Fill out retirement transfer forms

with AI.

Retirement transfer forms are the administrative backbone of moving wealth between financial institutions or different account types without triggering unintended tax consequences. These documents are essential for maintaining the tax-deferred status of your savings when consolidating multiple 401(k) plans or shifting assets between providers like Vanguard and TIAA. By properly documenting these movements, you ensure that the IRS views the transaction as a rollover or direct transfer rather than a taxable distribution, protecting your long-term financial health.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About retirement transfer forms

Individuals typically encounter these forms during major life transitions, such as starting a new job, retiring, or restructuring an investment portfolio to reduce management fees. For instance, you might use an Asset Transfer Authorization to move funds into an employer-sponsored plan or a 1035 Exchange to shift annuity balances between companies. These forms are also vital for estate planning, specifically for designating beneficiaries on non-retirement accounts to ensure a seamless transfer of assets that bypasses the lengthy probate process.

Accuracy is paramount when dealing with retirement assets, as small errors in account numbers or liquidation instructions can lead to significant delays or financial penalties. Tools like Instafill.ai use AI to fill these retirement transfer forms in under 30 seconds, handling sensitive data accurately and securely to streamline the administrative side of your financial planning. This modern approach eliminates the frustration of manual entry while ensuring your transfer request is processed correctly the first time.

Forms in This Category

The forms in this category have a median Form Complexity Index of 43/100 (Basic), measured across 8 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Navigating retirement transfers can be complex, as the correct form depends on whether you are moving funds between institutions, consolidating accounts within the same provider, or managing non-retirement assets. Use the categories below to identify the document that fits your specific financial goal.

Consolidating Funds into a New Retirement Plan

If you are moving assets from an old 401(k), 403(b), or IRA into a new employer-sponsored or managed account, select the form based on the receiving institution:

- TIAA Plans: Use the Easy Transfer Form: Moving Funds to an Employer-Sponsored Retirement Plan at TIAA to consolidate external funds into your TIAA account.

