Fill out commercial insurance forms

with AI.

Commercial insurance forms serve as the essential communication link between businesses, brokers, and underwriters. These documents are designed to capture a comprehensive snapshot of a company’s risk profile, covering everything from basic entity information to complex operational details. Whether it is a foundational application like the ACORD 125 or a specialized habitational risks supplement, these forms provide the standardized data necessary for insurance carriers to accurately assess liability, calculate premiums, and issue policies that protect a business’s assets.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About commercial insurance forms

Insurance agents, risk managers, and business owners typically encounter these forms during the initial application process, annual renewals, or when expanding operations into new territories. Accuracy during this stage is critical; even minor errors in property descriptions or loss history can lead to delayed quotes or insufficient coverage. For professionals managing high volumes of paperwork, such as transportation supplements or formal records of advice, the administrative burden of manual data entry can be significant.

Tools like Instafill.ai use AI to fill these commercial insurance forms in under 30 seconds, handling complex data accurately and securely to streamline the underwriting process. By automating the repetitive aspects of form completion, insurance professionals can focus more on risk analysis and client service rather than manual data entry.

Forms in This Category

The forms in this category have a median Form Complexity Index of 65/100 (Complex), measured across 24 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Selecting the correct commercial insurance form is critical for accurate underwriting and ensuring your business is properly protected. Depending on your industry and the specific stage of the application process, you will need to choose between general applications, specialized supplements, or compliance records.

