Fill out IRA rollover forms

with AI.

IRA rollover forms are essential documents used to move retirement assets from one account to another without incurring immediate tax penalties. This category covers a wide range of financial transitions, such as moving funds from an employer-sponsored 401(k) to a personal IRA or transferring between different financial institutions. Proper documentation is critical to ensure the transaction complies with IRS regulations, such as the 60-day rule or direct trustee-to-trustee transfer requirements, which protect your hard-earned savings from unnecessary taxation.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About IRA rollover forms

These forms are typically required by individuals who have changed jobs, retired, or inherited retirement assets from a deceased family member. Whether you are using a BlackRock IRA Rollover Certification Form to verify a contribution or a Vanguard Direct Rollover IRA Adoption Agreement to establish a new account, the goal is often to consolidate assets and maintain tax-deferred growth. Beneficiaries also use specialized forms, such as an Inherited IRA Transfer of Assets, to properly title and manage funds according to legal inheritance rules.

Navigating the complex fields of these financial documents can be time-consuming and prone to manual error. Tools like Instafill.ai use AI to fill these forms in under 30 seconds, ensuring that data is handled accurately and securely. By automating the process, you can quickly finalize your retirement account transitions and focus on your long-term financial strategy rather than paperwork.

Forms in This Category

The forms in this category have a median Form Complexity Index of 45/100 (Basic), measured across 14 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Selecting the correct IRA rollover form is essential to ensuring your retirement funds remain tax-deferred and avoiding unnecessary IRS penalties. Use the categories below to identify the form that matches your current financial transition.

Consolidating Employer-Sponsored Plans

If you are moving assets from a 401(k), 403(b), or other qualified plan into a new IRA, you generally need an application or adoption agreement.

- Vanguard Direct Rollover IRA Adoption Agreement: Use this when moving Vanguard mutual fund assets from an employer plan into a Vanguard IRA.

- Transamerica Premier Funds Direct Rollover IRA Application: Choose this to establish a new Transamerica account specifically for funds coming from an employer plan.

- Voya IRA Application and Adoption Agreement: A comprehensive package for opening a new Traditional or Roth IRA with Voya via a rollover.

Managing Automatic Rollovers

Sometimes, former employers automatically move small account balances into a default IRA. To take control of these funds, use specific Fidelity forms:

- Fidelity Advisor IRA Application for Automatic Rollover Accounts: Use this to claim an account that was automatically set up for you and choose your own investments.

- Fidelity Advisor IRA Distribution Request for Automatic Rollover Accounts: Select this if you want to withdraw the cash or move those automatically rolled funds to a different institution.

Time-Sensitive & Certification Forms

If you have already received a check personally and need to deposit it into an IRA within the IRS-mandated 60-day window, you must document the transaction:

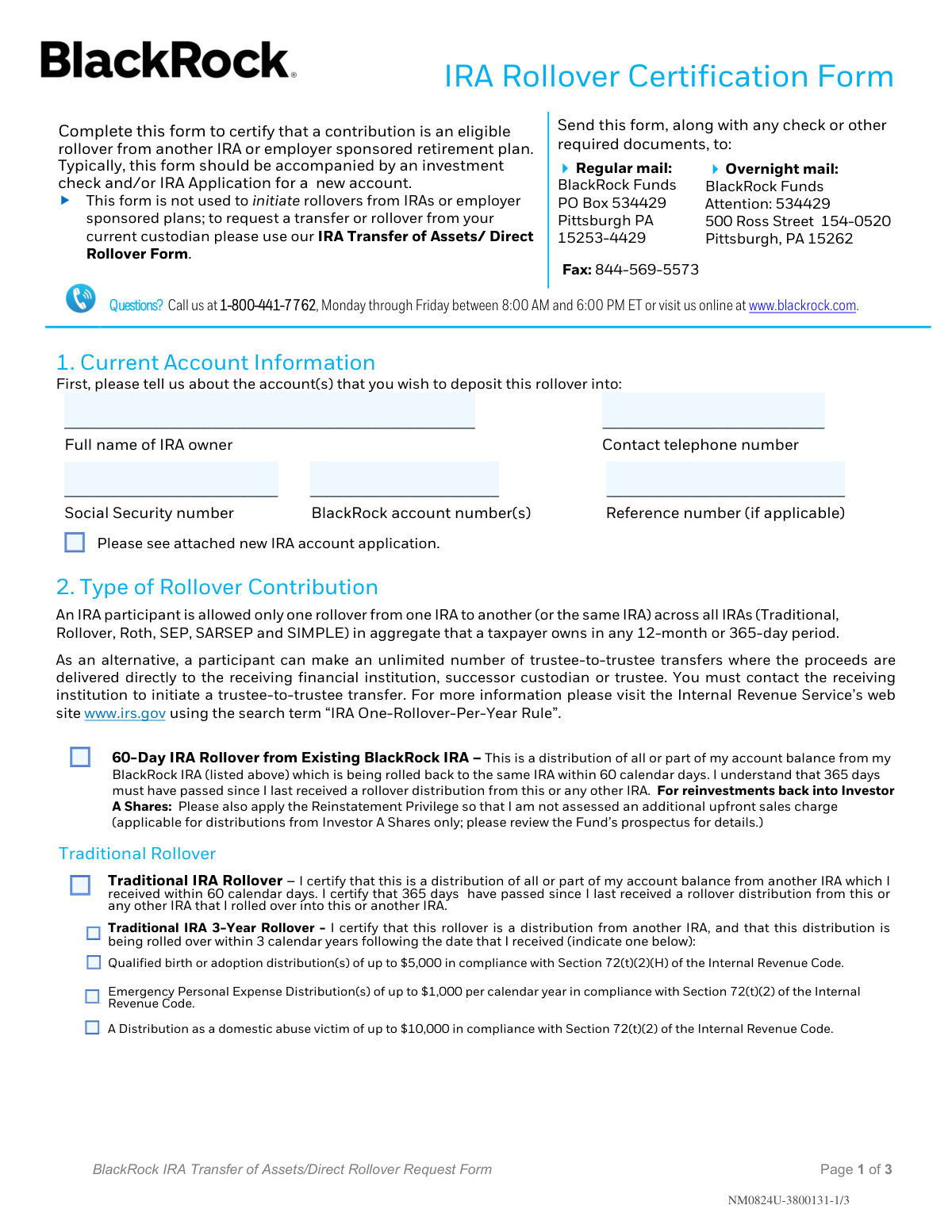

- BlackRock IRA Rollover Certification Form: Required to certify that your deposit meets IRS rules (like the one-rollover-per-year limit).

- Form F11260, TIAA IRA 60-Day Rollover Request: Use this for depositing funds into a TIAA account that were distributed to you from another institution.

Specialized Transfers & Inherited IRAs

For unique situations like inheritance or state-specific plans, specialized forms are required:

- Inherited IRA Transfer of Assets/ Direct Rollover Form: Use this (available for Voya or Impax) when you are the beneficiary of a deceased participant's retirement plan.

- Vanguard 529 College Savings Plan Direct Rollover Out to Roth IRA Form: A specific form for moving unused 529 college savings into a Roth IRA for the beneficiary.

- IRA Direct Rollover to QRP - American Century Investments: Use this to move funds from an IRA back into an employer’s Qualified Retirement Plan (QRP).

Tips for IRA rollover forms

AI-powered tools like Instafill.ai can complete these complex IRA forms in under 30 seconds with high accuracy. This is a significant time-saver when managing multiple accounts, and your sensitive financial data remains secure throughout the entire process.

If you receive rollover funds directly via check, you must deposit them into a new IRA within 60 days to avoid taxes and early withdrawal penalties. Have your certification forms ready before the funds arrive to ensure you don't miss this strict IRS window.

Whenever possible, choose a direct 'trustee-to-trustee' transfer rather than an indirect rollover. This method prevents the mandatory 20% federal income tax withholding that typically applies when funds are paid out directly to the account holder.

When using forms for inherited assets, the account title must follow a very specific format involving both the deceased owner's name and the beneficiary's name. Double-check the instructions on forms from providers like Voya or Impax to ensure the legal titling is exact to avoid processing delays.

Opening a new rollover IRA often requires fresh beneficiary designations, as your previous employer's settings will not automatically carry over. Take a moment to fill out this section completely on your Fidelity or BlackRock applications to ensure your estate plan remains intact.

Some financial institutions require a Medallion Signature Guarantee—which is different from a standard notary—for large transfers or distributions. Review the 'Authorization' section of your form early to see if you need to visit a physical bank branch to obtain this specific stamp.

Most rollover adoption agreements require you to specify how your funds should be invested the moment they arrive. Research the specific fund symbols or names for your new BlackRock or TIAA-CREF account beforehand so you can provide accurate allocation percentages on the form.

