Yes! You can use AI to fill out IRA Beneficiary Designation Form

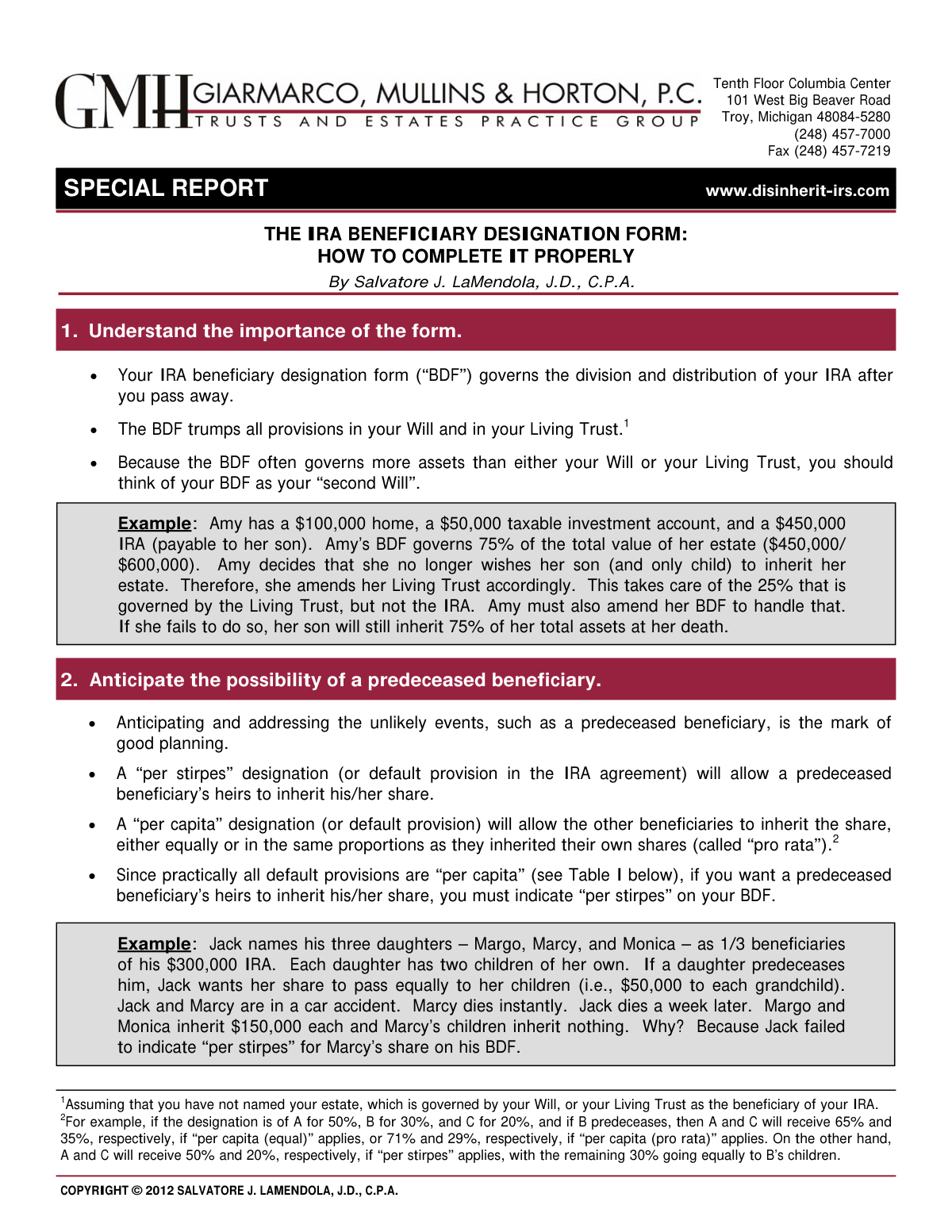

An IRA Beneficiary Designation Form (BDF) is a legal document that specifies who will receive the funds from your Individual Retirement Account (IRA) after you pass away. This designation is critically important as it supersedes any instructions in your will or living trust regarding the IRA assets, effectively acting as a 'second will' for a potentially large part of your estate. Today, this form can be filled out quickly and accurately using AI-powered services like Instafill.ai, which can also convert non-fillable PDF versions into interactive fillable forms.

IRA BDF is part of the

beneficiary forms, IRA forms, beneficiary designation forms and IRA beneficiary forms categories on Instafill.

Form specifications

| Form name: | IRA Beneficiary Designation Form |

| Number of pages: | 1 |

| Language: | English |

Our AI automatically handles information lookup, data retrieval, formatting, and form filling.

