Fill out investment withdrawal forms

with AI.

Investment withdrawal forms are essential documents used to request the distribution of assets from various investment vehicles, such as retirement accounts, college savings plans, and annuities. These forms are critical because they dictate how much money is being removed, the reason for the distribution, and how taxes should be withheld. Whether you are managing a 403(b) distribution or requesting a one-time withdrawal from a 529 College Savings Plan, accuracy is paramount to ensure compliance with IRS regulations and to avoid unexpected tax penalties or processing delays.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About investment withdrawal forms

Typically, these forms are needed by individuals reaching retirement age who must satisfy Required Minimum Distributions (RMDs), beneficiaries managing an Inherited IRA, or account holders who need to cover qualified education expenses. They are also used for one-time events, such as rolling over funds to a different retirement account or surrendering an annuity contract. Because these documents often require detailed financial information and specific tax elections, they can be time-consuming and prone to manual errors. Tools like Instafill.ai use AI to fill these forms in under 30 seconds, handling data accurately and securely to streamline the process.

Forms in This Category

The forms in this category have a median Form Complexity Index of 52/100 (Moderate), measured across 12 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

| Form Name | Pages | FCI | |

|---|---|---|---|

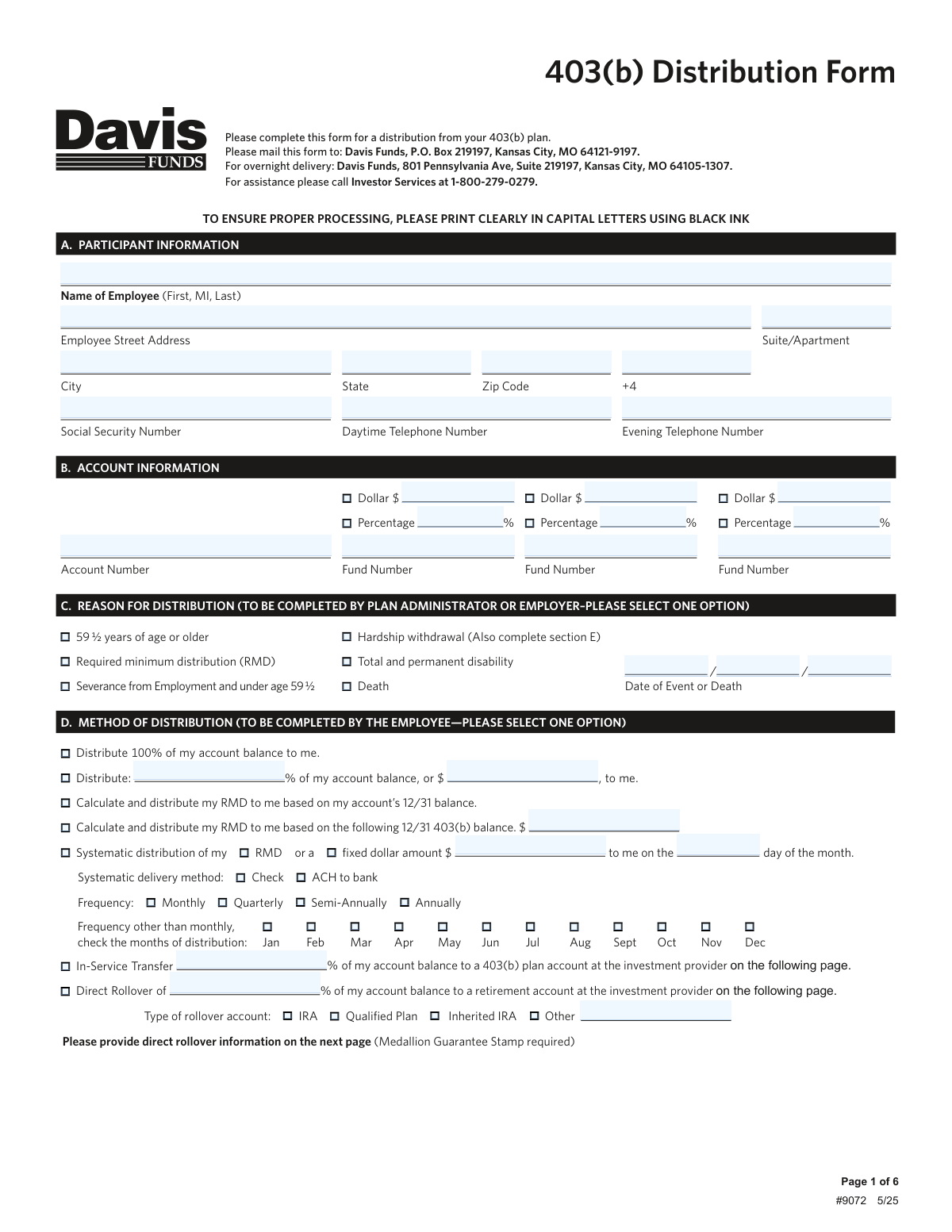

| 1. | 403(b) Distribution Form - Davis Funds | 1 | Moderate 52 |

| 2. | Automatic Withdrawals — Inherited IRA - Fidelity Investments | 1 | Moderate 55 |

| 3. | Fidelity Investments Earnings Automatic Withdrawal Plan — IRA | 1 | Basic 40 |

| 4. | Fidelity Investments Withdrawal — One-Time | 1 | Basic 41 |

| 5. | Fidelity Investments Withdrawals—529 College Savings Plan | 1 | Moderate 46 |

| 6. | Form F11323, Cash Withdrawal From Your Retirement Investments | 1 | – |

| 7. | Form F11610, Cash Withdrawal from your Retirement Investments for Plans Not Subject to QJSA | 1 | – |

| 8. | IRA/ESA Distribution Request Instructions | 1 | Moderate 59 |

| 9. | IRA Periodic Distribution Request Form | 1 | Moderate 60 |

| 10. | NextGen 529 Client Direct Series Withdrawal Request Form | 1 | Moderate 49 |

| 11. | One-Time Withdrawal – Investment-Only (Non-Prototype) Retirement Account | 1 | Moderate 54 |

| 12. | One-Time Withdrawal – IRA, Fidelity Investments | 1 | Moderate 52 |