Frequently Asked Questions

These forms are used to move retirement assets from one account to another, such as from an employer-sponsored 401(k) to a personal IRA. They ensure the transfer is documented correctly with the financial institution and the IRS to maintain the tax-deferred status of your savings and avoid unnecessary penalties.

You typically need these forms when a former employer has automatically moved your retirement funds into a default IRA because your account balance was below a certain threshold. Using these forms allows you to take control of the account, choose your own investments, and designate beneficiaries for the new account.

An indirect rollover occurs when you receive a check for your retirement funds personally; you then have 60 days to deposit those funds into a new IRA to avoid taxes and penalties. Forms like the TIAA 60-Day Rollover Request are used to certify that you are meeting this specific IRS deadline.

Yes, under certain conditions, you can roll over unused 529 plan funds to a Roth IRA for the same beneficiary. Specific forms, such as the Vanguard 529ROR, help you navigate the lifetime limits and account age requirements set by the IRS for these types of transfers.

Financial institutions like BlackRock use certification forms to verify that the money you are depositing qualifies as a valid rollover. This protects both you and the institution by ensuring the transaction follows IRS rules, such as the limit of one indirect rollover per 12-month period.

If you are the beneficiary of a deceased participant's retirement plan, you must use specific Inherited IRA transfer forms. These documents ensure the assets are moved into a properly titled beneficiary account, which is managed differently than a standard IRA to comply with inheritance tax laws.

Yes, you can use AI-powered tools like Instafill.ai to complete these forms quickly. The AI can accurately extract data from your existing account statements or source documents and place it into the correct fields on the PDF in under 30 seconds.

While manually filling out complex financial forms can take 15 to 30 minutes, using an AI assistant can reduce this time significantly. AI tools like Instafill.ai streamline the process by automatically populating repetitive information and ensuring data accuracy across multiple pages in less than a minute.

Most financial institutions, such as Fidelity, Vanguard, or BlackRock, require you to submit the completed form directly to them via their secure online portal, fax, or mail. You should check the 'Submission Instructions' section on the specific form for the correct delivery address or digital upload link.

You will generally need your Social Security number, the account number of the originating retirement plan, and the contact information for the current custodian. If you are designating beneficiaries or choosing new investment allocations, you should have those details prepared as well.

A direct rollover usually refers to moving funds from an employer plan (like a 401k) to an IRA, while a transfer of assets typically refers to moving funds between two IRAs of the same type. Both processes allow you to move your money without triggering a taxable event, provided the correct forms are used.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 45/100 (Basic). See exactly how it is calculated.

- Direct Rollover

- A transfer of retirement assets directly from one plan provider to another, or from an employer plan to an IRA, without the money being paid to you first. This method is preferred because it avoids immediate taxes and mandatory federal withholding.

- 60-Day Rollover

- An indirect rollover where you personally receive a distribution check and must deposit those funds into another eligible retirement account within 60 days. Missing this deadline usually results in the IRS treating the money as taxable income and potentially applying early withdrawal penalties.

- Qualified Retirement Plan (QRP)

- An employer-sponsored plan, such as a 401(k) or 403(b), that qualifies for special tax treatment under the Internal Revenue Code. These plans are the primary source of funds for individuals opening a rollover IRA.

- Automatic Rollover

- A process where an employer moves a former employee's retirement savings into an IRA without their explicit instruction, usually because the account balance is small (typically under $7,000). These forms are used to take control of those funds once they have been moved to a default provider like Fidelity or BlackRock.

- Trustee-to-Trustee Transfer

- A transaction where retirement assets move directly between financial institutions without the account holder ever touching the money. This is common when moving funds between two IRAs of the same type and does not count toward the IRS 'one-rollover-per-year' limit.

- Inherited IRA

- A separate IRA account established for a beneficiary after the original account owner dies. These accounts have unique rules regarding how and when the money must be distributed, and the funds cannot be rolled over into the beneficiary's own personal IRA.

- Roth Conversion

- The process of moving pre-tax assets from a Traditional IRA or employer plan into a post-tax Roth IRA. This requires you to pay income tax on the amount converted in the current year, but allows for tax-free growth and withdrawals in the future.

- Custodian

- The financial institution, such as BNY Mellon or a brokerage firm, responsible for holding the assets in your IRA and reporting to the IRS. They ensure the account follows federal regulations but do not typically provide investment advice.