It takes less than a minute to fill out IRA BDF using our AI form filling.

Securely upload your data. Information is encrypted in transit and deleted immediately after the form is filled out.

Instafill Demo: How to fill out PDF forms in seconds with AI

How to Fill Out IRA BDF Online for Free in 2026

Are you looking to fill out a IRA BDF form online quickly and accurately? Instafill.ai offers the #1 AI-powered PDF filling software of 2026, allowing you to complete your IRA BDF form in just 37 seconds or less.

Follow these steps to fill out your IRA BDF form online using Instafill.ai:

- 1 Navigate to Instafill.ai and upload your IRA provider's Beneficiary Designation Form or select a template.

- 2 Enter your personal details as the IRA account owner, including your name and account number.

- 3 Clearly identify your primary beneficiaries, providing their full legal names, relationship, and other required details.

- 4 Specify the percentage of the IRA each primary beneficiary will inherit, ensuring the total adds up to 100%, and choose between 'per stirpes' or 'per capita' distribution if applicable.

- 5 Name contingent (or secondary) and successor beneficiaries who will inherit the assets if the primary beneficiaries are unable to.

- 6 Review all the information for accuracy, especially names and percentages, before electronically signing and dating the form.

- 7 Download the completed form, keep a copy for your personal records, and submit the original to your IRA custodian to ensure it is accepted and on file.

Our AI-powered system ensures each field is filled out correctly, reducing errors and saving you time.

Why Choose Instafill.ai for Your Fillable IRA BDF Form?

Speed

Complete your IRA BDF in as little as 37 seconds.

Up-to-Date

Always use the latest 2026 IRA BDF form version.

Cost-effective

No need to hire expensive lawyers.

Accuracy

Our AI performs 10 compliance checks to ensure your form is error-free.

Security

Your personal information is protected with bank-level encryption.

Frequently Asked Questions About IRA BDF

An IRA Beneficiary Designation Form (BDF) specifies who inherits your IRA assets when you die. It is critically important because its instructions override any conflicting directions in your Will or Living Trust for those specific funds.

Anyone who owns an Individual Retirement Account (IRA) must complete a Beneficiary Designation Form. It is essential to keep this form updated, especially after major life events like marriage, divorce, or the birth of a child, to ensure your assets go to the intended people.

A 'per stirpes' designation means that if one of your beneficiaries predeceases you, their share will pass down to their own heirs. In contrast, 'per capita' means the deceased beneficiary's share would be divided among your other surviving primary beneficiaries.

A contingent beneficiary inherits your IRA only if your primary beneficiary has already passed away at the time of your death. A successor beneficiary is designated to inherit any remaining IRA funds after the original beneficiary, who did inherit from you, passes away.

A 'stretch-out' allows your beneficiary to take distributions over their own life expectancy, maximizing the tax-deferred growth of the IRA funds. This is often more financially advantageous than a 'cash-out,' where the entire amount is withdrawn at once and subject to immediate, and often higher, income tax.

Yes, you can name a trust as your IRA beneficiary, which provides greater control over how and when the assets are distributed to heirs. However, this requires specific, careful wording on the BDF, so consulting with a legal or financial advisor is highly recommended.

You should review your BDF at least annually and any time a major life event occurs, such as a birth, death, marriage, or divorce. An outdated form can cause your IRA, which may be your largest asset, to be inherited by someone you no longer intend.

If no valid BDF is on file at the time of your death, your IRA provider will distribute the assets according to the default rules in your IRA agreement. These default rules may not align with your wishes, so it's crucial to have a BDF on file and to keep a copy for your own records.

The default provisions in the specific IRA agreement you signed are what govern your account if your BDF is invalid or missing. Since providers can update their standard agreements over time, keeping your original signed copy ensures you have proof of the rules that apply to your account.

Yes, services like Instafill.ai use AI to accurately auto-fill form fields, which can save you time and help prevent common errors. While helpful for standard entries, you should still consult a professional for complex estate planning decisions like naming a trust.

You can use a service like Instafill.ai to complete your BDF online. Simply upload the form from your IRA provider, and the tool will allow you to type your information directly onto the document before you print it for signing and submission.

If you have a non-fillable or 'flat' PDF, you can use a tool like Instafill.ai to instantly convert it into an interactive, fillable form. This allows you to easily type in your beneficiary information for a clean and legible final document.

If naming multiple beneficiaries, confirm that your IRA agreement allows for the creation of 'separate accounts' after your death. This enables each beneficiary to use their own life expectancy for calculating distributions, which is especially beneficial for younger heirs.

