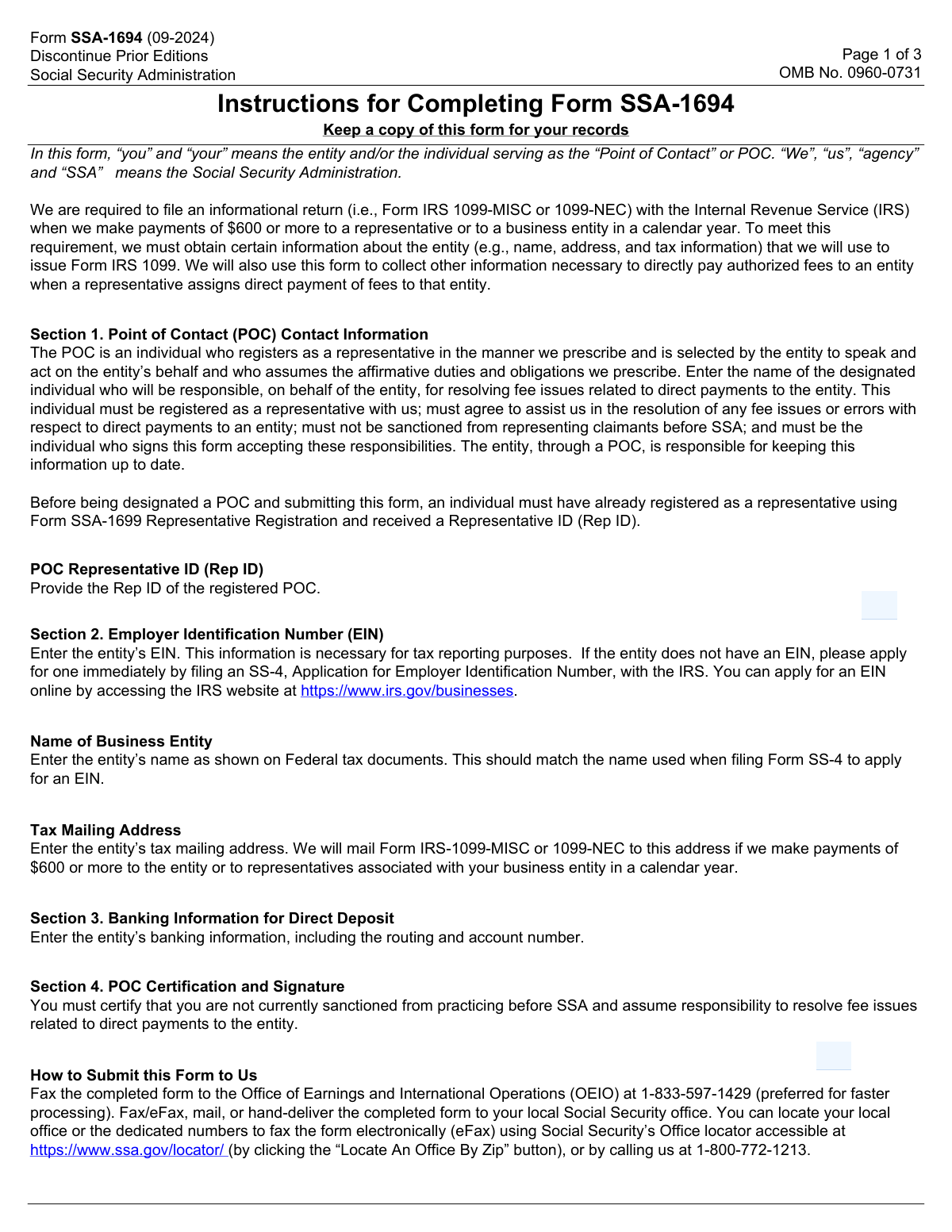

Fill out entity tax forms

with AI.