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Selecting the correct investment withdrawal form depends primarily on the financial institution holding your assets, the type of account you own, and whether you need a single payment or a recurring income stream.

Retirement Account Withdrawals (IRA & 403b)

If you are managing a standard retirement account, your choice depends on the frequency of the distribution:

- One-Time Requests: For a single payout from a Fidelity account, use the One-Time Withdrawal – IRA, Fidelity Investments. If your account is held through Pershing, select the IRA/ESA Distribution Request.

- Recurring Income: To set up scheduled payments or satisfy RMDs, use the IRA Periodic Distribution Request Form. If you only wish to withdraw the growth from your investments while keeping the principal intact, use the Fidelity Investments Earnings Automatic Withdrawal Plan — IRA.

- Employer-Sponsored Plans: Participants in non-profit or school-based plans should use the 403(b) Distribution Form - Davis Funds.

TIAA and Specialized Retirement Plans

TIAA participants have specific forms based on their plan's legal structure:

- General Cash Payouts: Use Form F11323, Cash Withdrawal From Your Retirement Investments for standard requests.

- Non-QJSA Plans: If your plan is not subject to Qualified Joint and Survivor Annuity requirements, use Form F11610, Cash Withdrawal from your Retirement Investments for Plans Not Subject to QJSA.

- Trustee Requests: For specialized non-prototype accounts, use the One-Time Withdrawal – Investment-Only (Non-Prototype) Retirement Account form.

Education Savings and Beneficiaries

If you are withdrawing funds for college expenses or managing an inherited legacy, look for these specific forms:

- 529 Plans: Choose between the Fidelity Investments Withdrawals—529 College Savings Plan or the NextGen 529 Client Direct Series Withdrawal Request Form depending on your plan provider.

- Inherited Accounts: Beneficiaries managing an inherited IRA should use Automatic Withdrawals — Inherited IRA - Fidelity Investments to schedule their distributions.

- Annuities: For one-time withdrawals or full contract surrenders of an annuity, use the Fidelity Investments Withdrawal — One-Time form.

Tips for investment withdrawal forms

Many withdrawal forms default to a 10% federal tax withholding if you do not specify a preference. Ensure your selection aligns with your actual tax bracket to avoid an unexpected tax bill or a smaller-than-expected net payout.

When selecting a delivery method, choose Electronic Funds Transfer (EFT) over a physical check whenever possible. It significantly reduces the wait time for your funds and eliminates the risk of the check being lost or delayed in the mail.