The Standard Starting Point

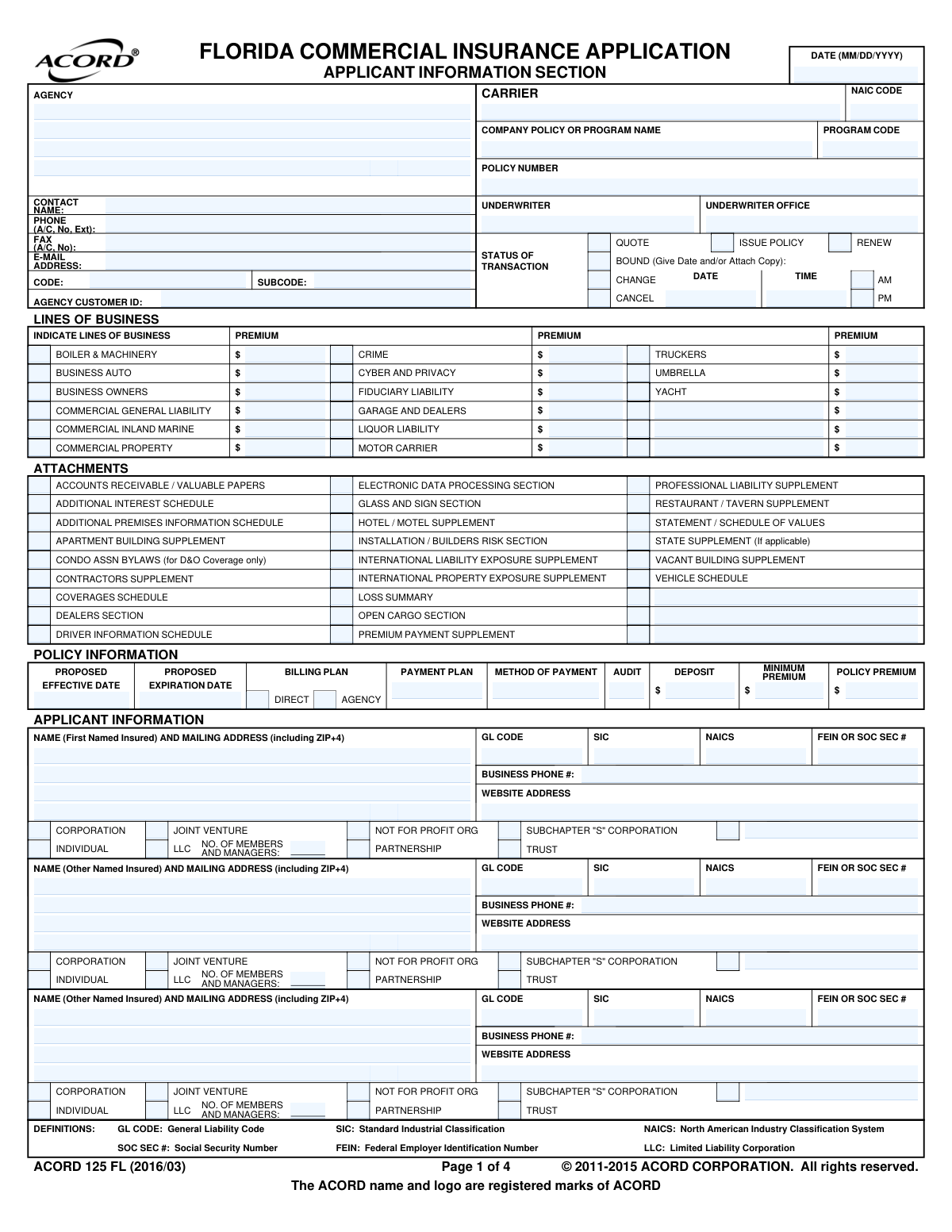

For most businesses seeking general liability, commercial property, or business auto coverage, the ACORD 125, Commercial Insurance Application is the industry standard. It is used to gather foundational data such as business structure, operations, and loss history. If you are only focused on the initial entity details and premises data, the ACORD 125, Commercial Insurance Application, Applicant Information Section may be sufficient for your internal records or preliminary quotes.

Industry-Specific Requirements

Standard applications often require additional sections or supplements to address the unique risks of specific sectors:

- Transportation and Logistics: If your business involves motor truck cargo or freight, use the ACORD 125, Commercial Insurance Application and ACORD 143, Transportation Section. This combined set provides the specific underwriting details needed for transit-related risks.

- Real Estate and Property Management: For those insuring apartment buildings, student housing, or shelters, the Habitational Risks Supplement Application Form is required. This form captures specialized data on occupancy, construction safety, and liability risks that the standard ACORD 125 does not cover in detail.

Compliance and Advisory Records

If you are an insurance advisor or broker, your needs go beyond the application itself. The Record of Advice and Needs Analysis (Non-Life Insurance — Personal and Commercial Lines) is essential for documenting the consultation process. This form ensures compliance with regulatory standards (such as the FAIS Act) by recording the customer’s needs, the coverages discussed, and the final recommendations made by the advisor.

Form Comparison

| Form | Primary Purpose | Target Risk/Focus | Key Information Collected |

|---|---|---|---|

| ACORD 125, Commercial Insurance Application | Standardized application for assessing general commercial insurance risks. | General business operations and standard commercial entities. | Loss history, premises details, and prior insurance coverage. |

| ACORD 125, Commercial Insurance Application and ACORD 143, Transportation Section | Combined application for general commercial and specialized transportation coverage. | Transportation and motor truck cargo businesses. | Cargo types, routes, and specialized logistics underwriting data. |

| ACORD 125, Commercial Insurance Application, Applicant Information Section | Specific section focused on the identity and structure of the applicant. | Applicant identification and basic business setup. | Legal entity name, address, and contact information. |

| Habitational Risks Supplement Application Form | Supplemental questionnaire for assessing multi-unit residential property risks. | Apartment buildings, student housing, and residential shelters. | Construction safety features, occupancy levels, and property liability. |

| Record of Advice and Needs Analysis (Non-Life Insurance — Personal and Commercial Lines) | Mandatory record of advice provided to insurance customers for compliance. | Regulatory compliance and customer needs analysis. | Coverage recommendations, discussed options, and client declarations. |

Tips for commercial insurance forms

When submitting a package that includes the ACORD 125 and supplements like the ACORD 143, verify that the legal business name and EIN are identical on every page. Discrepancies in basic entity information can trigger flags in underwriting systems and cause significant delays in receiving a quote.

Most commercial underwriters require a comprehensive record of claims from the last five years to assess risk accurately. Having your loss runs and claim details ready before you start filling out the application prevents you from having to pause the process to gather data from previous insurers.

AI-powered tools like Instafill.ai can complete complex commercial insurance forms in under 30 seconds with high accuracy. The data stays secure during the process, providing a practical and reliable way to manage high volumes of paperwork without manual data entry.

