Fill out financial planning forms

with AI.

Financial planning forms are the essential building blocks for securing your financial future and ensuring your assets are managed according to your wishes. This category encompasses a wide range of documents used for retirement management, tax optimization, and wealth transfer. Whether you are adjusting your investment strategy or preparing for the transition of assets to the next generation, these forms provide the legal and administrative framework required by major financial institutions. Accurate completion of these documents is vital, as they often dictate how significant sums of money are handled and can even override instructions left in a traditional will.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About financial planning forms

These documents are typically needed by individual investors, retirees, and estate planners working with institutions like Fidelity, Charles Schwab, or TIAA. Common scenarios include designating beneficiaries for a brokerage account to avoid probate, managing Required Minimum Distributions (RMDs) to remain compliant with IRS regulations, or converting a Traditional IRA to a Roth IRA for better tax positioning. For those managing complex estates or retirement plans, having the correct estate planning forms or Vanguard-specific documents on hand ensures that transitions are seamless and that charitable goals, such as through Qualified Charitable Distributions, are met without unnecessary tax penalties.

Navigating the fine print of these financial documents can be time-consuming and prone to error. Tools like Instafill.ai use AI to fill these forms in under 30 seconds, ensuring your data is handled accurately and securely. This automated approach allows you to focus on your long-term financial goals rather than the repetitive task of manual data entry.

Forms in This Category

The forms in this category have a median Form Complexity Index of 41/100 (Basic), measured across 13 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

| Form Name | Pages | FCI | |

|---|---|---|---|

| 1. | Beneficiary Designation Form - Merrill Lynch | 1 | Moderate 54 |

| 2. | Designated Beneficiary Plan Agreement | 1 | – |

| 3. | Designated Beneficiary Plan Agreement | 1 | – |

| 4. | Distribution — RMD Annual One-Time Payment | 1 | Basic 40 |

| 5. | Form F1387, Designating Beneficiaries for Your TIAA-CREF Accounts | 1 | – |

| 6. | Individual Retirement Account (IRA) — Qualified Charitable Distribution Form | 1 | Basic 41 |

| 7. | Premiere Select Roth IRA Conversion 1.747921.112 | 1 | Basic 39 |

| 8. | Qualified Retirement Plan Designation of Beneficiary | 1 | Moderate 47 |

| 9. | Request for Required Minimum Distribution (RMD) - IRA Owner/Plan Participant | 1 | Basic 36 |

| 10. | TIAA Beneficiary Designation Form | 1 | – |

| 11. | TIAA Beneficiary Designation Form (F11468) | 1 | – |

| 12. | TIAA-CREF Form F1387, Designating Your Beneficiaries | 1 | – |

| 13. | TIAA-CREF Form F1387, Designation of Beneficiary | 1 | – |

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Managing your financial future requires the right paperwork for your specific accounts and life stage. Whether you are securing your legacy or managing retirement income, these forms are categorized by their primary financial function.

Estate and Legacy Planning

To ensure your assets pass directly to your heirs without the delays of probate, you must keep your beneficiary designations current. Most financial institutions require their own specific documents:

- For Brokerage Accounts: Use the Designated Beneficiary Plan Agreement for Charles Schwab accounts or the Beneficiary Designation Form - Merrill Lynch for Merrill accounts.

- For Retirement Annuities: TIAA participants should use Form F1387 (Designating Beneficiaries for Your TIAA-CREF Accounts) or Form F11468 (TIAA Beneficiary Designation Form) to name individuals or trusts as recipients of death benefits.

- For General Employer Plans: Use the Qualified Retirement Plan Designation of Beneficiary for standard 401(k) or 403(b) accounts.

Managing Retirement Distributions

Once you reach the age for Required Minimum Distributions (RMDs), you must document your withdrawals to avoid significant IRS penalties.

- Standard Withdrawals: Use the Distribution — RMD Annual One-Time Payment for Fidelity-administered employer plans or the Request for Required Minimum Distribution (RMD) - IRA Owner/Plan Participant for Fidelity & Guaranty annuity contracts.