Entity tax forms are IRS certificates used by foreign organizations to establish their tax status, identity, and eligibility for reduced withholding rates when receiving U.S.-sourced income. These forms play a critical role in the U.S. tax withholding and reporting system, ensuring that payments made to foreign entities are properly documented and taxed at the correct rate. Getting them right matters — errors or omissions can result in the maximum withholding rate being applied, which can significantly impact an organization's cash flow.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About entity tax forms

These forms are typically needed by foreign corporations, partnerships, trusts, intermediaries, and flow-through entities that receive income from U.S. sources such as dividends, interest, royalties, or other payments. For example, Form W-8BEN-E is used by foreign entities to claim treaty benefits and establish FATCA status, while Form W-8IMY is used by intermediaries and flow-through entities acting on behalf of other payees. Both forms are provided directly to withholding agents or payers rather than filed with the IRS, but they must be accurate and kept current.

Because these forms involve detailed entity classifications, treaty provisions, and FATCA compliance requirements, they can be time-consuming and confusing to complete. Tools like Instafill.ai use AI to fill these forms in under 30 seconds, helping organizations handle the documentation accurately and securely without getting bogged down in complex IRS instructions.

Forms in This Category

The forms in this category have a median Form Complexity Index of 67/100 (Complex), measured across 2 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Both forms on this page are IRS withholding certificates for foreign entities receiving U.S.-source income — but they serve distinct roles. Here's how to tell which one you need.

You Are the Direct Beneficial Owner of the Income

If your foreign entity (corporation, partnership, trust, or other organization) is the actual beneficial owner of the U.S.-source income — meaning you're receiving it for your own account, not passing it through to others — choose Form W-8BEN-E.

- Use it to establish your entity's Chapter 3 status and FATCA (Chapter 4) classification

- Use it to claim treaty benefits or reduced withholding rates

- Required by the withholding agent before payments are made; incorrect or missing documentation triggers the maximum withholding rate

You Are Acting as an Intermediary or Flow-Through Entity

If your entity is receiving income on behalf of others — or if payments will flow through your entity to underlying payees — choose Form W-8IMY.

- Applies to qualified intermediaries (QIs), nonqualified intermediaries (NQIs), foreign partnerships, foreign grantor trusts, and qualifying U.S. branches of foreign banks or insurers

- Must typically be accompanied by a withholding statement and the underlying payees' own documentation (e.g., W-8BEN-E or W-9 forms)

- Used by withholding agents to determine how to allocate withholding across multiple payees

Quick Decision Summary

| Situation | Form to Use |

|---|---|

| Foreign entity is the beneficial owner | W-8BEN-E |

| Entity acts as intermediary or passes income through | W-8IMY |

| Claiming a tax treaty benefit for your entity | W-8BEN-E |

| Submitting on behalf of multiple underlying payees | W-8IMY |

Neither form is filed with the IRS — both are provided directly to your withholding agent or payer. Update whichever form you use promptly if any certified information changes.

Form Comparison

| Form | Purpose | Who Files It | When to Use |

|---|---|---|---|

| Form W-8IMY (Rev. October 2021), Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S. Branches for United States Tax Withholding and Reporting | Certify intermediary or flow-through entity status for withholding | Foreign intermediaries, flow-through entities, or U.S. branches | When receiving U.S.-source income on behalf of other payees |

| Form W-8BEN-E, Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities) | Certify foreign entity status as beneficial owner for withholding | Foreign entities (corporations, partnerships, trusts, organizations) | When receiving U.S.-source income directly as the beneficial owner |

Tips for entity tax forms

W-8BEN-E is for foreign entities claiming beneficial owner status on U.S.-sourced income, while W-8IMY is for intermediaries, flow-through entities, or U.S. branches acting on behalf of others. Submitting the wrong form can cause withholding delays or result in the maximum tax rate being applied. Identify your entity's exact role in the payment chain before selecting a form.

Both forms require you to classify your entity under Chapter 3 (NRA withholding) and Chapter 4 (FATCA) rules, and selecting the wrong classification is one of the most common errors. Review IRS instructions carefully to identify which entity type and FATCA status applies to your organization. Getting this right upfront prevents rejection by withholding agents and avoids backup withholding.

A frequent mistake is attempting to file W-8BEN-E or W-8IMY directly with the IRS — these forms are provided to your withholding agent or payer, not submitted to the tax authority. Make sure you deliver the completed form to the financial institution, broker, or counterparty requesting it. Keep a copy for your records in case the form needs to be referenced or updated later.

The W-8IMY almost always requires a withholding statement and underlying payee documentation (such as W-8BEN or W-8BEN-E forms for each beneficial owner). Submitting the W-8IMY without these attachments is a common reason withholding agents reject or return the form. Prepare all supporting documents in advance so the full package can be submitted together.