A disclaimer is a formal refusal by a beneficiary to accept the inheritance. You can plan for this by naming a specific 'disclaimer contingent beneficiary' (like a charity or another person) who would inherit only if the primary beneficiary officially disclaims the asset.

Compliance IRA BDF

Validation Checks by Instafill.ai

1

Primary Beneficiary Percentage Summation

This check verifies that the percentages assigned to all primary beneficiaries add up to exactly 100%. This is critical to ensure the entire IRA is distributed according to the owner's wishes without ambiguity. If the total is not 100%, the designation could be legally challenged, leading to disputes or distribution according to the IRA provider's default rules.

2

Contingent Beneficiary Percentage Summation

This check validates that the percentages assigned to all contingent beneficiaries sum to exactly 100%. This ensures a clear line of inheritance if no primary beneficiaries survive the IRA owner. An incorrect sum can create legal uncertainty and may result in the assets being distributed to the owner's estate instead of the intended individuals.

3

Beneficiary Information Completeness

This validation ensures that each designated beneficiary has a full legal name, date of birth, and a Social Security Number (SSN) or Taxpayer Identification Number (TIN). Complete and accurate information is essential for the IRA custodian to locate and verify the identity of the beneficiaries after the owner's death. Missing information can cause significant delays and complications in the distribution process.

4

Per Stirpes/Per Capita Designation Check

This check confirms that a distribution method ('per stirpes' or 'per capita') has been selected for each beneficiary where applicable. This choice dictates how a deceased beneficiary's share is handled, either passing to their heirs or being divided among the other surviving beneficiaries. Failing to make an explicit choice will subject the distribution to the custodian's default rule, which may not align with the owner's intent.

5

Trust Beneficiary Naming Convention

This validation verifies that when a trust is named as a beneficiary, it is identified with the proper legal language, including the name of the trust, the trustee, and the date of the trust agreement (u/a/d). Using precise legal language is crucial to ensure the designation is valid and that the trust can be properly funded. Vague designations can lead to legal challenges and may invalidate the bequest to the trust.

6

Minor Beneficiary Custodian Assignment

This check ensures that if a beneficiary is identified as a minor based on their date of birth, a custodian has been named for them under the Uniform Transfers to Minors Act (UTMA). Without a designated custodian, a court-appointed guardian may be required to manage the funds, a process that is costly and time-consuming. The validation confirms that a responsible adult is legally appointed to manage the inheritance until the minor reaches the age of majority.

7

IRA Owner Signature and Date Presence

This validation confirms that the IRA owner has signed and dated the Beneficiary Designation Form. A signature is required to legally execute the document and make the designations binding. An unsigned or undated form is invalid and will be rejected, meaning any previous designation or the provider's default rules will apply upon the owner's death.

8

Primary Beneficiary Existence

This check ensures that at least one primary beneficiary is designated on the form. Naming a primary beneficiary is the fundamental purpose of the form, establishing the first in line to inherit the IRA assets. If no primary beneficiary is listed, the assets will pass to the contingent beneficiaries or, if none, to the owner's estate, which can have significant tax and probate implications.

9

Charitable Beneficiary EIN Verification

This check verifies that any organization named as a beneficiary, such as a charity, includes a valid Employer Identification Number (EIN). The EIN is necessary to confirm the organization's legal and tax-exempt status, ensuring the funds are transferred correctly. An incorrect or missing EIN can delay the distribution or cause it to fail.

10

Conditional Language for Trust Beneficiaries

This validation checks for the presence of conditional language (e.g., 'If my spouse survives me...') when a trust is named as a beneficiary. This is important to create a clear succession plan if the condition is not met, such as the spouse predeceasing the owner. The absence of such language can create ambiguity and lead to the IRA passing to the trust unnecessarily, complicating the estate settlement.

11

Account Identification Specificity

This validation ensures that the form clearly specifies the IRA account number(s) to which the designation applies. An IRA owner may have multiple accounts, and failing to specify which one is covered by the BDF can lead to the designation being applied incorrectly or not at all. This check prevents ambiguity by requiring an explicit link between the designation and the asset.

12

Disclaimer Beneficiary Specification

This check verifies if a specific beneficiary has been named to receive assets in the event a primary beneficiary disclaims their share. The desired disclaimer beneficiary may be different from the standard contingent beneficiary, such as a charity instead of grandchildren. Explicitly naming a disclaimer beneficiary provides flexibility for post-mortem estate planning and ensures assets flow to the intended alternate recipient.