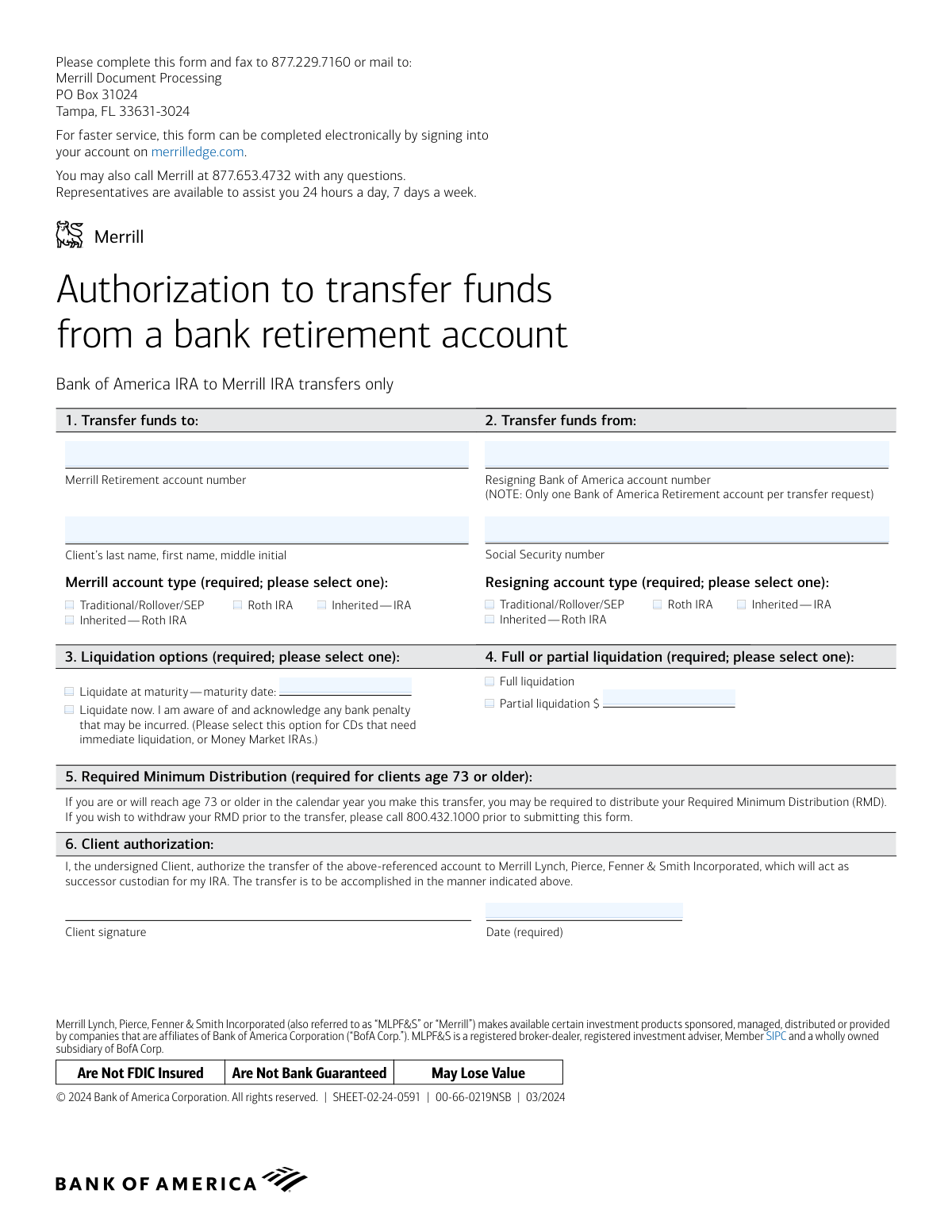

- Merrill Lynch: If you are moving funds specifically from a Bank of America IRA to a Merrill IRA, use the Authorization to transfer funds from a bank retirement account.

- Specific Employer Plans: For specialized plans, use the Housing Agency Retirement Trust Transfer/Rollover Form or the Vanguard Asset Transfer Authorization Form for the Emory University Retirement Plan if you are a participant in those specific programs.

Moving Funds Between Existing Accounts or Annuities

If you already hold accounts with a provider and need to shift balances internally or perform a tax-advantaged exchange, look at these options:

- Internal Vanguard Moves: Choose the Retirement Transfer Between Existing Vanguard Accounts for distributions or rollovers between two Vanguard accounts you already own.

- Annuity Exchanges: To move TIAA Traditional account balances to a different investment company while avoiding immediate tax liabilities, use the TIAA 1035 Exchange Authorization to Alternate Investment Company Transfer Payout Annuity for ATRA.

Non-Retirement Transfers and Gifting

Some forms in this category apply to standard brokerage accounts rather than tax-advantaged retirement plans:

- Estate Planning: Use the Beneficiaries — Nonretirement Transfer on Death form to ensure individual or joint brokerage assets bypass probate and go directly to your heirs.

- Gifting Assets: If you want to move stocks or mutual funds to another person or entity at a different firm, use the Transfer Shares as a Gift — Nonretirement form.

Form Comparison

| Form | Purpose | Source & Destination | Account Type |

|---|---|---|---|

| Authorization to transfer funds from a bank retirement account | Consolidates Bank of America retirement assets into a Merrill IRA. | Bank of America to Merrill Lynch | Bank-held IRA |

| Beneficiaries — Nonretirement Transfer on Death | Assigns beneficiaries for nonretirement assets to ensure transfer without probate. | Fidelity (Internal Update) | Nonretirement (Individual/Joint) |

| Easy Transfer Form: Moving Funds to an Employer-Sponsored Retirement Plan at TIAA | Transfers retirement funds from external institutions into TIAA employer plans. | External Institution to TIAA | Employer-Sponsored (403b) |

| Housing Agency Retirement Trust Transfer/Rollover Form | Facilitates consolidating external retirement funds into a Housing Agency Trust. | External Plans to HART | 457b, 403b, 401k, or IRA |

| Retirement Transfer Between Existing Vanguard Accounts | Moves retirement assets between two accounts already held at Vanguard. | Vanguard to Vanguard (Internal) | Retirement (IRA/Rollover) |

| TIAA 1035 Exchange Authorization to Alternate Investment Company Transfer Payout Annuity for ATRA | Executes a tax-free 1035 exchange of annuity balances to another company. | TIAA to Alternate Company | After-Tax Retirement Annuity |

| Transfer Shares as a Gift — Nonretirement | Authorizes gifting securities from a Fidelity account to another financial firm. | Fidelity to External Firm | Nonretirement Brokerage |

| Vanguard Asset Transfer Authorization Form for the Emory University Retirement Plan | Transfers 403(b) assets from external providers to Vanguard's Emory plan. | External Provider to Vanguard | Emory University 403(b) |

Tips for retirement transfer forms

One of the most common reasons for transfer delays is a typo in the account or routing number. Double-check these digits against your latest statement to ensure the funds reach the correct destination without being rejected by the receiving institution.

When moving retirement funds, request a trustee-to-trustee or direct transfer whenever possible. This prevents the originating institution from withholding mandatory taxes, keeping your full balance intact and avoiding potential early withdrawal penalties.

