Fill out charitable distribution forms

with AI.

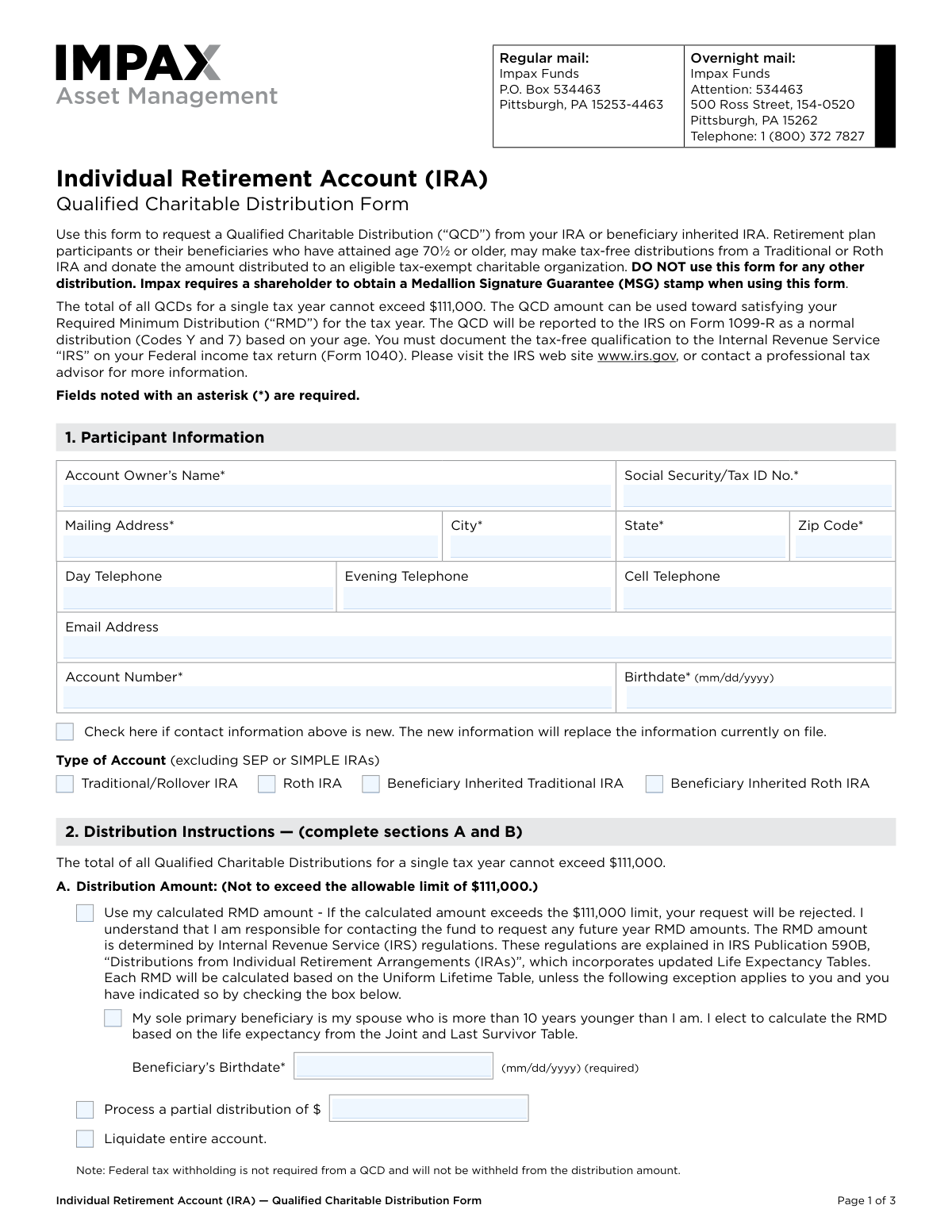

Charitable distribution forms are the essential legal documents used to facilitate the transfer of assets from retirement accounts to non-profit organizations. These forms are primarily centered around the Qualified Charitable Distribution (QCD), a strategic financial move that allows IRA owners to donate directly to a charity. By using these documents, individuals can fulfill their philanthropic goals while simultaneously managing their tax obligations, as these distributions often count toward Required Minimum Distributions (RMDs) without being added to the donor's adjusted gross income.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About charitable distribution forms

This category is most relevant for individual retirement account holders who have reached the age of 70½, as well as representatives of charitable organizations acting as beneficiaries. You might encounter these forms when requesting a direct transfer from a brokerage account at institutions like Vanguard or TIAA, or when a charity needs to claim assets from a deceased donor's estate. Because these transactions involve sensitive financial data and strict IRS regulations, ensuring that every detail—from account numbers to tax identification information—is recorded correctly is vital for a seamless transfer.