Before submitting a 529 withdrawal request, confirm that the funds are being used for qualified education expenses. Withdrawing for non-qualified reasons can trigger both income taxes and a 10% penalty on the earnings portion of the distribution.

Investment firms often have distinct forms for Traditional IRAs, Roth IRAs, and Inherited accounts. Using the wrong document can cause your request to be rejected or result in incorrect tax reporting to the IRS, requiring a lengthy correction process.

AI-powered tools like Instafill.ai can complete these complex withdrawal forms in under 30 seconds with high accuracy. Your sensitive financial data stays secure during the process, making it a reliable time-saver for anyone managing multiple investment accounts.

Have your bank's routing number and your specific account number ready before you start filling out the form. Most one-time or periodic distribution requests require this information to establish a secure direct link for the transfer of your assets.

Be careful not to use a periodic distribution form if you only intend to make a single withdrawal. Periodic forms are designed for recurring income, and using the wrong document could trigger unintended monthly or quarterly payments from your balance.

Frequently Asked Questions

Investment withdrawal forms are formal documents used to request the distribution of funds from financial accounts such as IRAs, 403(b) plans, or 529 college savings plans. They allow account holders or beneficiaries to specify the withdrawal amount, the reason for the distribution, and the preferred delivery method for the funds.

You should select a form based on the financial institution managing your assets and the specific type of account you hold. For example, a 403(b) plan requires a different distribution form than a Traditional IRA, and you must also distinguish between one-time requests and recurring automatic withdrawal plans.

These forms are filed whenever you need to access your savings, whether for retirement income, qualified education expenses, or financial hardship. They are also used to satisfy Required Minimum Distributions (RMDs) or to initiate a rollover of assets to another qualified retirement account.

A one-time distribution form is used for a single, immediate withdrawal or to fully surrender a contract. Periodic distribution forms are used to establish a recurring schedule, allowing you to receive regular income or manage automatic withdrawals of earnings over a set period.

Most forms require your personal identification, such as your Social Security number and account number, along with specific payment instructions like bank routing and account details. You will also need to make elections regarding federal and state tax withholding, as these distributions are often reportable to the IRS.

Completed forms are generally submitted to the plan administrator or the financial institution that holds the account, such as Fidelity, TIAA, or Davis Funds. Many institutions allow for digital uploads through their secure customer portals, though some may require submission via mail or fax.

Yes, there are dedicated forms for 529 plans used to request funds for qualified higher education expenses. These forms also facilitate other actions, such as rolling over funds to a different 529 plan or transferring assets to a Roth IRA for the beneficiary.

Yes, you can fill out investment withdrawal forms using AI tools like Instafill.ai. These tools can accurately extract and place data from your source documents into the form fields, helping you avoid manual entry errors and ensuring the document is ready for submission.

Using AI-powered services like Instafill.ai, you can complete these investment forms in under 30 seconds. The AI automates the data entry process, making it much faster than filling out the PDF manually or by hand.

Most withdrawals from retirement accounts are considered taxable income and may be subject to early withdrawal penalties if you are under age 59 ½. It is important to carefully complete the tax withholding section of the form to ensure you are meeting your tax obligations and avoiding potential underpayment penalties.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 52/100 (Moderate). See exactly how it is calculated.

- RMD (Required Minimum Distribution)

- The minimum amount the IRS requires you to withdraw annually from most retirement accounts once you reach a certain age, usually 72 or 73.

- Tax Withholding

- The portion of your withdrawal that a financial institution sends directly to the IRS or state tax authorities as a prepayment of your income taxes.

- Qualified Distribution

- A withdrawal from a tax-advantaged account, such as a Roth IRA or 529 plan, that meets specific IRS requirements to be tax-free and penalty-free.

- Rollover

- The process of moving funds from one retirement or education savings account to another similar account while maintaining its tax-deferred status.

- QJSA (Qualified Joint and Survivor Annuity)

- A retirement plan benefit that provides a lifetime income to the participant and a survivor benefit to a spouse; some forms require a waiver to choose a different payment method.

- Early Withdrawal Penalty

- A 10% additional tax typically charged by the IRS if you take money out of a retirement account before reaching age 59 ½, unless an exception applies.

- Qualified Education Expenses

- Specific costs like tuition, fees, books, and room and board that allow for tax-free withdrawals from a 529 College Savings Plan.

- EFT (Electronic Funds Transfer)

- A digital method of sending your withdrawn funds directly to your bank account rather than receiving a physical check in the mail.