Fill out ACORD forms

with AI.

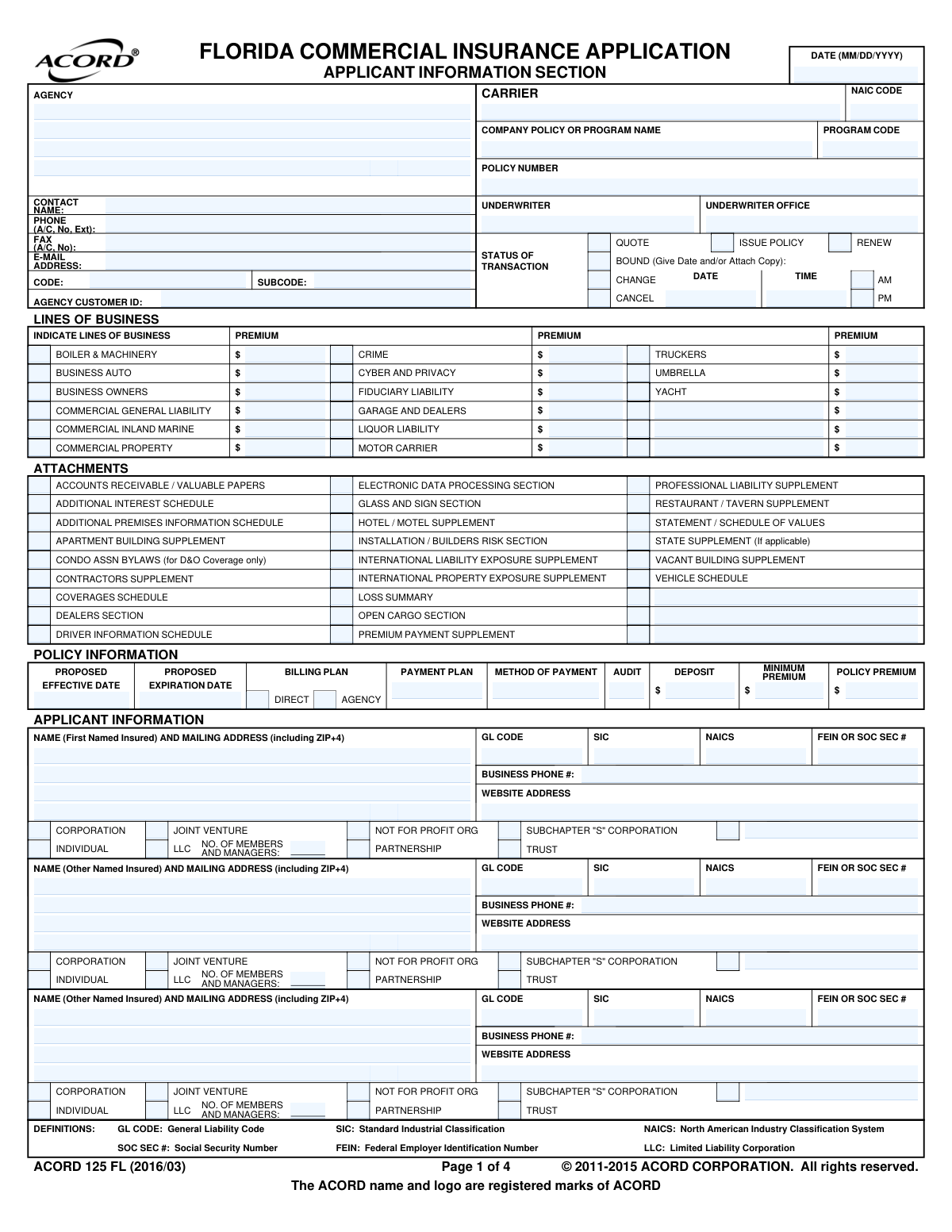

ACORD (Association for Cooperative Operations Research and Development) forms are the universal standard for the insurance industry, designed to streamline the exchange of information between brokers, carriers, and clients. These documents, ranging from insurance application forms to specialized property insurance forms, provide a consistent framework for reporting data, assessing risk, and documenting coverage. Because they are recognized by almost every major insurance provider, using standardized ACORD forms is essential for ensuring that policy information is processed accurately and that there are no gaps in communication during the underwriting process.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About ACORD forms

These forms are typically used by insurance agents, business owners, and independent contractors who need to apply for coverage or verify existing policies. For example, a business might use the ACORD 125 for a commercial application, while a property owner might require dwelling fire forms to protect a residential rental. In many cases, providing a certificate of insurance is a prerequisite for signing contracts or entering job sites, making these documents a vital part of daily business operations. Tools like Instafill.ai use AI to fill these forms in under 30 seconds, handling the data accurately and securely to help you save time on administrative tasks.

Forms in This Category

The forms in this category have a median Form Complexity Index of 66/100 (Complex), measured across 49 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Navigating the extensive library of ACORD forms is simpler when you group them by their primary function: starting a new application, providing proof of coverage, or managing an existing policy.