Completing these documents doesn't have to be a manual burden; tools like Instafill.ai use AI to fill these forms in under 30 seconds, handling your data with high accuracy and security. This streamlined approach helps donors and non-profit administrators save time on administrative tasks, allowing them to focus more on the charitable mission at hand.

Forms in This Category

The forms in this category have a median Form Complexity Index of 43/100 (Basic), measured across 8 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Navigating charitable distributions from an IRA depends on your role—whether you are the account owner giving a gift or a non-profit organization receiving one—and which financial institution holds the funds. Use this guide to select the document that matches your specific situation.

If You Are the IRA Owner (Making a Gift)

If you are age 70½ or older and want to make a tax-free donation to satisfy your Required Minimum Distribution (RMD), you need a Qualified Charitable Distribution (QCD) form. Your choice depends on where your account is held and the specific account type:

- For TIAA Brokerage Accounts: Use the Request for a Qualified Charitable Distribution (QCD) from a Brokerage Individual Retirement Account (IRA) (Form F41205).

- For TIAA Trust or Standard IRAs: Select either the Request for qualified charitable distribution from individual retirement account (TIAA Trust, N.A.) or the Request for a Charitable Distribution from an Individual Retirement Account (IRA) (Form F11185).

- For Other Institutions: If your provider does not have a proprietary form, the Sample IRA Distribution Letter for a Qualified Charitable Distribution (QCD) serves as a professional template to formally request a direct transfer from your IRA to a charity.

If You Are a Charity (Claiming an Inheritance)

When a donor passes away and leaves their IRA assets to a non-profit, the organization must file specific paperwork to claim the inheritance. These forms allow the charity to provide its tax identification number and liquidation instructions.

- For General Vanguard IRAs: Use the standard IRA Distribution to Charitable Beneficiary form.

- For Vanguard Brokerage IRAs: Use the specific IRA Distribution to Charitable Beneficiary (Form DIRDISTVBA) to handle assets specifically held within a brokerage-style retirement account.

Choosing the correct form ensures the distribution is coded properly for tax purposes, preventing the donor from being taxed on the gift and ensuring the charity receives the funds without legal delays.

Form Comparison

| Form | Primary Purpose | Who Files It | Key Benefit |

|---|---|---|---|

| Sample IRA Distribution Letter for a Qualified Charitable Distribution (QCD) | Template for requesting a direct transfer from an IRA to a charity. | IRA account owners who are aged 70.5 or older. | Satisfies Required Minimum Distributions without increasing the owner's taxable income. |

| IRA Distribution to Charitable Beneficiary | Claiming assets from a deceased individual's Vanguard IRA account. | The designated charitable organization named as the account beneficiary. | Facilitates the legal and tax-exempt transfer of inherited retirement assets. |

| IRA Distribution to Charitable Beneficiary — Form DIRDISTVBA | Claiming inheritance from a deceased owner's Vanguard Brokerage IRA. | The non-profit organization designated as the beneficiary on the account. | Enables asset liquidation and proper delivery of funds to the charity. |

| Request for a Qualified Charitable Distribution (QCD) from a Brokerage Individual Retirement Account (IRA) | Directing a tax-free donation from a TIAA brokerage IRA to charity. | TIAA brokerage account holders aged 70.5 or older. | Provides a tax-efficient way to give while satisfying annual RMD requirements. |

| Request for qualified charitable distribution from individual retirement account | Authorizing TIAA Trust to make a direct distribution to a charity. | TIAA Trust IRA account holders aged 70.5 or older. | Allows for donations up to annual limits without incurring taxable income. |

| Request for a Charitable Distribution from an Individual Retirement Account (IRA) | Requesting a direct payment from a standard TIAA IRA to charity. | TIAA IRA account holders aged 70.5 or older. | Excludes the distributed amount from the owner's taxable gross income. |

Tips for charitable distribution forms

Handling multiple charitable distribution requests can be time-consuming and repetitive. AI-powered tools like Instafill.ai can complete these forms in under 30 seconds with high accuracy while ensuring your sensitive financial data stays secure throughout the process.

