Fill out Freddie Mac forms

with AI.

Freddie Mac forms are standardized documents used throughout the residential mortgage process — from the initial loan application to the final packaging of loans for the secondary market. These forms are developed in coordination with Fannie Mae and are required by lenders, underwriters, and servicers to ensure consistency, regulatory compliance, and accurate risk assessment across the mortgage industry. Because they follow uniform guidelines, they are accepted by lenders nationwide and play a central role in how conforming mortgage loans are originated and sold.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About Freddie Mac forms

Anyone applying for a residential mortgage will likely encounter at least one of these forms. Homebuyers, refinancing homeowners, and real estate investors typically start with the Uniform Residential Loan Application (Form 65 / Form 1003), which captures everything from income and employment history to assets and liabilities. Mortgage professionals — including loan officers, processors, and underwriters — rely on forms like the Uniform Underwriting and Transmittal Summary (Form 1077 / Form 1008) to consolidate and deliver loan data when selling conforming loans to the secondary market.

These forms can be dense and detail-heavy, but tools like Instafill.ai use AI to fill them out accurately in under 30 seconds, making the process significantly faster for both borrowers and mortgage professionals handling high volumes of paperwork.

Forms in This Category

The forms in this category have a median Form Complexity Index of 82/100 (Very Complex), measured across 7 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