Commercial Insurance Applications

Most commercial insurance packages begin with ACORD 125 (Commercial Insurance Application), which captures basic applicant information. Depending on the risks you need to cover, you will likely need to attach specific sections:

- General Liability: Use ACORD 126 (Commercial General Liability Section) to detail premises and operations risks.

- Property: Use ACORD 140 (Property Section) for building and contents coverage, often supported by ACORD 139 (Statement of Values) for multiple locations.

- Auto and Transport: Choose ACORD 127 (Business Auto Section) for standard company vehicles, or ACORD 143 (Transportation / Motor Truck Cargo Section) for specialized hauling.

- Workers Compensation: Use ACORD 130 CA for California-specific workers' comp applications.

Certificates and Evidence of Insurance

If a client, landlord, or lender requires proof that you are insured, look for these standardized certificates:

- Liability Proof: ACORD 25 (Certificate of Liability Insurance) is the most common form requested by vendors and clients.

- Property Proof: Use ACORD 27 (Evidence of Property Insurance) or ACORD 28 (Evidence of Commercial Property Insurance) specifically for lenders or loss payees.

- Assets: For specific equipment or vehicles, use ACORD 23 (Vehicle or Equipment Certificate of Insurance).

Personal Lines and Specialty Coverage

For individual or residential needs, select forms based on the asset type:

- Residential: Choose ACORD 80 (Homeowner Application) for standard homes, ACORD 84 (Dwelling Fire Application) for rental properties, or ACORD 85 (Mobile Home Application).

- Personal Liability: Use ACORD 83 (Personal Umbrella Application) for excess liability coverage.

- Marine: Select ACORD 82 (Watercraft Application) for boats or ACORD 81 (Personal Inland Marine Application) for high-value items like jewelry or fine art.

Policy Maintenance

To update an active policy, use ACORD 175 (Commercial Policy Change Request). If you are switching brokers, you will need ACORD 36 (Agent/Broker of Record Change) to formalize the transition.

Form Comparison

| Form | Primary Purpose | Insurance Category | Key Information Collected | Common Use Case |

|---|---|---|---|---|

| ACORD 125, Commercial Insurance Application | Collects general underwriting data for commercial business policies. | Commercial Lines | Business entity type, operations, premises, and prior loss history. | Starting a new application for various commercial insurance coverages. |

| ACORD 126, Commercial General Liability Section | Assesses liability exposures for business operations and products. | Commercial Liability | Premises hazards, contractor info, and products/completed operations. | Applying for general liability coverage to protect against injury claims. |

| ACORD 127, Business Auto Section | Gathers data for underwriting commercial vehicle insurance policies. | Commercial Auto | Vehicle schedules, driver information, and operational use details. | Insuring a fleet of company vehicles or individual business trucks. |

| ACORD 130 CA, California Workers Compensation Application | Provides underwriting information for California workers' compensation coverage. | Workers Compensation | Payroll totals, employee classifications, and specific operational risks. | Securing state-mandated injury coverage for employees in California. |

| ACORD 140, Property Section | Details physical property characteristics for commercial insurance applications. | Commercial Property | Building construction, occupancy, fire protection, and requested limits. | Insuring physical business assets like buildings, equipment, and inventory. |

| ACORD 25, Certificate of Liability Insurance | Summarizes existing liability insurance coverage for third parties. | Proof of Insurance | Policy numbers, liability limits, and effective coverage dates. | Providing proof of insurance to clients or vendors before starting work. |

| ACORD 28, Evidence of Commercial Property Insurance | Provides proof of property insurance to interested stakeholders. | Proof of Insurance | Property limits, deductibles, and details of additional interested parties. | Satisfying a lender's requirement for proof of building insurance. |

| ACORD 75, Insurance Binder | Serves as a temporary legal contract for insurance coverage. | Temporary Coverage | Temporary policy limits, effective dates, and basic coverage terms. | Meeting immediate contractual obligations while the final policy is issued. |

| ACORD 80, Homeowner Application | Standardized application for residential homeowner insurance policies. | Personal Lines | Dwelling construction, replacement cost, and personal loss history. | Applying for insurance on a primary residence or personal property. |

| ACORD 131, Umbrella / Excess Liability Section | Gathers data for liability coverage exceeding primary policy limits. | Umbrella/Excess | Underlying policy details and specific high-limit risk exposures. | Seeking additional catastrophic liability protection for a business. |

| ACORD 160, Property Loss Notice | Initiates the formal reporting of a property insurance claim. | Claims | Date of loss, cause of damage, and property location. | Notifying an insurance carrier of a fire, theft, or weather damage. |

| ACORD 36, Agent/Broker of Record Change | Formally notifies carriers of a change in designated insurance agents. | Policy Management | Policy numbers, effective dates, and new agent of record details. | Transferring the management of existing policies to a new broker. |

Tips for ACORD forms

When filling out the ACORD 125 Commercial Insurance Application, always verify which supplemental sections are required, such as ACORD 126 for liability or ACORD 140 for property. Mismatched or missing sections are a leading cause of underwriting delays and rejected applications.