- Tax-Efficient Giving: If you are 70½ or older and wish to donate to charity while satisfying your RMD, use the Individual Retirement Account (IRA) — Qualified Charitable Distribution Form. This allows for a direct transfer of funds to an eligible charity without increasing your taxable income.

Strategic Account Changes

If you are looking to change the tax status of your retirement savings, look for conversion documents. The Premiere Select Roth IRA Conversion form is used specifically to move assets from pre-tax accounts (like a Traditional, SEP, or SIMPLE IRA) into a post-tax Roth IRA. This is a crucial step for investors who expect to be in a higher tax bracket in the future.

Form Comparison

| Form | Primary Purpose | Account Type | Key Benefit |

|---|---|---|---|

| Beneficiary Designation Form - Merrill Lynch | Designate primary and contingent heirs for account assets. | Merrill Lynch IRAs, HSAs, and 403(b)s. | Ensures assets are distributed according to your wishes after death. |

| Designated Beneficiary Plan Agreement | Establish Transfer on Death (TOD) or Payable on Death (POD) status. | Schwab One Brokerage and Investor Checking accounts. | Facilitates direct transfer of assets and potentially avoids probate. |

| Distribution — RMD Annual One-Time Payment | Request a mandatory annual distribution from a retirement plan. | Fidelity-administered employer retirement plans. | Ensures compliance with IRS regulations to avoid significant tax penalties. |

| Form F1387, Designating Beneficiaries for Your TIAA-CREF Accounts | Specify individuals to receive retirement funds as a death benefit. | TIAA-CREF Retirement and Supplemental Retirement Annuities. | Critical for estate planning to ensure assets reach intended beneficiaries. |

| Individual Retirement Account (IRA) — Qualified Charitable Distribution Form | Directly transfer funds from an IRA to a qualified charity. | Traditional, Roth, or beneficiary inherited IRAs. | Satisfies RMD requirements without the distribution being included in taxable income. |

| Premiere Select Roth IRA Conversion | Authorize the transfer of pre-tax assets into a post-tax Roth IRA. | Traditional, SEP, or SIMPLE IRAs. | Enables tax-free growth and withdrawals in exchange for immediate taxation. |

| Qualified Retirement Plan Designation of Beneficiary | Officially name primary and contingent heirs for retirement plan assets. | Qualified plans like 401(k) or 403(b) accounts. | Allows retirement assets to bypass probate and go directly to heirs. |

| Request for Required Minimum Distribution (RMD) - IRA Owner/Plan Participant | Start, update, or waive mandatory RMD payments from an annuity. | Fidelity & Guaranty Life Insurance Company annuity contracts. | Allows customization of payment frequency and specific tax withholding preferences. |

| TIAA Beneficiary Designation Form | Name individuals, trusts, or organizations to receive account assets. | TIAA retirement plan accounts. | Prevents legal complications and ensures assets are distributed per your wishes. |

| TIAA Beneficiary Designation Form (F11468) | Legally document heirs for retirement assets upon the holder's death. | TIAA retirement plans. | Ensures your wishes are carried out and avoids delays for heirs. |

| TIAA-CREF Form F1387, Designating Your Beneficiaries | Identify primary and contingent beneficiaries for annuity death benefits. | TIAA-CREF retirement and annuity accounts. | Helps heirs avoid legal complications and ensures clear asset distribution. |

| TIAA-CREF Form F1387, Designation of Beneficiary | Specify who will receive death benefits from an annuity contract. | TIAA-CREF annuity accounts. | Ensures assets are distributed correctly, avoiding potential legal delays. |

Tips for financial planning forms

AI-powered tools like Instafill.ai can complete complex financial forms in under 30 seconds with high accuracy. This is a major time-saver when managing multiple accounts, and you can rest assured that your sensitive data stays secure throughout the automated filling process.