| Form Name | Pages | FCI | |

|---|---|---|---|

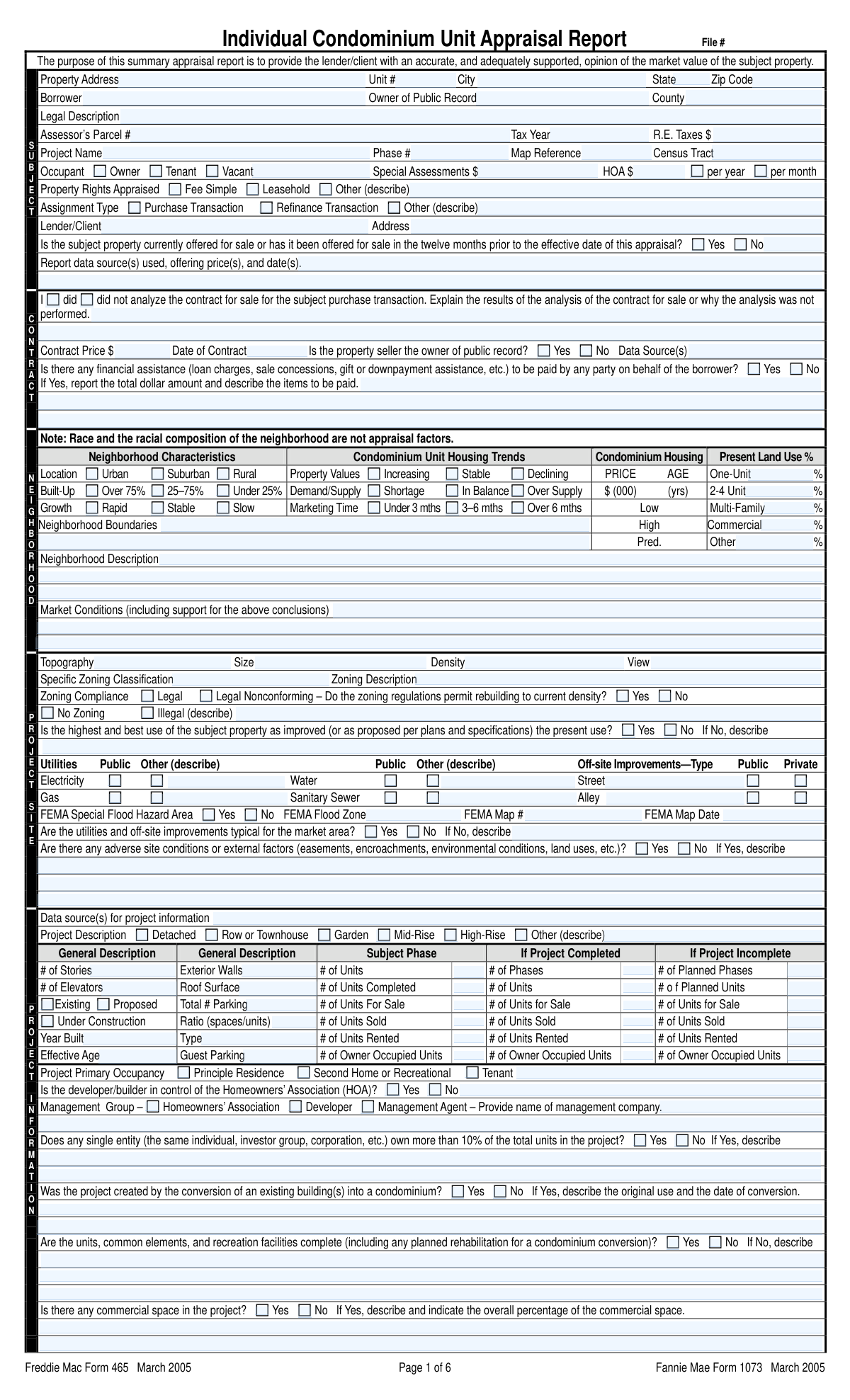

| 1. | Fannie Mae Form 1073 / Freddie Mac Form 465, Individual Condominium Unit Appraisal Report | 7 | Very Complex 86 |

| 2. | Uniform Residential Appraisal Report (Fannie Mae Form 1004 / Freddie Mac Form 70) | 6 | Very Complex 82 |

| 3. | Uniform Residential Loan Application (Fannie Mae Form 1003 / Freddie Mac Form 65) | 3 | Moderate 46 |

| 4. | Uniform Residential Loan Application, Fannie Mae Form 1003 / Freddie Mac Form 65 | 9 | Very Complex 97 |

| 5. | Uniform Residential Loan Application (Freddie Mac Form 65 / Fannie Mae Form 1003) | 9 | Very Complex 92 |

| 6. | Uniform Residential Loan Application (Freddie Mac Form 65 / Fannie Mae Form 1003) | 1 | Complex 64 |

| 7. | Uniform Underwriting and Transmittal Summary (Fannie Mae Form 1008 / Freddie Mac Form 1077) | 1 | Complex 68 |

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

With only two forms in this category, choosing the right one comes down to who you are in the mortgage process and what stage you're at.

If You're a Borrower Applying for a Home Loan

Start with the Uniform Residential Loan Application (Freddie Mac Form 65 / Fannie Mae Form 1003). This is the form you fill out when you're seeking a mortgage — it captures everything a lender needs to evaluate your application:

- Personal identity and contact information

- Employment history and income details

- Assets, debts, and existing real estate

- Loan amount, property address, and loan purpose

- Required declarations and demographic disclosures

This is almost always the first form in any residential mortgage transaction and is required by virtually every lender offering conforming loans.

If You're a Lender or Mortgage Professional Delivering Loans to the Secondary Market

You'll need the Uniform Underwriting and Transmittal Summary (Fannie Mae Form 1008 / Freddie Mac Form 1077). This form is not filled out by borrowers — it's a lender-side document used when selling or delivering conforming loans to Fannie Mae or Freddie Mac. Use it when you need to:

- Summarize underwriting findings and qualifying ratios

- Document loan terms, property details, and risk assessment results

- Package the loan file for secondary market delivery

Think of Form 1008/1077 as the cover sheet that accompanies the completed loan file, while Form 1003/65 is the foundation document the borrower submits.

Quick Decision Summary

| Situation | Use This Form |

|---|---|

| Applying for a mortgage as a borrower | Form 65 / Form 1003 |

| Delivering a loan to Fannie Mae or Freddie Mac | Form 1077 / Form 1008 |

Both forms can be completed quickly and accurately using Instafill.ai's AI-powered tools.