Remember that forms like the ACORD 25 Certificate of Liability Insurance are for informational purposes only and do not grant coverage or modify the underlying policy. Always refer to the actual policy documents for legal definitions of coverage, as the certificate cannot override policy language.

Small typos in Vehicle Identification Numbers on the ACORD 129 or Federal Employer Identification Numbers on the ACORD 130 can cause significant issues with policy issuance. Verify these numbers against official registration or tax documents to ensure your coverage is legally valid.

Handling dozens of different ACORD forms can be overwhelming, but AI-powered tools like Instafill.ai can complete these forms in under 30 seconds with high accuracy. Your data stays secure during the process, making it a reliable way to manage high-volume insurance paperwork efficiently.

When using the ACORD 37 Statement of No Loss for policy reinstatements, ensure the dates align perfectly with the lapse period. Inaccurate loss reporting on the ACORD 125 or ACORD 80 can lead to premium adjustments or policy cancellation if discrepancies are found later.

For forms like the ACORD 139 Statement of Values, provide specific details for each premises, including construction type and fire protection measures. Grouping multiple distinct buildings under a single entry often triggers requests for more information, slowing down the quoting process.

Some states require specialized versions of standard forms, such as the ACORD 130 CA for California Workers Compensation. Using the generic version when a state-mandated form is available may result in your application being rejected by the carrier or state regulatory boards.

Frequently Asked Questions

ACORD forms are standardized documents used across the insurance industry to ensure consistency in data collection and reporting. They allow agents, brokers, and carriers to process applications, issue certificates of insurance, and manage policy changes efficiently using a format that everyone in the industry recognizes.

Usually, insurance agents or brokers fill out these forms based on information provided by the applicant. However, business owners and individuals often need to review, sign, or provide the raw data for these documents to ensure the underwriting information is completely accurate before submission.

The form you need depends on the type of insurance you are applying for; for example, the ACORD 125 is the standard base for commercial applications, while the ACORD 80 is used for homeowners. You will often need a combination of a base application and specific 'Section' forms, such as ACORD 126 for General Liability or ACORD 127 for Business Auto.

Yes, AI tools like Instafill.ai can automatically fill out ACORD forms by extracting data from your source documents and placing it into the correct fields. This technology ensures that data is transferred accurately from your records directly into the standardized insurance format without manual typing.

Using AI-powered services, you can complete even complex ACORD forms in under 30 seconds. These tools accurately extract and place data from your existing files, which significantly speeds up the application process compared to traditional manual entry.

An ACORD 25 (Certificate of Liability Insurance) is a summary of liability coverage provided to third parties, whereas an ACORD 27 or 28 (Evidence of Insurance) is typically used to prove property coverage to lenders or landlords. While they look similar, they serve different legal purposes regarding who is being notified of the coverage status.

Completed application forms should be submitted to your insurance agent, broker, or directly to the insurance carrier's underwriting department. If you are providing a Certificate of Insurance, you will send the completed form to the 'Certificate Holder,' which is the person or company requesting proof of your coverage.

Supplemental forms allow insurers to gather deep, granular detail about specific risks that aren't covered in a general application. For example, if your business owns a fleet of vehicles, the ACORD 127 Business Auto Section provides the specific driver and vehicle data an underwriter needs to price that specific part of your policy.

An ACORD 75 is used as a temporary legal contract to provide immediate proof of insurance while the formal policy is still being processed by the carrier. It is frequently required during the closing of a business loan or when a new contract requires evidence that coverage is officially 'in force' today.

Most ACORD forms are standardized for use nationwide to maintain industry efficiency. However, some states have specific versions (often indicated by a state abbreviation like 'CA' for California) to comply with local regulations, particularly for Workers' Compensation and Auto Insurance applications.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 66/100 (Complex). See exactly how it is calculated.

- ACORD

- The Association for Cooperative Operations Research and Development is a non-profit organization that creates standardized forms used by almost all insurance carriers and agencies to ensure data consistency.

- Underwriting

- The process an insurance company uses to assess the risk of an applicant, which determines whether they will provide coverage and what the premium cost will be.

- Certificate of Insurance (COI)

- A document, such as the ACORD 25, that serves as a summary of insurance coverage and provides proof to third parties that a policy is active.

- Insurance Binder

- A temporary legal agreement that provides immediate proof of coverage for a short period while the formal insurance policy is being processed and issued.

- Inland Marine

- A category of insurance that covers property that is mobile, in transit over land, or used to facilitate transportation and communication, such as construction equipment or fine arts.

- Loss History

- A record of an applicant's past insurance claims, often required by underwriters to evaluate the likelihood of future losses and to calculate accurate premiums.

- Additional Interest

- A person or entity, such as a lender or landlord, who is added to a policy because they have a financial stake in the insured property or asset.

- Statement of Values (SOV)

- A detailed list of all insured locations and the specific financial value of buildings, contents, and equipment at each site, used primarily for commercial property underwriting.