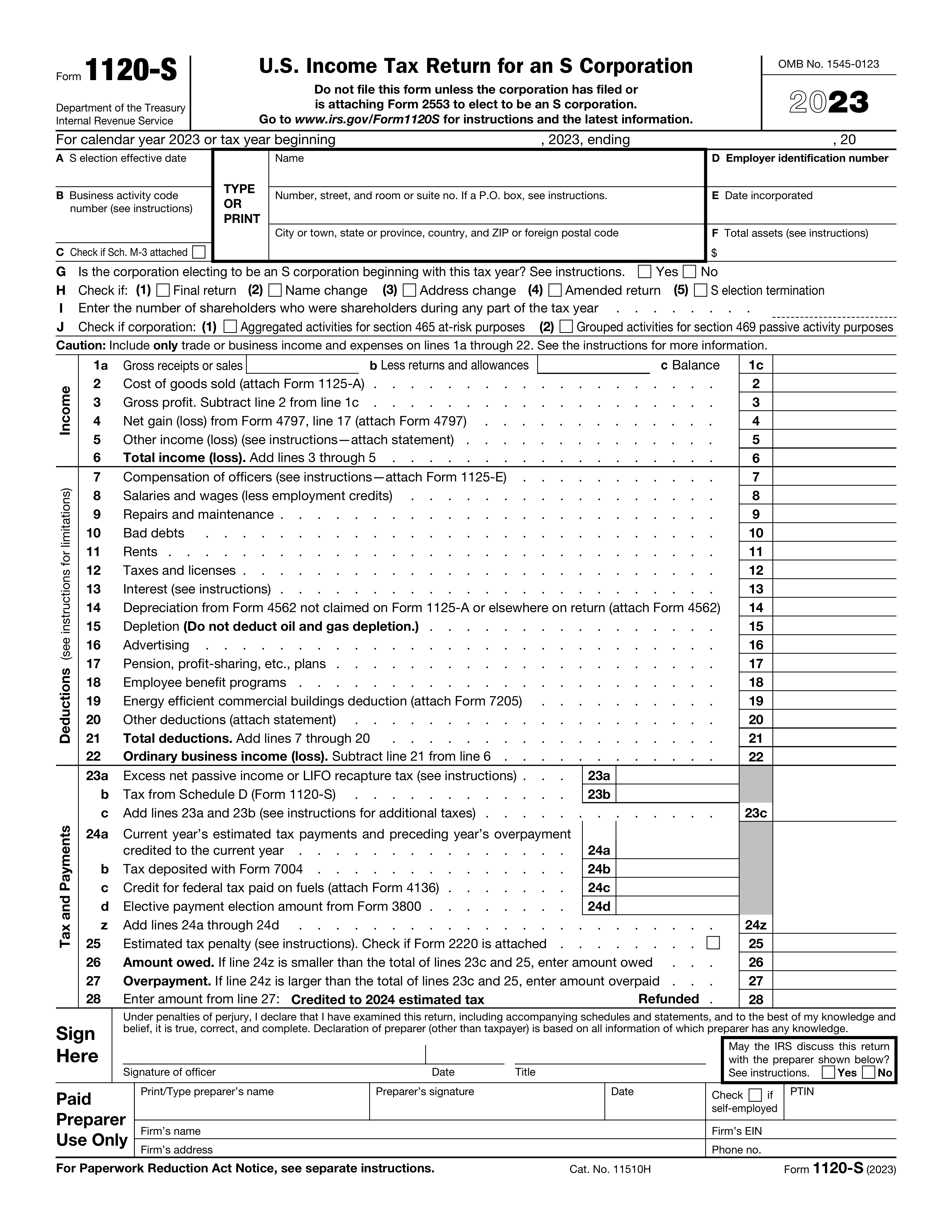

A critical mistake is not filing or attaching Form 2553, Election by a Small Business Corporation, before submitting Form 1120-S. This form is essential for a corporation to elect S corporation status. Without it, the IRS will not recognize the corporation as an S corporation, leading to potential tax liabilities as a C corporation. To avoid this, ensure Form 2553 is completed accurately and submitted timely, ideally within two months and 15 days after the start of the tax year the election is to take effect.

Submitting Form 1120-S with an incorrect or missing Employer Identification Number (EIN) is a common error that can delay processing. The EIN is crucial for the IRS to identify the corporation and process its tax return. To prevent this mistake, double-check the EIN on all documents before submission. If the corporation does not have an EIN, it must apply for one through the IRS before filing Form 1120-S.

Incorrectly stating or omitting the S election effective date on Form 1120-S can lead to misunderstandings about when the S corporation status begins. This date is vital for determining the tax year in which the S corporation election takes effect. To ensure accuracy, verify the effective date with the date on Form 2553 and consistently use this date on all related tax documents.

Reporting an incorrect business activity code number on Form 1120-S can misrepresent the corporation's primary business activities to the IRS. This code helps the IRS classify the corporation for statistical purposes and ensure compliance with tax laws. To avoid this error, carefully review the North American Industry Classification System (NAICS) codes and select the one that best matches the corporation's primary business activity.