General forms like the ACORD 125 often require additional documents, such as the Habitational Risks Supplement for property owners or transportation sections for logistics firms. Reviewing the requirements for your specific industry early ensures you don't submit an incomplete application package to your broker.

Avoid using vague language when describing your business activities on underwriting forms. Providing a clear, specific summary of your daily operations helps underwriters categorize your risk profile correctly, which can lead to more accurate policy pricing and coverage terms.

For compliance-heavy documents like the Record of Advice and Needs Analysis, always keep a permanent digital copy for your records. This documentation serves as a vital reference point during policy renewals or audits to justify why specific coverage limits and recommendations were originally chosen.

When filling out property-related supplements, be extremely detailed about safety features such as fire suppression systems, security cameras, and recent building updates. These specific details are primary factors in risk assessment and can directly influence the premium rates offered by the insurer.

Frequently Asked Questions

These forms are standardized documents used by businesses to apply for various types of coverage, such as general liability, property, or transportation insurance. They allow underwriters to gather essential data about a company's operations, risks, and history to determine policy eligibility and pricing.

The ACORD 125, or Commercial Insurance Application, serves as the foundational document for many commercial lines of insurance. It collects general applicant information that remains consistent across different types of coverage, making it a universal starting point for brokers and insurers.

You should include the ACORD 143 when your business involves motor truck cargo or specific transportation risks. It acts as a specialized supplement to the standard ACORD 125, providing deeper insights into fleet operations and cargo details that a general application does not cover.

Typically, the business owner or a designated risk manager completes these forms, often with the assistance of an insurance agent or broker. The agent ensures that the data provided meets the specific requirements of the insurance carriers they are approaching for quotes.

This supplement is required for businesses that manage residential-style risks, such as apartment complexes, student housing, or shelters. It asks detailed questions about building construction, safety systems, and occupancy to help underwriters assess the unique liabilities of housing multiple residents.

This form documents the consultation process between an insurance advisor and a client, ensuring that the recommended coverage aligns with the client’s actual needs. It serves as a compliance record, particularly in regulated markets like South Africa, to prove that the advice given was professional and transparent.

Yes, AI tools like Instafill.ai can fill these forms in under 30 seconds by accurately extracting and placing data from your source documents. This technology eliminates the need for manual typing while ensuring that complex underwriting forms are completed with high precision.

Using AI-powered automation, even multi-page commercial insurance forms can be completed in less than 30 seconds. The system identifies the required fields and maps your business information directly into the PDF, significantly speeding up the application process.

Completed forms are generally submitted to your insurance broker or directly to the underwriting department of the insurance carrier. In many cases, these forms are part of a larger submission package used to solicit quotes from multiple insurance companies simultaneously.

You should have your business's legal entity information, prior insurance policy details, and a record of any losses or claims from the last three to five years. Having these documents ready allows AI tools to more effectively pull the necessary data into the application forms.

While the ACORD 125 covers general applicant information, most insurers require specific sections or supplements for different lines of business, such as property or workers' compensation. Using a modular approach ensures that the underwriter has all the specific data needed for each unique risk.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 65/100 (Complex). See exactly how it is calculated.

- ACORD

- A non-profit organization that provides the standardized forms used by the vast majority of the insurance industry to ensure consistency in data collection and processing.

- Underwriting

- The process an insurance company uses to evaluate the risk of a potential client to determine if they should be insured and at what premium rate.

- Loss History

- A detailed record of previous insurance claims filed by a business, typically covering the last three to five years, used to assess future risk.

- General Liability

- A standard insurance coverage that protects businesses from financial loss resulting from claims of bodily injury, property damage, or personal injury to third parties.

- Habitational Risks

- An insurance classification for multi-unit residential properties like apartment buildings, condominiums, or student housing that have specific safety and liability requirements.

- Motor Truck Cargo

- Specialized insurance that covers the legal liability of a carrier for damage or loss to the freight they are transporting for others.

- Needs Analysis

- A formal evaluation of a business's operations to identify specific financial risks and determine the types and amounts of insurance coverage required.

- FAIS Act

- The Financial Advisory and Intermediary Services Act, a regulation requiring insurance advisors to provide professional advice and maintain a formal record of recommendations for their clients.