Fill out tax withholding forms

with AI.

Tax withholding forms are used to document, certify, and report the proper withholding of U.S. taxes on income paid to or by foreign individuals, entities, and intermediaries — as well as in situations involving worker classification and real property transactions. These forms serve as the legal basis for determining how much tax a payer must withhold before funds are disbursed, and they help ensure compliance with both standard IRS rules and international frameworks like FATCA. Getting them right matters: errors or missing documentation can trigger the default 30% withholding rate or cause significant payment delays.

By continuing, you acknowledge Instafill's Privacy Policy and agree to get occasional product update and promotional emails.

About tax withholding forms

These forms are commonly needed by foreign corporations and partnerships receiving U.S.-sourced income, financial intermediaries managing payments on behalf of multiple parties, businesses trying to correctly classify workers for payroll tax purposes, and buyers or transferees involved in U.S. real property transactions with foreign sellers. For example, Form W-8BEN-E is required by foreign entities to claim treaty benefits, Form W-8IMY is used by intermediaries to pass through withholding documentation, and Form 8288 is filed when withholding tax must be reported on a foreign person's disposition of U.S. real property.

Because many of these forms are lengthy, technically detailed, and easy to get wrong, tools like Instafill.ai use AI to help users fill them out accurately in under 30 seconds — a practical option for individuals and businesses who need to get the paperwork done without wading through complex IRS instructions.

Forms in This Category

The forms in this category have a median Form Complexity Index of 52/100 (Moderate), measured across 9 forms by field count, input difficulty, length, conditional logic and structure. See how it is calculated.

- Enterprise-grade security & data encryption

- 99%+ accuracy powered by AI

- 1,000+ forms from all industries

- Complete forms in under 60 seconds

How to Choose the Right Form

Start by identifying your situation: Are you a foreign entity or intermediary receiving U.S.-source income? Are you selling U.S. property? Or are you trying to clarify a worker's tax status? Each scenario points to a different form.

Foreign Entities Certifying Beneficial Owner Status

If you're a non-U.S. entity (corporation, partnership, trust, etc.) receiving U.S.-source income, you need one of the W-8BEN-E forms:

- Form W-8BEN-E (Rev. October 2021) — Use this version if you need to document both your Chapter 3 (NRA withholding) and Chapter 4 (FATCA) status, or if you want to claim a reduced withholding rate under a tax treaty.

- Form W-8BEN-E (standard version) — Functionally the same certificate; choose whichever version your withholding agent or payer requires. Both establish your identity and help avoid the default 30% withholding rate.

> Note: These forms are given directly to your payer or withholding agent — they are NOT filed with the IRS.

Foreign Intermediaries and Flow-Through Entities

- Form W-8IMY — Choose this if your entity acts as an intermediary (qualified or nonqualified), a foreign partnership/trust that is a flow-through entity, or a U.S. branch of a foreign entity. It's commonly submitted alongside a withholding statement and underlying payee documentation so the withholding agent can allocate payments correctly.