These certificates generally remain valid for three years from the date of signing, but they become invalid immediately if any certified information changes — such as a change in entity status, country of incorporation, or FATCA classification. Set a reminder to review and resubmit before expiration to avoid gaps in your withholding documentation. Withholding agents may apply maximum withholding rates if an expired or incorrect form is on file.

AI-powered tools like Instafill.ai can complete entity tax forms like W-8BEN-E and W-8IMY in under 30 seconds with high accuracy, reducing the risk of classification errors or missing fields. Your data stays secure throughout the process, making it a practical option for finance teams managing multiple foreign entity certifications. This is especially useful when working against tight deadlines from withholding agents or financial institutions.

If your entity is claiming a reduced withholding rate under a tax treaty on the W-8BEN-E, confirm that the treaty is currently in force and that your entity type qualifies for the specific benefit being claimed. Treaty provisions vary significantly by country and income type, and an incorrect treaty claim can trigger back-withholding. Cross-reference the IRS's published list of tax treaties before completing the treaty article sections.

Both forms must be signed by an authorized representative of the entity, and the signature must include the signer's capacity (e.g., director, officer, or authorized agent). Unsigned or improperly signed forms will be rejected by withholding agents, causing payment delays. If signing under a power of attorney, attach the relevant documentation as required by the withholding agent.

Frequently Asked Questions

Entity tax forms in this category are IRS certificates used by foreign entities and intermediaries to establish their tax status for U.S. withholding and reporting purposes. They allow withholding agents and payers to determine the correct rate of tax to withhold on U.S.-sourced income payments. Providing the correct form helps entities avoid the default maximum withholding tax rate.

Form W-8BEN-E is used by foreign entities that are the beneficial owners of U.S.-sourced income, such as foreign corporations or trusts claiming treaty benefits. Form W-8IMY, on the other hand, is used by entities acting as intermediaries, flow-through entities, or qualifying U.S. branches that are receiving income on behalf of others. The key distinction is whether the entity is the ultimate beneficial owner of the income or is passing it through to underlying payees.

Foreign entities — including corporations, partnerships, trusts, and other organizations — that receive U.S.-sourced income such as dividends, interest, royalties, or other fixed or determinable annual or periodical (FDAP) income need to complete Form W-8BEN-E. It is provided to the withholding agent or payer, not submitted directly to the IRS. Failure to provide this form can result in the payer applying the maximum withholding tax rate.

Form W-8IMY is designed for entities acting as intermediaries — such as qualified intermediaries (QIs), nonqualified intermediaries (NQIs), foreign partnerships, foreign simple or grantor trusts, and qualifying U.S. branches of foreign banks or insurance companies. These entities receive U.S.-sourced payments on behalf of others and must certify their Chapter 3 and Chapter 4 (FATCA) status. It is typically submitted along with a withholding statement and documentation for the underlying payees.

No — both Form W-8BEN-E and Form W-8IMY are provided directly to the withholding agent or payer (such as a bank, broker, or other financial institution), not filed with the IRS. The withholding agent retains the forms as documentation to support their withholding and reporting decisions. However, the IRS may request these forms during an audit or review of the withholding agent's records.

Generally, W-8 forms remain valid for three calendar years after the year in which they are signed, unless a change in circumstances makes the information on the form incorrect. For example, a form signed in 2023 would typically remain valid through the end of 2026. Entities must promptly update their form if any certified information changes, such as a change in tax treaty eligibility or FATCA status.

FATCA (Foreign Account Tax Compliance Act) is a U.S. law requiring foreign financial institutions and certain other entities to report information about U.S. account holders to the IRS. Both W-8BEN-E and W-8IMY require entities to certify their Chapter 4 (FATCA) status, which determines whether they are compliant, exempt, or subject to FATCA withholding. Providing the correct FATCA classification is essential to avoid an additional 30% withholding on certain payments.

Yes — Form W-8BEN-E allows foreign entities to claim reduced withholding rates or exemptions under an applicable U.S. income tax treaty by identifying the treaty country and the specific treaty article being claimed. Form W-8IMY does not itself claim treaty benefits on behalf of underlying payees, but it may accompany documentation from those payees who are claiming treaty benefits. The withholding agent uses this information to apply the appropriate withholding rate.