Many retirement transfers involving high dollar amounts or specific institutions require a Medallion Signature Guarantee rather than a standard notary. Confirm if your form requires this specialized stamp from a bank or brokerage before submitting to avoid processing delays.

AI-powered tools like Instafill.ai can complete these complex forms in under 30 seconds with high accuracy, ensuring all technical fields are mapped correctly. Your data stays secure during the process, making it a reliable time-saver when managing multiple account consolidations.

Transferring assets to a new plan or institution often resets your beneficiary designations. Once the transfer is complete, always verify that your Transfer on Death or beneficiary instructions have been updated on the new platform to ensure your legacy plans remain active.

Decide whether you want to sell your assets or move them as-is before filling out the form. Choosing an in-kind transfer can help you avoid market timing risks, but you must ensure the receiving institution supports the specific mutual funds or securities you currently hold.

Save a copy of every signed transfer authorization and the confirmation of receipt from the financial institution. Retirement transfers can take several weeks, and having your documentation organized makes it easier to follow up if the funds do not appear in a timely manner.

Frequently Asked Questions

These forms are used to move assets between different financial institutions or account types without incurring taxes or penalties. They are essential for consolidating multiple 401(k) or IRA accounts into a single plan for easier management and lower administrative fees.

The correct form is usually determined by the receiving institution where you want the money to go. For instance, if you are moving funds into a TIAA plan, you would use the Easy Transfer Form, while moving assets into a Vanguard account for the Emory University Retirement Plan requires their specific authorization document.

A direct transfer moves funds directly from one financial institution to another, which is generally tax-free and simpler to report. A rollover may involve the funds being sent to you personally first, which requires you to deposit them into a new eligible plan within 60 days to avoid taxes and potential penalties.

Yes, you can use AI tools like Instafill.ai to complete these forms in under 30 seconds. The AI accurately extracts data from your source documents, such as bank statements or existing account records, and places it into the correct fields on the PDF.

A 1035 Exchange is a provision in the tax code that allows for a tax-free transfer of an existing annuity or life insurance contract for a new one. It is commonly used when moving funds from a TIAA Traditional account to an alternate investment company while maintaining tax-deferred status.

Many financial institutions require a Medallion Signature Guarantee for large transfers to verify the identity of the person authorizing the transaction. You should check the specific requirements of the firm you are transferring assets from, as a standard notary public signature is often not accepted for securities transfers.

While manually entering account numbers and institution addresses can take 15 to 20 minutes, AI-powered services can fill these forms accurately in under 30 seconds. These tools can also convert static, non-fillable PDF versions into interactive forms that are easier to sign and submit.

You will typically need your current account numbers, the name and address of the delivering institution, and details regarding which assets you wish to liquidate or move in-kind. Having your most recent account statement available is recommended to ensure the data matches the records of both institutions.

Yes, specific forms like the 'Transfer Shares as a Gift' document allow you to move non-retirement assets such as stocks or mutual funds to another person. This process is often used for charitable giving or transferring wealth to family members without selling the assets first.

In most cases, you submit the completed form to the 'successor' or receiving institution. They will then contact your current financial provider to initiate the movement of funds on your behalf, though some institutions may require you to provide a copy to both parties.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 43/100 (Basic). See exactly how it is calculated.

- Direct Rollover

- The movement of retirement funds directly from one qualified plan to another, such as from a 401(k) to an IRA. This process ensures the money is not taxed as income and avoids early withdrawal penalties.

- Trustee-to-Trustee Transfer

- A transaction where retirement assets are sent directly from one financial institution to another. Because the account holder never receives the money, there is no mandatory tax withholding.

- 1035 Exchange

- A provision in the tax code that allows for the tax-free exchange of an existing annuity or life insurance contract for a new one. It is commonly used to move funds between insurance companies without creating a taxable event.

- Transfer on Death (TOD)

- A legal designation for non-retirement accounts that names specific beneficiaries to inherit the assets upon the owner's death. This allows the account to bypass the probate process and go directly to the heirs.

- ACATS (Automated Customer Account Transfer Service)

- A regulated system used by brokerage firms to transfer securities like stocks and mutual funds from one firm to another. It is the industry standard for moving assets between investment accounts.

- Medallion Signature Guarantee

- A certification provided by a financial institution that authenticates a signature on a document. It is often required for transferring high-value securities to prevent unauthorized or fraudulent transfers.

- Liquidation

- The act of selling assets within an account to turn them into cash. Many retirement transfers require you to sell your current investments so the cash value can be moved to a new provider.

- 403(b) Plan

- A retirement plan designed for employees of public schools, certain non-profits, and religious organizations. These plans are frequently the source or destination of funds in retirement transfer forms.