-H is itself the election; you make the choice each tax year.

When Form 1120-H May NOT Be the Right Fit

- If your HOA does not meet the qualifying income or expenditure thresholds under Section 528, you may need to file Form 1120 (standard corporate return) instead.

- If your association is a tax-exempt nonprofit under Section 501(c)(4), a different filing path applies.

Bottom Line

If you're an HOA treasurer or manager looking to minimize your association's tax burden on member-related income, Form 1120-H is your form. Use Instafill.ai to fill it out accurately — the AI-powered tool can even convert non-fillable PDF versions into interactive forms, making the process faster and less error-prone.

Form Comparison

| Form | Purpose | Who Files It | When to Use |

|---|---|---|---|

| Form 1120-H, U.S. Income Tax Return for Homeowners Associations | Report HOA income and pay tax on non-exempt earnings | Qualifying HOAs, condo, timeshare associations | Annually when electing Section 528 tax benefits |

Tips for homeowners association forms

Not every homeowners association automatically qualifies to file Form 1120-H. Your association must meet specific IRS criteria under Section 528, including thresholds for exempt function income and membership composition. Confirm eligibility before filing to avoid submitting the wrong return type.

One of the most common mistakes HOAs make is misclassifying income as exempt when it is actually taxable. Member dues, fees, and assessments used for community upkeep typically qualify as exempt function income, while investment income or rental income from non-members generally does not. Keeping clean, categorized financial records throughout the year makes this separation much easier at tax time.

Standard HOAs pay a flat 30% tax rate on non-exempt income, while timeshare associations pay 32%. Applying the wrong rate is a straightforward error that can trigger IRS notices or penalties. Double-check which category your association falls into before calculating your tax liability.

Choosing to file Form 1120-H is an annual election, meaning your HOA must actively choose it each tax year rather than being locked in permanently. This also means you have the option to evaluate each year whether 1120-H or Form 1120 (the standard corporate return) is more advantageous for your association's financial situation.

AI-powered tools like Instafill.ai can fill out Form 1120-H with high accuracy in under 30 seconds, which is especially helpful for volunteer HOA board members who may not be tax professionals. Your data stays secure throughout the process, and Instafill.ai can even convert non-fillable PDF versions into interactive forms. It's a practical time-saver when managing association finances alongside other board responsibilities.

Before opening Form 1120-H, compile your association's total income, expense records, reserve fund contributions, and any investment account statements for the tax year. Having these figures ready prevents errors from estimating and reduces the need to restart or correct the form mid-way through.

HOAs can deduct ordinary and necessary expenses directly connected to producing non-exempt (taxable) income, which can reduce the overall tax owed. Many associations miss this opportunity by not properly allocating expenses between exempt and non-exempt activities. Working with a CPA familiar with HOA taxation can help ensure you're not overpaying.

Form 1120-H is generally due by the 15th day of the fourth month after the end of the association's tax year, though you should always verify the current deadline with the IRS. Late filing can result in penalties that accumulate quickly, so mark the deadline on your board's calendar well in advance and consider filing for an extension if needed.

Frequently Asked Questions

Homeowners association forms are used by HOAs to manage their legal, financial, and tax obligations. In the context of IRS filings, the primary form in this category—Form 1120-H—is used by qualifying HOAs to file their annual federal income tax return and take advantage of special tax treatment under Section 528 of the Internal Revenue Code.

Form 1120-H is available to three types of qualifying associations: condominium management associations, residential real estate associations, and timeshare associations. Each type must meet specific IRS requirements related to income and expenditure thresholds to be eligible to file using this form.

Filing Form 1120-H allows a qualifying HOA to exclude exempt function income—such as membership dues, fees, and assessments—from taxable income, which can significantly reduce the association's tax burden. While non-exempt income is taxed at a flat rate of 30% (or 32% for timeshare associations), this election is often more favorable than filing a standard Form 1120 corporate return.