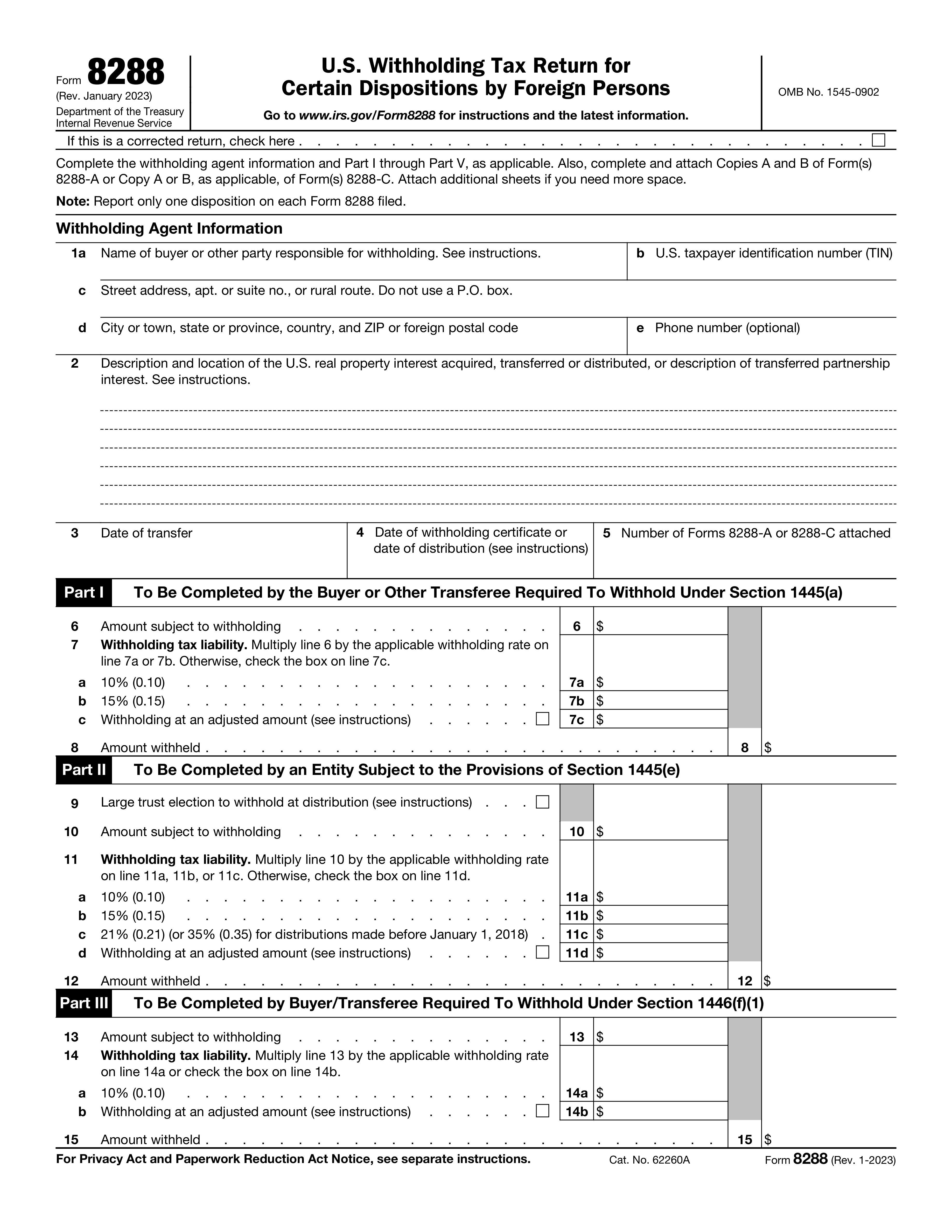

Withholding on U.S. Real Property Sales

- Form 8288 — Use this if a foreign person or entity is selling or transferring a U.S. real property interest. This form reports and remits the required withholding tax to the IRS and is the only form in this category that is actually filed with — and paid to — the IRS.

Worker Classification for Tax Withholding Purposes

- Form SS-8 — If there's a dispute or uncertainty about whether a worker is an employee or independent contractor, either the worker or the hiring firm can submit this form to ask the IRS for an official determination. This affects payroll tax obligations and income tax withholding going forward.

Form Comparison

| Form | Purpose | Who Files It | When to Use |

|---|---|---|---|

| Form 8288, U.S. Withholding Tax Return | Report and pay withholding tax on U.S. real property sales | Buyer or transferee of U.S. real property from foreign person | When foreign person sells or transfers U.S. real property interest |

| Form W-8IMY (Rev. October 2021), Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S. Branches for United States Tax Withholding and Reporting | Certify intermediary or flow-through entity status for withholding | Foreign intermediaries, flow-through entities, or qualifying U.S. branches | When receiving U.S.-source income on behalf of other payees |

| Form SS-8 (Rev. December 2023), Determination of Worker Status for Purposes of Federal Employment Taxes and Income Tax Withholding | Request IRS determination of employee vs. independent contractor status | Workers or firms seeking official IRS worker classification ruling | When employment status and withholding obligations are disputed or unclear |

| Form W-8BEN-E (Rev. October 2021), Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities) | Certify foreign entity beneficial owner status and FATCA classification | Non-U.S. entities receiving U.S.-source income | When claiming reduced withholding rates or treaty benefits as a foreign entity |

| Form W-8BEN-E, Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities) | Establish foreign entity identity, Chapter 3 type, and FATCA status | Foreign corporations, partnerships, trusts, and other organizations | When foreign entity receives U.S.-sourced income requiring withholding compliance |

Tips for tax withholding forms

Tax withholding forms vary significantly depending on whether you are an individual, a foreign entity, an intermediary, or a worker seeking classification. Using the wrong form — for example, submitting a W-8BEN-E when a W-8IMY is required — can cause payment delays or incorrect withholding. Take a moment to confirm your entity type and the nature of the income before you begin.