Yes — AI-powered tools like Instafill.ai can fill out forms such as W-8BEN-E and W-8IMY in under 30 seconds by accurately extracting and placing data from your source documents. This significantly reduces the risk of errors that can lead to incorrect withholding or rejected documentation. Instafill.ai can also convert non-fillable PDF versions of these forms into interactive, fillable formats.

Manually completing forms like W-8BEN-E or W-8IMY can take significant time due to their complexity, including FATCA classifications, treaty claims, and withholding statements. Using AI tools like Instafill.ai, the data extraction and form-filling process can be completed in under 30 seconds, with information accurately pulled from your existing business or tax documents. This is especially useful for entities that need to provide updated forms to multiple withholding agents.

If a foreign entity fails to provide the appropriate W-8 form to a withholding agent, the payer is generally required to apply the maximum withholding tax rate — currently 30% — on U.S.-sourced income payments. This can significantly reduce the amount the entity receives and may create complications for reclaiming over-withheld amounts. Providing a correctly completed and timely form ensures the appropriate withholding rate is applied from the outset.

These forms are primarily required for passive income types such as interest, dividends, royalties, rents, and similar fixed or determinable annual or periodical (FDAP) income from U.S. sources. They may also be relevant in certain effectively connected income (ECI) scenarios. The specific income types and withholding obligations depend on the entity's status, the nature of the income, and any applicable tax treaties.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 67/100 (Complex). See exactly how it is calculated.

- Withholding Agent

- A person or entity (such as a bank, broker, or payer) responsible for deducting and remitting U.S. tax from payments made to foreign persons or entities. Foreign entities submit W-8 forms to their withholding agent to establish their tax status and claim any applicable exemptions.

- FATCA (Foreign Account Tax Compliance Act)

- A U.S. law requiring foreign financial institutions and certain other foreign entities to report information about accounts and payments held by U.S. persons to the IRS. On W-8 forms, this is referred to as 'Chapter 4' status, and entities must identify their FATCA classification to avoid a 30% withholding penalty.

- Chapter 3 Status

- A classification under Chapter 3 of the U.S. Internal Revenue Code that governs withholding on payments made to foreign persons (also called NRA withholding). Entities must declare their Chapter 3 entity type on W-8 forms so the withholding agent knows the correct withholding rate to apply.

- Beneficial Owner

- The foreign entity or individual that is the true owner of the income being paid, as opposed to an intermediary passing the payment along to someone else. Form W-8BEN-E is specifically used by entities claiming beneficial owner status on U.S.-sourced income.

- Qualified Intermediary (QI)

- A foreign financial institution that has entered into a formal agreement with the IRS to assume certain withholding and reporting responsibilities on behalf of its account holders. QI status is one of the key classifications declared on Form W-8IMY.

- Flow-Through Entity

- An entity—such as a foreign partnership, simple trust, or grantor trust—whose income 'flows through' to its owners or beneficiaries rather than being taxed at the entity level. Flow-through entities use Form W-8IMY to pass withholding responsibilities and documentation to the underlying payees.

- Withholding Statement

- A document attached to Form W-8IMY that allocates payments among the underlying beneficial owners or payees and specifies the withholding rate or exemption applicable to each. Withholding agents use this statement to determine how to withhold on the portions of income flowing to different recipients.

- Tax Treaty

- A bilateral agreement between the U.S. and another country that may reduce or eliminate U.S. withholding tax rates on certain types of income paid to residents of that country. Foreign entities claim treaty benefits on W-8 forms by identifying the applicable treaty country and the specific article that provides the reduced rate.

- NRA Withholding (Nonresident Alien Withholding)

- The standard U.S. requirement to withhold 30% of certain U.S.-sourced income paid to foreign persons or entities who have not established an exemption or reduced rate. Properly completed W-8 forms are the primary mechanism for foreign entities to reduce or avoid this default withholding rate.

- Global Intermediary Identification Number (GIIN)

- A unique identification number assigned by the IRS to foreign financial institutions and other entities that have registered under FATCA. Entities that have a GIIN enter it on their W-8 forms to confirm their FATCA-compliant status to withholding agents.