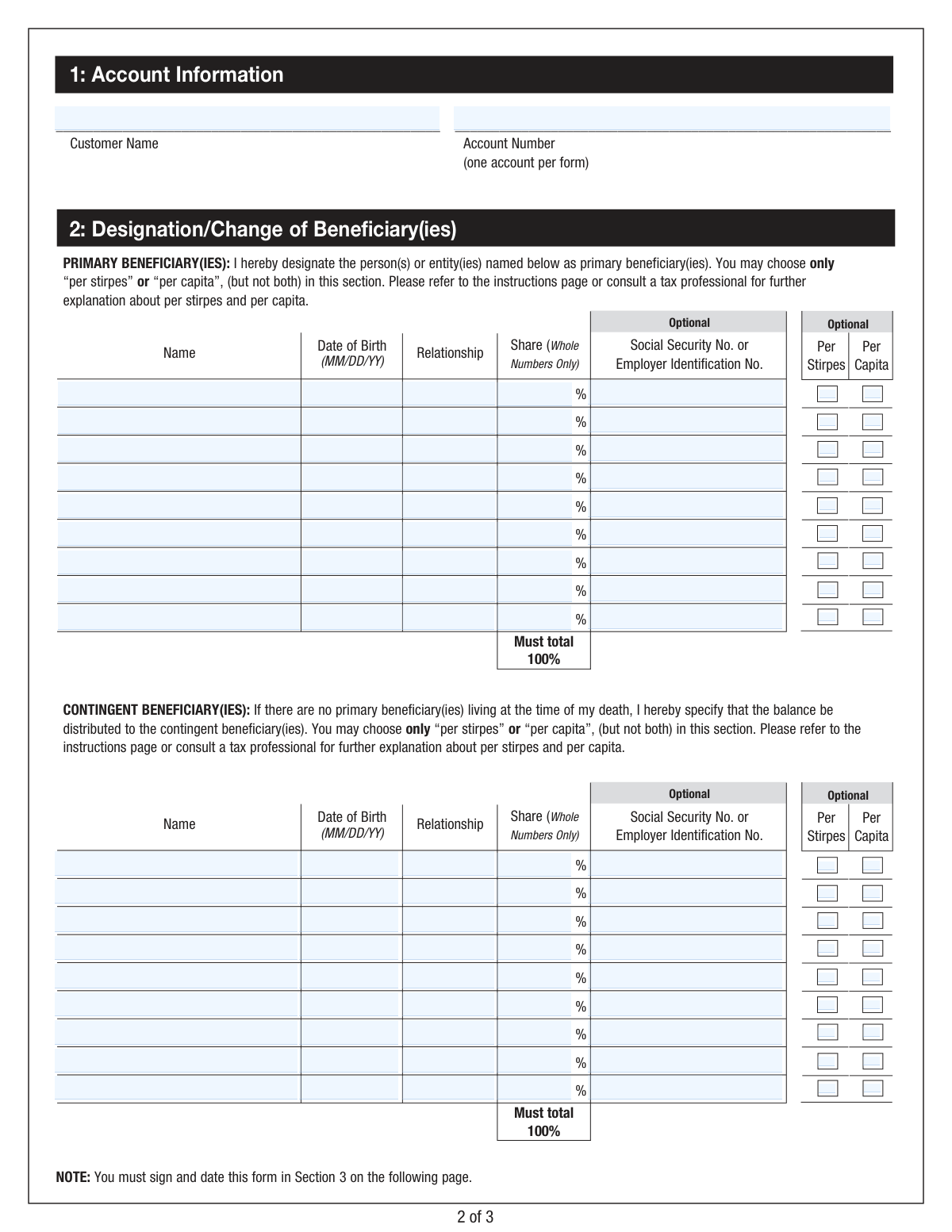

Always name a contingent beneficiary in addition to your primary choice to provide a backup for your assets. This simple step ensures your accounts are transferred according to your wishes even if your first beneficiary predeceases you, helping your estate avoid probate.

Double-check that Social Security numbers, dates of birth, and legal names are exactly correct for every person listed. Minor typographical errors on these forms can lead to significant legal delays or administrative hurdles for your heirs during the asset distribution process.

Remember that beneficiary designations on financial accounts typically override instructions in a will or trust. It is critical to review these forms periodically to ensure they remain synchronized with your broader estate plan and current family situation.