W-8 forms require you to declare both your Chapter 3 (NRA withholding) and Chapter 4 (FATCA) classifications, and these selections affect which sections of the form you must complete. Entering an incorrect or inconsistent classification is one of the most common errors on these forms. Review the IRS instructions or consult a tax advisor to confirm your classifications before filling in any boxes.

Withholding agents and payers are required to apply the default 30% withholding rate if a W-8 form is incomplete or missing required information. Make sure every applicable part of the form is filled out, including treaty claims, entity type checkboxes, and taxpayer identification numbers where required. An incomplete form can result in unnecessary tax being withheld that may be difficult to recover.

AI-powered tools like Instafill.ai can complete tax withholding forms — including complex W-8 forms and Form 8288 — in under 30 seconds with high accuracy, saving significant time especially when dealing with multiple forms. Your data stays secure throughout the process, making it a practical choice for businesses and individuals managing international tax obligations. This is especially useful for foreign entities that regularly need to provide updated certifications to multiple withholding agents.

W-8 forms are generally valid for three years from the date of signing, after which they must be renewed to avoid the withholding agent reverting to the default 30% rate. Set a reminder well before your certificate expires so you can provide an updated form without interrupting payments. Any change in circumstances that makes the form incorrect also requires immediate recertification, regardless of the expiration date.

The IRS requires detailed factual information — including contracts, invoices, and any Forms W-2 or 1099 — to process a worker classification determination via Form SS-8. Submitting the form without supporting documentation is a common reason for delays or inconclusive determinations. Gather all relevant records about behavioral control, financial arrangements, and the working relationship before filing.

A critical distinction with these forms is that W-8 certificates (such as W-8BEN-E and W-8IMY) are given directly to the withholding agent or payer — they are not filed with the IRS. Form 8288, on the other hand, is filed directly with the IRS along with the required withholding payment. Submitting a form to the wrong recipient can cause compliance failures and potential penalties.

Some versions of IRS tax withholding forms are distributed as non-fillable PDFs, which can make accurate completion difficult and error-prone if filled out by hand. Using a service that converts these into interactive fillable forms saves time and reduces transcription mistakes. This is particularly helpful for multi-page forms like the W-8IMY, which often requires accompanying withholding statements.

Frequently Asked Questions

Tax withholding forms are IRS documents used to establish, report, or determine the correct amount of tax to be withheld from certain payments. They are typically required by foreign individuals, foreign entities, intermediaries, and businesses involved in U.S.-sourced income or real property transactions. Withholding agents, payers, and workers seeking employment classification rulings may also need these forms.

W-8 forms (such as W-8BEN-E and W-8IMY) are certificates provided by foreign entities or intermediaries to withholding agents to establish their tax status and claim reduced withholding rates or exemptions. Other forms in this category, like Form 8288, are filed directly with the IRS to report and pay withheld taxes. Form SS-8 is distinct in that it asks the IRS to make a determination about a worker's classification for withholding purposes.

Foreign entities (such as corporations, partnerships, and trusts) should use Form W-8BEN-E to certify their beneficial owner status and claim reduced withholding rates under an applicable tax treaty. If the entity is acting as an intermediary or flow-through entity rather than the beneficial owner, Form W-8IMY is the appropriate form to provide to the withholding agent.

Form 8288 is required when a foreign person or entity sells or transfers a U.S. real property interest, triggering withholding tax obligations under FIRPTA (Foreign Investment in Real Property Tax Act). The buyer or transferee is generally responsible for withholding and must use this form to report and remit the withheld amount to the IRS.

No, W-8 forms such as W-8BEN-E and W-8IMY are not filed directly with the IRS. Instead, they are provided to the withholding agent or payer, who relies on them to determine the correct withholding rate and reporting requirements. The withholding agent retains these forms for their records.

Generally, W-8 forms remain valid for three calendar years after the year they are signed, unless a change in circumstances makes the information on the form incorrect. Entities must provide an updated form to their withholding agent whenever their status, entity type, or other certified information changes.

If a foreign entity does not provide a properly completed W-8BEN-E, the withholding agent is typically required to apply the default 30% withholding rate to U.S.-sourced payments. This can result in significant tax costs and payment delays, making it important for foreign entities to submit accurate documentation promptly.