Failing to attach Schedule M-3 when required is a mistake that can lead to penalties. Schedule M-3 is necessary for corporations with total assets of $10 million or more to reconcile financial accounting net income with taxable income. To prevent this oversight, assess the corporation's total assets and ensure Schedule M-3 is completed and attached if the threshold is met or exceeded.

Accurate reporting of total assets is crucial for the correct assessment of an S Corporation's financial health and tax obligations. Mistakes in this area can lead to discrepancies in the tax return, potentially triggering audits or penalties. To avoid this, ensure that all assets are accurately valued and reported according to the latest IRS guidelines. Regular audits and reviews of asset records can help maintain accuracy and compliance.

Failing to check the appropriate boxes for a final return or amendments can result in the IRS not recognizing the return's status, leading to processing delays or incorrect tax assessments. It is essential to carefully review the form instructions to determine if the return is final or amended and to mark the correct boxes accordingly. This attention to detail ensures that the IRS processes the return as intended, avoiding unnecessary complications.

Reporting an incorrect number of shareholders can affect the S Corporation's eligibility for certain tax treatments and credits. This mistake often stems from not keeping shareholder records up to date or misunderstanding the requirements for shareholder counting. To prevent this, maintain accurate and current records of all shareholders and consult the IRS guidelines or a tax professional to ensure the correct number is reported.

Accurate reporting of income and deductions is fundamental to complying with tax laws and avoiding penalties. Errors in this area can result from oversight, misunderstanding of tax rules, or incorrect data entry. To minimize mistakes, use reliable accounting software, double-check entries against financial records, and seek advice from tax professionals when uncertain about the classification or calculation of income and deductions.

Omitting required forms and statements can lead to incomplete tax returns, which may delay processing or result in the disallowance of certain deductions or credits. It is important to review the form instructions thoroughly to identify all required attachments for specific line items. Organizing and reviewing all documentation before filing can help ensure that no necessary forms or statements are overlooked.

A frequent error in filing Form 1120-S is the incorrect calculation of tax and payments. This can lead to discrepancies in the amount owed or refunded, potentially resulting in penalties or interest charges. To avoid this, it is crucial to double-check all calculations, including taxable income, deductions, and credits. Utilizing tax software or consulting with a tax professional can help ensure accuracy. Additionally, reviewing the IRS guidelines for S Corporations can provide clarity on how to correctly compute taxes and payments.

Failing to sign or date Form 1120-S is a common oversight that can invalidate the tax return. The IRS requires a signature from an authorized officer of the corporation to process the return. To prevent this mistake, ensure that the form is signed and dated before submission. It's also advisable to keep a copy of the signed return for your records. Establishing a checklist that includes verifying the signature and date can serve as a helpful reminder.

When a tax preparer is used to complete Form 1120-S, omitting their information is a mistake that can delay processing. The IRS requires the preparer's name, signature, PTIN, and other relevant details if someone other than the taxpayer prepares the return. To avoid this error, ensure that all preparer information is accurately filled out and included with the submission. Communication with the preparer about their responsibilities and the information required can help streamline this process.

An incomplete Schedule B can lead to questions or audits from the IRS, as it provides essential information about the corporation's activities and affiliations. To prevent this, thoroughly review Schedule B and ensure all applicable questions are answered accurately. Gathering all necessary information before beginning the form can help ensure completeness. Consulting the instructions for Schedule B can also clarify what information is required.

Inaccuracies in Schedule K can affect the shareholders' tax liabilities, as it details their pro rata share items. Errors here can lead to incorrect tax filings for shareholders and potential penalties. To avoid this, meticulously review all entries on Schedule K for accuracy. It's beneficial to cross-verify the information with the corporation's financial records. Engaging a tax professional to review Schedule K can also help ensure that all information is correctly reported.

Failing to fully complete Schedule L, which details the corporation's balance sheets per books, is a frequent oversight. This schedule is crucial for providing a clear financial picture of the corporation at the beginning and end of the tax year. To avoid this mistake, ensure all assets, liabilities, and equity accounts are accurately reported. Double-check the figures against the corporation's financial records to ensure consistency and completeness.

Incorrectly reconciling the corporation's book income with its taxable income on Schedule M-1 is a common error. This reconciliation is essential for identifying differences between financial accounting and tax reporting. To prevent this mistake, carefully review the corporation's financial statements and tax return to accurately identify and report any discrepancies. Consulting with a tax professional can also help ensure the reconciliation is done correctly.

Neglecting to complete Schedule M-2, which tracks the corporation's accumulated adjustments account (AAA) and other equity accounts, when applicable, can lead to inaccuracies in the tax return. This schedule is vital for S corporations to report changes in shareholder equity. To avoid this oversight, determine if Schedule M-2 is required based on the corporation's financial activities and ensure all relevant changes in equity are accurately reported.

Omitting necessary attachments and additional forms required by the IRS is a mistake that can delay the processing of the tax return. These attachments may include statements, schedules, or other documentation that supports the information reported on Form 1120-S. To prevent this error, thoroughly review the IRS instructions for Form 1120-S to identify all required attachments and ensure they are included with the tax return. Keeping a checklist of required documents can also help ensure nothing is overlooked.