A common mistake is withdrawing funds personally before donating them, which can trigger an unintended tax liability. To qualify as a tax-free distribution, the check or transfer must be made payable directly from the IRA custodian to the eligible 501(c)(3) organization.

Before filling out your distribution letter, double-check that the recipient is a qualified charitable organization. You will need their legal name and Employer Identification Number (EIN) to ensure the distribution is processed correctly by your brokerage or bank.

If you are over the age of 72, you can use these forms to satisfy your Required Minimum Distribution (RMD) for the year. Coordinating the distribution amount with your RMD can significantly reduce your adjusted gross income and provide substantial tax savings.

When requesting a distribution from a brokerage account, specify exactly which assets or funds should be liquidated to cover the donation. Providing clear instructions on the form prevents processing delays and ensures the correct amount is sent to the beneficiary.

While the distribution may be tax-free, you must still report it correctly on your tax return. Always keep a copy of the completed distribution form and the written acknowledgment from the charity to prove the funds were received as a direct transfer.

Frequently Asked Questions

A QCD is a direct transfer of funds from your IRA custodian, payable to a qualified charity. It allows eligible individuals to donate to a non-profit while potentially reducing their taxable income by excluding the distribution from their adjusted gross income.

Generally, individuals who are age 70½ or older are eligible to make a Qualified Charitable Distribution from their IRA. For beneficiary-specific forms, the authorized representative of a charitable organization must complete the paperwork to claim inherited assets from a deceased individual's account.

You should select the form that corresponds to your specific financial institution, such as TIAA or Vanguard, where your IRA is held. If your custodian does not provide a specific document, a 'Sample IRA Distribution Letter' can serve as a formal template to request the transfer.

Yes, a QCD can satisfy all or part of your annual RMD for the year. By using these forms to transfer funds directly to a charity, you fulfill your withdrawal requirements without the amount being added to your taxable income.

A standard QCD request form is used by the living account owner to donate funds to a charity. In contrast, a beneficiary distribution form is used by a charitable organization to claim its inheritance from a deceased individual's IRA.

Completed forms should be submitted directly to the financial institution or brokerage firm that holds the IRA account. Most custodians provide specific mailing addresses, fax numbers, or secure online upload portals for these documents.

Yes, you can use AI tools like Instafill.ai to complete these forms with high accuracy. The AI can extract necessary data from your source documents and place it into the correct fields, ensuring that account numbers and charitable details are entered correctly.

Using AI-powered platforms like Instafill.ai, these forms can often be completed in under 30 seconds. This process automates the data entry for complex fields, making it much faster than manual typing or handwriting.

The IRS sets an annual maximum limit for Qualified Charitable Distributions per individual. While these forms allow you to authorize a distribution, you should verify the current tax year's limit to ensure your donation stays within the tax-free threshold.

You will typically need your IRA account number, the legal name of the charitable organization, their Federal Tax ID number (EIN), and the specific dollar amount to be transferred. If you are claiming as a beneficiary, you may also need the deceased account holder's information.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 43/100 (Basic). See exactly how it is calculated.

- Qualified Charitable Distribution (QCD)

- A direct transfer of funds from an Individual Retirement Account (IRA) to a qualified 501(c)(3) charity. This distribution allows the account owner to donate to a cause without the funds being counted as taxable income.

- Required Minimum Distribution (RMD)

- The minimum amount the IRS requires retirement account holders to withdraw annually once they reach a specific age. Using a QCD can satisfy all or part of this annual withdrawal requirement.

- Direct Transfer

- A transaction where funds move directly from the financial institution to the charitable organization. To qualify for tax benefits, the money must never be paid out to the account holder first.

- Charitable Beneficiary

- A non-profit organization named in a retirement account agreement to receive the remaining assets upon the death of the account holder. This designation allows the charity to claim the funds through specific distribution forms.

- Age 70 ½ Rule

- The specific age milestone at which an IRA owner becomes eligible to make tax-free charitable distributions. Even if the RMD age has increased, the eligibility for QCDs remains at 70 ½.

- Asset Liquidation

- The process of selling stocks, bonds, or mutual funds within a brokerage IRA to convert them into cash. This is often necessary before a financial institution can issue a payment to a charitable organization.

- Taxable Income Exclusion

- A tax advantage where the amount of a charitable distribution is subtracted from the donor's adjusted gross income. This can help the donor stay in a lower tax bracket and potentially reduce the taxation of Social Security benefits.