Form SS-8 can be filed by either a worker or a business firm to request that the IRS determine whether a worker should be classified as an employee or an independent contractor for federal tax and withholding purposes. The IRS reviews facts about behavioral control, financial control, and the working relationship before issuing a determination, which affects payroll tax obligations and income reporting.

Yes, AI-powered tools like Instafill.ai can fill out tax withholding forms in under 30 seconds by accurately extracting and placing data from your source documents. This is especially helpful for complex forms like W-8BEN-E or W-8IMY, which require precise entity classification and treaty information. Instafill.ai can also convert non-fillable PDF versions of these forms into interactive fillable formats.

Manually completing tax withholding forms can take anywhere from several minutes to over an hour, depending on the complexity of the form and the information required. Using an AI-powered service like Instafill.ai, these forms can be completed in under 30 seconds by automatically extracting relevant data and populating the correct fields accurately.

Most forms in this category are specifically designed for international use — foreign individuals, foreign entities, and intermediaries receiving U.S.-sourced income are the primary users of W-8 forms and Form 8288. However, Form SS-8 applies to both U.S. and foreign workers and businesses seeking a worker classification determination from the IRS.

The submission destination varies by form: W-8 forms are given directly to the withholding agent or payer and not sent to the IRS, while Form 8288 is mailed to the IRS along with the withheld tax payment. Form SS-8 is submitted directly to the IRS for a formal determination. Always refer to the specific IRS instructions for each form to confirm the correct submission address and method.

Glossary

- Form Complexity Index

- Instafill’s 0–100 measure of how much effort a form takes to complete, calculated deterministically from the form’s own structure rather than estimated. It combines the number of fillable fields (the largest factor), how difficult those fields are to complete based on their type, the number of pages that contain fields, the amount of conditional “fill-only-if” logic, and how many sections the form is divided into, then adds modifiers for tables and repeating lists, bundled instruction pages, and dense page layouts. A higher score means the form is harder to fill out by hand. The forms in this category have a median Form Complexity Index of 52/100 (Moderate). See exactly how it is calculated.

- Withholding Tax

- A portion of income automatically deducted by the payer and sent directly to the IRS before the recipient ever receives the funds. It ensures taxes are collected at the source, particularly on payments made to foreign persons or entities.

- Withholding Agent

- Any person or entity (such as a bank, broker, or business) that has control over a payment to a foreign person and is legally responsible for deducting and remitting the correct amount of U.S. tax to the IRS.

- FATCA (Chapter 4)

- The Foreign Account Tax Compliance Act, a U.S. law requiring foreign financial institutions and certain other entities to report information about accounts held by U.S. persons. On W-8 forms, 'Chapter 4 status' refers to how an entity is classified under FATCA rules.

- Chapter 3 Status

- A classification under the U.S. tax code (Chapter 3 of the Internal Revenue Code) that determines the withholding rate applied to U.S.-sourced income paid to foreign persons, often referred to as NRA (Non-Resident Alien) withholding.

- Beneficial Owner

- The person or entity that ultimately owns or controls income and is entitled to its benefits, as opposed to an intermediary who merely passes it along. Withholding agents need to identify the beneficial owner to apply the correct tax rate.

- FIRPTA (Foreign Investment in Real Property Tax Act)

- A U.S. law requiring that taxes be withheld when a foreign person sells or transfers U.S. real property interests. Form 8288 is used to report and pay withholding taxes collected under FIRPTA.

- Qualified Intermediary (QI)

- A foreign financial institution or entity that has entered into a special agreement with the IRS to assume responsibility for withholding, reporting, and documentation on certain U.S.-source payments it receives on behalf of its customers.

- Tax Treaty

- A bilateral agreement between the U.S. and another country that can reduce or eliminate the standard 30% U.S. withholding tax rate on certain types of income. Foreign entities use W-8 forms to claim treaty benefits with their withholding agent.

- Worker Classification

- The IRS determination of whether a worker is an employee or an independent contractor, which directly affects payroll tax obligations, income tax withholding, and how income is reported (W-2 vs. 1099). Form SS-8 is used to request this determination.

- Flow-Through Entity

- A business structure (such as a partnership or certain trusts) that does not pay income tax at the entity level; instead, income 'flows through' to the owners or beneficiaries, who then report it on their own tax returns. Special withholding rules apply to foreign flow-through entities.