Treat financial planning forms as living documents rather than 'set and forget' paperwork. Make it a habit to update your forms immediately following life changes such as marriage, divorce, or the birth of a child to ensure your assets are directed to the correct individuals.

When requesting distributions or Roth conversions, pay close attention to the tax withholding sections. Failing to specify your preferences can result in default withholding rates that may not align with your actual tax bracket, potentially leading to an unexpected bill at year-end.

Frequently Asked Questions

Financial planning forms are essential documents used to manage assets, designate heirs, and handle tax-related distributions from retirement accounts. They help individuals communicate specific instructions to financial institutions such as Vanguard, Fidelity, or Charles Schwab regarding how their money should be handled or distributed.

Beneficiary designation forms ensure that your assets are transferred directly to your chosen heirs upon your death, often bypassing the lengthy and expensive probate process. These documents typically take precedence over instructions left in a will, making them one of the most important tools for ensuring your financial legacy is honored.

It is recommended to review and update these forms after major life events such as marriage, divorce, the birth of a child, or the death of a previously named beneficiary. Regular reviews, perhaps every few years, ensure your account instructions remain aligned with your current family situation and financial goals.

Yes, you can fill out various financial planning forms using AI tools like Instafill.ai. These tools can accurately extract data from your existing source documents and place it into the correct fields on the PDF, ensuring high accuracy for complex paperwork without manual typing.

Using AI-powered services, you can complete most financial planning forms in under 30 seconds. This technology significantly reduces the time spent on manual data entry while maintaining the precision required for legal and financial documents.

A primary beneficiary is the first person or entity designated to receive your assets upon your death. A contingent beneficiary acts as a backup, receiving the assets only if the primary beneficiary is no longer living or is unable to accept the inheritance at the time of distribution.

An RMD form is used to request the mandatory annual withdrawals that the IRS requires from certain retirement accounts once the owner reaches a specific age. These forms help you specify the amount to be withdrawn, the payment frequency, and your preferences for federal and state tax withholding.

While many financial planning forms are designed to be completed by the account holder, consulting with a financial advisor or legal professional is often helpful for complex estates. For standard updates to beneficiaries or simple distribution requests, most individuals can handle the paperwork themselves using the provided forms.

A QCD form allows an IRA owner who meets the age requirements to transfer funds directly from their retirement account to an eligible charity. This process can satisfy Required Minimum Distribution (RMD) obligations for the year without the distributed amount being included in the owner's taxable income.

Completed forms are typically submitted directly to the financial institution that holds the account, such as Merrill Lynch, TIAA, or Schwab. Most major institutions allow for submission via secure online portals, though some may still require the form to be sent via mail or fax depending on the specific transaction.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 41/100 (Basic). See exactly how it is calculated.

- Beneficiary (Primary vs. Contingent)

- The individual or entity designated to receive your assets; a primary beneficiary is first in line, while a contingent beneficiary receives assets only if the primary beneficiary is deceased.

- Required Minimum Distribution (RMD)

- The minimum amount the IRS requires you to withdraw from your retirement accounts annually once you reach a specific age, typically 73, to ensure tax-deferred funds are eventually taxed.

- Transfer on Death (TOD) / Payable on Death (POD)

- A legal designation that allows account assets to pass directly to named beneficiaries upon the owner's death, bypassing the lengthy and often expensive probate process.

- Probate

- The court-supervised legal process of validating a will and distributing a deceased person's estate; many financial planning forms are designed specifically to help assets avoid this process.

- Qualified Charitable Distribution (QCD)

- A direct transfer of funds from an IRA to a registered charity that can satisfy an RMD requirement without being counted as taxable income for the account owner.

- Roth IRA Conversion

- The process of moving funds from a pre-tax retirement account, such as a Traditional IRA or 401(k), into a Roth IRA, which involves paying taxes now to secure tax-free withdrawals later.

- Qualified Retirement Plan

- An employer-sponsored plan, such as a 401(k) or 403(b), that meets specific IRS guidelines and provides tax advantages for retirement savings.

- Annuity

- A financial contract typically offered by insurance companies that provides a guaranteed stream of income for a set period or for the remainder of the holder's life.