Form Comparison

| Form | Purpose | Who Files It | When to Use |

|---|---|---|---|

| Uniform Residential Loan Application (Freddie Mac Form 65 / Fannie Mae Form 1003) | Apply for a residential mortgage loan | Borrower, with lender assistance | At the start of the mortgage application process |

| Uniform Underwriting and Transmittal Summary (Fannie Mae Form 1008 / Freddie Mac Form 1077) | Summarize underwriting data for secondary market delivery | Lender or underwriter submitting loan to agency | When selling or delivering conforming loans to Fannie Mae or Freddie Mac |

Tips for Freddie Mac forms

Before filling out the Uniform Residential Loan Application (Form 65/1003), collect your W-2s, recent pay stubs, bank statements, and tax returns. Having these on hand prevents mid-form interruptions and ensures the income, asset, and debt figures you enter are accurate and consistent across all documents.

The loan application (Form 65/1003) and the Underwriting and Transmittal Summary (Form 1008/1077) must reflect identical borrower information, loan terms, and qualifying ratios. Discrepancies between the two forms are a common red flag during underwriting review and can delay or derail loan approval.

Lenders and agencies require complete information on both Freddie Mac forms — leaving fields blank or entering 'N/A' incorrectly can trigger compliance issues or return the package for correction. If a section genuinely does not apply, confirm with your lender how it should be handled before submitting.

The qualifying ratios on Form 1008/1077 must align precisely with the income and liability data entered on the loan application. A miscalculated DTI ratio is one of the most common underwriting errors — verify your monthly debt and income figures carefully before finalizing either form.

AI-powered tools like Instafill.ai can auto-complete Freddie Mac mortgage forms with high accuracy, saving significant time when you're managing multiple loan files. Your data stays secure throughout the process, and Instafill.ai can even convert non-fillable PDF versions of these forms into interactive, editable documents.

The subject property address, appraised value, loan amount, and loan purpose must be entered exactly the same way on every form in the loan package. Even minor inconsistencies — like an abbreviated street name — can cause delays when the file is reviewed for secondary market delivery.

The declarations and acknowledgments section of the URLA (Form 1003/65) carries legal weight — the borrower is certifying the accuracy of all submitted information. Read each question thoroughly and answer honestly, as misrepresentation on a mortgage application can have serious legal consequences.

Always save a copy of your completed Freddie Mac forms with the submission date noted, especially when delivering loan packages to the secondary market. Having a clear record protects all parties if questions arise during post-closing audits or investor reviews.

Frequently Asked Questions

Freddie Mac forms are standardized mortgage industry documents used by lenders, borrowers, and real estate professionals to apply for and process conforming residential loans. They are required when originating or selling mortgages that meet Freddie Mac (and often Fannie Mae) guidelines. Borrowers use them during the loan application process, while lenders rely on them to document underwriting decisions and deliver loans to the secondary market.

Many Freddie Mac and Fannie Mae forms are actually the same standardized documents shared across both agencies — they simply carry dual designations (e.g., Freddie Mac Form 65 is the same as Fannie Mae Form 1003). Both agencies work together to maintain uniform standards for the conventional mortgage market, so lenders typically satisfy both agencies' requirements with a single form submission.

If you are a borrower applying for a residential mortgage, you will need the Uniform Residential Loan Application (Freddie Mac Form 65 / Fannie Mae Form 1003). This is the industry-standard application that collects your personal, financial, and property information so lenders can evaluate your creditworthiness and process your loan.

The Uniform Underwriting and Transmittal Summary (Freddie Mac Form 1077 / Fannie Mae Form 1008) is a lender-facing document that consolidates key loan data — including income, property details, loan terms, and risk findings — into a single package for secondary market delivery. It is required when lenders sell or deliver conforming loans to Freddie Mac or Fannie Mae, serving as a cover sheet that summarizes the underwriting analysis for investors and agencies.

No — the Uniform Underwriting and Transmittal Summary (Form 1077/1008) is completed by the lender or underwriter, not the borrower. It is an internal and secondary-market document that accompanies the loan file when the lender delivers the mortgage to Freddie Mac or Fannie Mae. Borrowers are responsible for completing the Uniform Residential Loan Application (Form 65/1003).

Before completing the Uniform Residential Loan Application, you should gather documents such as government-issued ID, recent pay stubs and W-2s, tax returns, bank and investment account statements, information on existing debts and liabilities, and details about the property you intend to purchase or refinance. Having this information on hand ensures you can provide complete and accurate responses, which is critical since you certify the accuracy of your statements on the form.