Exempt function income generally includes dues, fees, and assessments collected from member homeowners that are used for the management, maintenance, and care of association property. Income from non-member sources or investment income typically does not qualify as exempt function income and is subject to taxation.

HOAs generally follow the same filing deadlines as other corporations, meaning Form 1120-H is typically due on the 15th day of the fourth month after the end of the association's tax year. For HOAs operating on a calendar year, this usually falls in April, though extensions may be available—consult IRS guidelines or a tax professional for your specific situation.

Form 1120-H is submitted to the IRS, either electronically or by mail to the appropriate IRS processing center based on the association's location. The IRS instructions for Form 1120-H provide the correct mailing address depending on the state where the HOA is located.

Filing Form 1120-H is not automatically required—it is an annual election that a qualifying HOA chooses to make. Each year, the association decides whether to file Form 1120-H or a standard corporate return, and the election is made by simply filing the form by the due date.

Yes, AI-powered tools like Instafill.ai can fill out Form 1120-H in under 30 seconds by accurately extracting and placing data from your source documents into the correct fields. Instafill.ai can also convert non-fillable PDF versions of the form into interactive, fillable formats, making the process faster and less error-prone.

Manually completing Form 1120-H can take considerable time, especially when gathering financial data and ensuring accuracy across all fields. Using AI tools like Instafill.ai, the form can be populated in under 30 seconds by automatically extracting relevant information from uploaded documents.

To complete Form 1120-H, an HOA generally needs financial records including total income, exempt function income, non-exempt income, deductible expenses, and any tax credits or payments made during the year. Having organized bookkeeping records and prior-year returns on hand will make the process much smoother.

While it is not legally required to use a tax professional, many HOAs work with a CPA or tax advisor familiar with nonprofit and association tax law to ensure accuracy and compliance. Smaller associations with straightforward finances may be able to file on their own, especially with the help of AI-assisted form tools.

Failing to file on time can result in IRS penalties and interest on any taxes owed. HOAs that need more time can typically request a filing extension, but it's important to note that an extension to file does not extend the deadline to pay any taxes due.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 67/100 (Complex). See exactly how it is calculated.

- Exempt Function Income

- Money collected by an HOA from its members for purposes directly related to the association's core activities, such as membership dues, fees, and assessments used to maintain common areas. This income is excluded from federal taxation when an HOA files Form 1120-H.

- Section 528

- A provision of the Internal Revenue Code that allows qualifying homeowners associations to elect special tax treatment, separating member-related income from taxable income and reducing their overall tax burden.

- HOA Election

- The formal choice an HOA makes each tax year to be treated as a qualifying homeowners association under Section 528 by filing Form 1120-H instead of the standard corporate tax return (Form 1120).

- Non-Exempt Function Income

- Income earned by an HOA from sources unrelated to its member services, such as interest on investments, rental income from non-members, or advertising revenue. This income is subject to a flat federal tax rate of 30% (or 32% for timeshare associations) on Form 1120-H.

- Qualifying Homeowners Association

- An HOA that meets IRS requirements to file Form 1120-H, including conditions such as having at least 60% of gross income come from exempt function income and spending at least 90% of expenses on exempt purposes.

- Timeshare Association

- A type of homeowners association that manages property shared among multiple owners on a rotating schedule. Timeshare associations face a higher flat tax rate of 32% on non-exempt income compared to the standard 30% rate for other qualifying HOAs.

- Condominium Management Association

- An HOA specifically organized to manage the common areas and shared facilities of a condominium complex. These associations are among the eligible entity types that can elect to file Form 1120-H.

- Assessments

- Fees charged by an HOA to its members, typically on a regular basis, to cover the costs of maintaining and operating common areas and shared amenities. Assessments generally qualify as exempt function income on Form 1120-H.

- Flat Tax Rate

- A fixed percentage applied to an HOA's taxable (non-exempt) income on Form 1120-H, regardless of the total amount earned. The IRS sets this rate at 30% for most qualifying associations and 32% for timeshare associations.