Common Mistakes in Completing IRA BDF

A Beneficiary Designation Form (BDF) is often a 'set it and forget it' document, and people forget to update it after a marriage, divorce, birth, or death. This is a critical error because the BDF supersedes a Will, meaning an ex-spouse could inherit your entire IRA if you forgot to remove them as the primary beneficiary. To prevent this, review your BDF annually and immediately after any significant life event.

People often list their children as beneficiaries but forget to add the 'per stirpes' designation, assuming a deceased child's share will automatically pass to their grandchildren. The consequence is that if a child predeceases the IRA owner, their share is split among the surviving primary beneficiaries ('per capita'), disinheriting the grandchildren. To avoid this, always add 'per stirpes' next to a beneficiary's name if you want their heirs to inherit their share.

When naming multiple beneficiaries, a common data entry error is assigning percentages that do not add up to exactly 100%. This happens due to simple miscalculation or typos, and the IRA custodian may reject the form or apply default rules that don't align with your intent. To avoid this, double-check all percentages before submitting. AI-powered form filling tools like Instafill.ai can prevent this error by automatically validating that percentages sum to 100%.

Filers often stop after naming primary and contingent beneficiaries, not considering who should inherit the IRA balance after the primary beneficiary dies. This oversight means the IRA provider's default rules will apply, often passing the remaining assets to the primary beneficiary's estate or spouse, which may not be the original owner's wish. To ensure your assets follow your intended path, you must explicitly name successor beneficiaries, which may require using a custom trust.

People sometimes just write a name or relationship (e.g., 'my son, John') without providing a full legal name, date of birth, and Social Security Number. This lack of detail can create significant delays and legal hurdles for the beneficiary when they try to claim the assets, as the custodian must verify their identity. Always provide complete and accurate identifying information for every beneficiary listed to ensure a smooth transition.

When designating a trust, people often use simple language like 'The John Doe Trust,' which can cause major complications. This is especially true if the trust is for a specific person who might predecease the IRA owner or if multiple sub-trusts are involved, potentially disqualifying the 'stretch-out' provision. Use precise, conditional language specifying the full trust name, date, and conditions for inheritance to avoid ambiguity.

People fill out the BDF assuming their IRA provider allows for features like mandated stretch-outs, separate accounts for multiple beneficiaries, or portability to another institution. Many standard agreements do not permit these, limiting the beneficiary's options and potentially costing them significant money in taxes or lost growth. Before filling out the BDF, review your IRA custodial agreement to understand its rules; if the agreement is restrictive, consider moving the IRA to a provider with more flexible terms.

An IRA owner may not consider that their wealthy primary beneficiary might want to 'disclaim' (refuse) the inheritance for tax or estate planning reasons. Without a specific disclaimer beneficiary named, the disclaimed portion goes to the contingent beneficiaries, which may not be the desired outcome (e.g., if the goal was to give it to charity). This forces the primary beneficiary into a less tax-efficient process of inheriting and then gifting the funds, so use specific language to name a different beneficiary in the event of a disclaimer.

An IRA owner may become incapacitated and unable to manage their own finances. Without a Durable Power of Attorney (DPOA) that explicitly grants an agent authority to handle IRAs, your accounts can become mismanaged or fail to adapt to changing circumstances. This can result in lost opportunities, like a spousal rollover, so ensure you have a DPOA that specifically lists the IRA-related powers your agent can exercise.

After submitting the form, many people fail to keep a copy for their records. If the IRA custodian loses the form or has an outdated version on file, there is no proof of the owner's final wishes, which can lead to disputes and incorrect distributions. Always keep a physical or digital copy of the signed and accepted BDF with your other important estate documents. Tools like Instafill.ai can make any flat PDF fillable and save a clean, digital copy for your records.

Saved over 80 hours a year

“I was never sure if my IRS forms like W-9 were filled correctly. Now, I can complete the forms accurately without any external help.”

Kevin Martin Green

Your data stays secure with advanced protection from Instafill and our subprocessors

Robust compliance program

Transparent business model

You’re not the product. You always know where your data is and what it is processed for.

ISO 27001, HIPAA, and GDPR

Our subprocesses adhere to multiple compliance standards, including but not limited to ISO 27001, HIPAA, and GDPR.

Security & privacy by design

We consider security and privacy from the initial design phase of any new service or functionality. It’s not an afterthought, it’s built-in, including support for two-factor authentication (2FA) to further protect your account.

Fill out IRA BDF with Instafill.ai

Worried about filling PDFs wrong? Instafill securely fills ira-beneficiary-designation-form forms, ensuring each field is accurate.