Freddie Mac forms are submitted to your mortgage lender or loan officer — not directly to Freddie Mac. The lender collects and reviews your completed application and supporting documents, then uses forms like the Transmittal Summary when delivering the finalized loan to the secondary market. Your lender will guide you on their specific submission process and required documentation.

Yes — AI-powered tools like Instafill.ai can fill out Freddie Mac forms such as the Uniform Residential Loan Application and the Transmittal Summary in under 30 seconds by accurately extracting and placing data from your source documents. These tools can also convert non-fillable PDF versions into interactive fillable forms, making the process faster and reducing the risk of errors.

Manually completing a form like the Uniform Residential Loan Application can take anywhere from 30 minutes to several hours depending on how prepared you are with your financial documents. However, AI-powered services like Instafill.ai can pre-populate these forms in under 30 seconds by pulling data directly from uploaded source documents, significantly reducing the time and effort involved.

Yes — the core Freddie Mac forms, such as the Uniform Residential Loan Application and the Transmittal Summary, are standardized documents used consistently across the mortgage industry. Individual lenders may have their own supplemental forms or checklists, but the Freddie Mac/Fannie Mae forms themselves follow a uniform format to ensure consistency for secondary market compliance.

Errors or omissions on mortgage forms like the Uniform Residential Loan Application can delay loan processing, trigger additional verification requests, or in serious cases raise compliance concerns since borrowers certify the accuracy of the information provided. It is important to review all entries carefully before submission and work with your lender to correct any mistakes promptly.

The Uniform Residential Loan Application (Form 65/1003) is the standard form for most conventional, FHA, VA, and USDA residential mortgage applications, making it nearly universal in the home lending process. The Transmittal Summary (Form 1077/1008) is specifically required for conforming loans delivered to Freddie Mac or Fannie Mae and may not apply to all loan types or portfolio lenders.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 82/100 (Very Complex). See exactly how it is calculated.

- URLA (Uniform Residential Loan Application)

- The industry-standard form used by borrowers to apply for a residential mortgage, collecting personal, financial, and property information that lenders use to evaluate creditworthiness. It is jointly designated as Freddie Mac Form 65 and Fannie Mae Form 1003.

- Freddie Mac

- The Federal Home Loan Mortgage Corporation, a government-sponsored enterprise (GSE) that purchases mortgages from lenders, packages them into securities, and sells them to investors, thereby providing lenders with funds to issue new home loans.

- Fannie Mae

- The Federal National Mortgage Association, another GSE that, like Freddie Mac, buys conforming mortgages from lenders and sells them on the secondary market, helping to keep mortgage funds available and affordable.

- Secondary Market

- The marketplace where lenders sell existing mortgage loans to investors such as Freddie Mac and Fannie Mae, allowing lenders to replenish their capital and issue new loans to borrowers.

- Conforming Loan

- A mortgage that meets the guidelines set by Freddie Mac and Fannie Mae, including loan limits, credit standards, and documentation requirements, making it eligible for purchase by these agencies.

- Debt-to-Income Ratio (DTI)

- A calculation that compares a borrower's total monthly debt payments to their gross monthly income, expressed as a percentage; lenders use it to assess whether a borrower can afford the mortgage payments.

- Underwriting

- The process by which a lender evaluates a borrower's financial profile—including income, credit history, assets, and the property's value—to determine the risk of approving a mortgage loan.

- Transmittal Summary (Form 1008 / Form 1077)

- A standardized cover sheet required by Freddie Mac and Fannie Mae when delivering a loan for purchase, summarizing key underwriting data, loan terms, and risk findings in a single document accompanying the loan file.

- Qualifying Income

- The portion of a borrower's income that a lender can count toward mortgage eligibility after applying agency guidelines, which may exclude irregular, temporary, or unverifiable income sources.

- HMDA / Demographic Monitoring

- The Home Mortgage Disclosure Act requires lenders to collect and report demographic data (such as race, ethnicity, and sex) from applicants to help regulators detect and prevent discriminatory lending practices.